CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Neil Ford

- Summary

- A dependence on components from Asia, import tariff uncertainty and demand concerns have curbed plans for American solar factories.

U.S. module factory capacity rose 11 GW in Q1 2024 as tax credits in the 2022 Inflation Reduction Act bore fruit, data from the Solar Energy Industries Association (SEIA) and Wood Mackenzie showed.

The increase brings U.S. module production capacity to 27 GW/year, compared with just 8 GW in 2022. Over the past year, Qcells expanded its Georgia module factory to 8.4 GW and First Solar expanded production in Ohio to 6.3 GW. Other new capacity comes from Canadian Solar (5 GW modules), Illuminate USA (LONGi/Invenergy) (5 GW modules) and REC Silicon (6 GW polysilicon).

The U.S. installed a record 40 GW of solar power in 2023 but flat growth, is forecast in 2024 and 2025 and higher installation rates are needed to achieve President Biden’s ambitious climate targets.

China dominates global solar supply and most U.S. developers source low cost solar panels from Southeast Asia, where many Chinese companies have shifted operations to bypass U.S. tariffs.

Many U.S. developers are looking to source American modules in the coming years, following new tax credits in the inflation act and increasing uncertainty over imports. However, U.S. supply chain plans are being hampered by a surplus of modules from China which has driven down global prices. U.S. module imports hiked 82% in 2023 to 54 GW on the back of rapidly falling prices.

Advertisement · Scroll to continue

In response, the Biden administration increased tariffs on solar imports from China and Southeast Asia to protect U.S. manufacturers, a move that will increase prices for developers.

U.S. manufacturing capacity will continue to rise but medium term growth is uncertain due to the current oversupply of modules and other supply and demand factors that are deterring new announcements.

Manufacturing growth could be hampered by supply chain gaps and skills shortages and solar developers will continue to face long grid connection queues and permitting challenges, which could soften the demand for U.S. products, Quill Robinson, Senior Program Manager at the Centre for Strategic and International Studies, told Reuters Events.

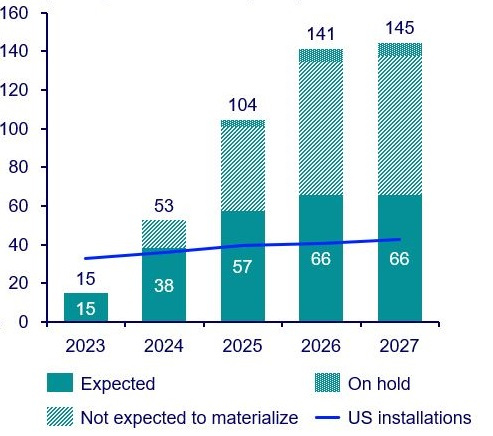

Research group Wood Mackenzie predicts U.S. module manufacturing capacity will reach 38 GW by end-2024 and 57 GW by end-2025, forecasting only a slight increase to 66 GW by the end of 2027, based on the latest announcements.

CHART: Announced US module manufacturing capacity (GW)

There have been few manufacturing announcements in recent months, Elissa Pierce, Research Analyst, Power & Renewables at Wood Mackenzie, said.

While suppliers that are already “well-known and bankable” in the U.S. are expanding, other aspiring manufacturers have delayed factory projects because of oversupply, Pierce said.

“They cannot secure financing or offtake,” she said.

Tariff threat

Import tariffs on China and Southeast Asia imposed by the Biden administration in May will increase the price of modules for U.S. developers. Prior to this, the cost of manufacturing solar equipment in China was 55% lower than in the United States, according to analysis from S&P Global Commodity Insights.

The Department of Commerce (DOC) also opened an investigation into whether producers in Southeast Asia are benefiting from government subsidies and dumping products in the U.S. market, with a preliminary decision expected this month.

Any tariff action resulting from the DOC probe would encourage more domestic manufacturing, but it would hike prices for both imported and domestic modules due to a dependence on components from Asia.

Antidumping and countervailing duties would increase the price of imported modules by 15 cents per watt, or 66%, to 40 cents per watt, curbing U.S. solar installations, Clean Energy Associates (CEA) said in a new report commissioned by the American Council on Renewable Energy (ACORE).

New duties would increase the price of American panels by 10 cents per watt, or 45%, to 32 cents per watt, the advisory group noted.

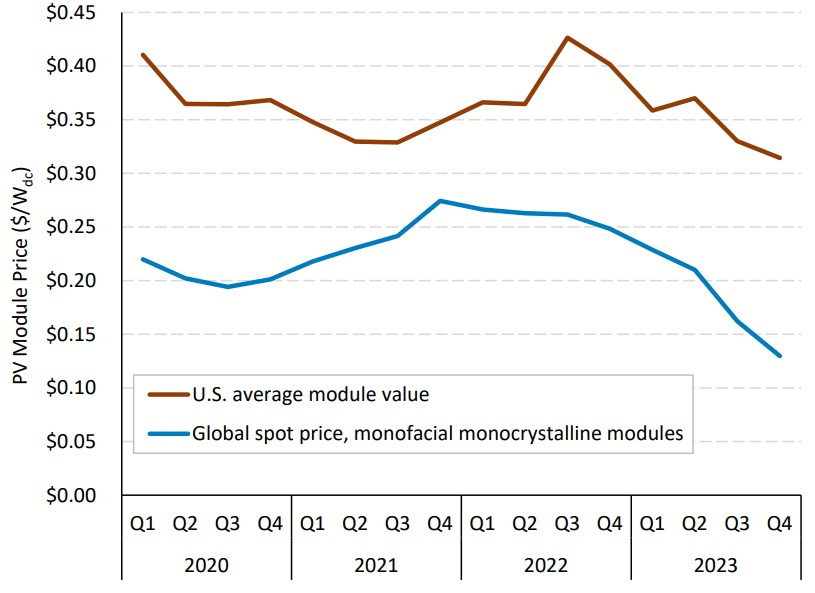

Module prices for late 2024 and 2025 fell on the back of U.S. manufacturing growth but this decline has been “reversed by the 2024 antidumping and countervailing duty (AD/CVD) case,” Joseph Johnson, Associate Director, Market Intelligence at Clean Energy Associates (CEA), told Reuters Events.

“Many U.S. manufacturers will have to pay tariffs on cell imports and will have room to increase their margins,” Pierce noted.

The price of American modules should slowly decrease over time through economies of scale, increased competition and efficiency improvements, Pierce said.

By the end of 2025, the price of utility-scale TOPCon modules – the leading type of cells shipped globally – should soften from 27c/W to 26c/W, she said.

Supply chain gaps

Expansions in U.S. solar cell, wafer and polysilicon production are lagging far behind module capacity, meaning module manufacturers will remain dependent on Asian components.

The Chinese solar industry benefits from 20 years of industrial policy “that has methodically created integrated and resilient supply chains,” Robinson noted.

U.S. wafer production was zero in 2022 and some manufacturers have ditched plans to build new capacity, blaming a collapse in global product prices, high energy prices and rising construction costs. Recent cancellations include CubicPV’s wafer plant, REC Silicon’s Montana polysilicon project and Enphase ceasing microinverter production in Wisconsin.

Wafer production is relatively capital intensive and suppliers in China and Southeast Asia benefit from far lower capital costs. Importantly, U.S. solar developers do not need to source U.S. wafers to meet domestic content thresholds and receive bonus tax credits.

WoodMac forecasts U.S. wafer production capacity at just 3 GW by the end of 2027 and cell capacity at 18 GW.

November’s presidential election casts further uncertainty over the solar industry, since the current growth trajectory is underpinned by the Biden administration’s inflation reduction act and other regulatory changes that favour low carbon technologies.

According to Robinson, the supply-side incentives provided to manufacturers should be more politically durable than demand-side incentives given to developers.

“Republicans like factories but are more sceptical of demand-side incentives,” he said.

Share This: