CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Catherine Ngai and Michael Roschnotti

Now, as the shale industry tries to pick up the pieces after Saudi Arabia’s latest price war caused crude to plummet, some of those same producers are reliving the same costly mistake. Noble Energy Inc., Callon Petroleum Co. and Parsley Energy Inc. are among producers sorely exposed to the latest market crash due to their hedging strategy, a Bloomberg review of company records show.

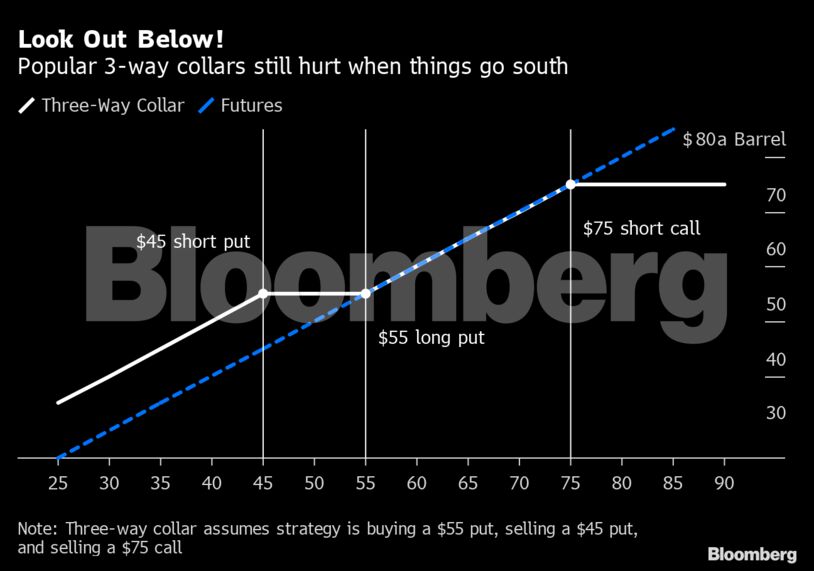

At issue are complex financial contracts called three-way collars. The options are a relatively cheap way to hedge against price fluctuations, as long as prices don’t fall too much. Compared with swaps, which guarantee a certain price, the collars are essentially costless — a key consideration in such a capital intensive industry where expenses have been cut nearly to the bone in order to survive and turn a profit.

While the three-way collars fell out of favor after the crash of 2014, many shale producers started loading up again in the past year or so, comforted by crude prices that reliably hovered between $50 and $60 a barrel.

“Flash forward, all those old habits for three-way collars started creeping back in,” said John Saucer, vice president of research and analysis at Mobius Risk Group, an energy risk management and advisory firm that works with oil producers. “It worked when oil was trading range-bound. But then things changed.”

Exposed

Hedging, in theory, protects producers from market declines by allowing them to lock-in a certain price for their oil. One way a company can hedge output is by buying a floor on the price (called a put option) and then offsetting the cost of that floor by selling a ceiling (a call option). To cut costs even further, a producer can sell what’s known as a subfloor, a put option that’s much lower than where prices are currently trading. That three-pronged approach is known as a three-way collar and it functions well when oil’s moving sideways but can leave producers vulnerable if the market bottoms out.

That wasn’t a problem during shale’s heyday, when West Texas Intermediate hummed around $90 a barrel, or even last month, when prices were trading within a predictable range.

But after Saudi Arabia last week announced it would flood the market with cheap crude, at least 350,000 barrels a day of WTI contracts became exposed to the meltdown in oil prices, according to data from BloombergNEF.

While most oil hedges are in the relatively safe form of swaps, “certain producers are in a bad position currently due to unfortunate three-way collars,” said Daniel Adkins, an analyst at BNEF.

Nevertheless, the strategy has become increasingly important to some producers’ hedging portfolios in recent years, according to company filings.

Deja Vu

Pioneer Natural Resources Co., which in the aftermath of the 2014 crash converted 85% of it oil derivatives from three-way collars to fixed-price swaps, recently started loading up on three-ways again. By the end of 2019, the company hedged almost 50 million barrels of oil using the strategy, up from just 5.5 million the year before.

In the last two years, Denbury Resources Inc. also eased its swap positions in favor of three-way collars, repeating a move it made from 2013 through 2015.

Parsley had more than 27 million barrels hedged using three-ways at the end of 2019, four times more than the prior year. The company also decreased use of put spreads and fixed-price swaps. While it had some three-way structures in 2014, it had none by the end of 2015.

Parsley on Monday announced it restructured its hedges and is reigning in capital spending in light of the downturn.

“Our three-ways were set up to protect against the price at which 80% of North American projects were no longer economic,” Parsley Chief Executive Officer Matt Gallagher said in a statement. “We are aggressively looking at all options to protect against asymmetric risk.”

Occidental Petroleum Corp. also plans to cut capital spending after prices plunged below some of its hedging levels and threatened its dividend.

“When you look at three-way collars, given the volatile nature of this market, being knocked out of the market was always a viable threat depending on how quickly prices moved,” said Michael Tran, director of global energy strategy at RBC Capital Markets. “This was an insurance policy that wasn’t always guaranteed.”

Share This: