CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Energy and materials companies were among the worst performers on the S&P 500 Index. In Europe, a gauge of tech stocks fell the most since March after German software maker SAP SE plunged 20% following a cut to its revenue forecast and warnings that the pandemic will hurt business through mid-2021. Boeing Co., Lockheed Martin Corp. and Raytheon Technologies Corp. slid on China’s plan to sanction the companies after the U.S. approved $1.8 billion in arms sales to Taiwan last week.

The dollar strengthened and Treasuries rose, sending yields on the 10-year lower. Oil futures and copper declined, while gold was little changed.

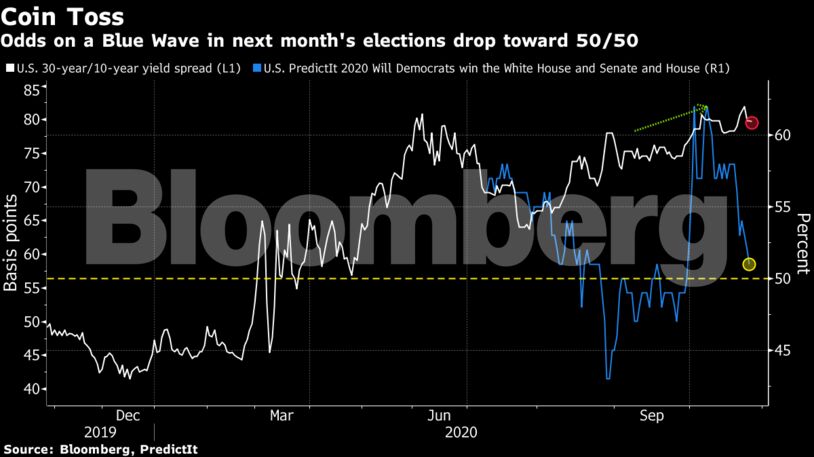

Investors remain focused on the prospect of a U.S. stimulus deal, even as time runs out to finish an aid package before the election. On the virus front, the World Health Organization’s director general said some countries in the northern hemisphere are facing a “dangerous moment” after U.S. infections hit a record for the second day. European countries are also tightening restrictions on business.

“The current mood in the market is bracing and non-committal,” said Peter Rosenstreich, head of market strategy at Swissquote Bank SA. “The concern around the Covid-19 pandemic and U.S. fiscal stimulus is dominating the market.”

In Washington, House Speaker Nancy Pelosi said she’s waiting for another aid counteroffer Monday from Treasury Secretary Steven Mnuchin, as she and White House Chief of Staff Mark Meadows accused each other of “moving the goalposts” in negotiations.

In other markets, the MSCI Asia Pacific Index slipped, with Japan and South Korea posting declines. Emerging-market stocks were also lower.

Turkey’s lira weakened past 8 per dollar for the first time. The central bank rattled investors last week by unexpectedly keeping rates on hold, and geopolitical risks have sapped interest in Turkish assets.

These are some events to watch this week:

- The Chinese Communist Party’s Central Committee holds its all-important plenum, where it’s expected to chart the course for the economy’s development for the next 15 years. Through Oct. 29.

- Brexit negotiating teams have started intense daily negotiations, and these are likely to continue as both sides push to finalize a deal by the middle of November.

- Bank of Japan and the European Central Bank have monetary policy decisions Thursday, followed by briefings from Governor Kuroda and President Lagarde.

- The first reading of U.S. 3Q GDP Thursday is anticipated to be the strongest on record following a record dive in the prior quarter as many businesses were shuttered by the pandemic.

Here are the major moves in markets:

Stocks

- The S&P 500 Index decreased 0.9% as of 9:31 a.m. New York time.

- The Stoxx Europe 600 Index fell 1.1%.

- The MSCI Asia Pacific Index dipped 0.3%.

- The MSCI Emerging Market Index declined 0.5%.

Currencies

- The Bloomberg Dollar Spot Index rose 0.4%.

- The euro fell 0.4% to $1.1817.

- The British pound fell 0.2% to $1.3018.

- The Japanese yen weakened 0.3% to 105.03 per dollar.

Bonds

- The yield on 10-year Treasuries declined three basis points to 0.81%.

- Germany’s 10-year yield rose one basis point to -0.57%.

- Britain’s 10-year yield was little changed at 0.28%.

Commodities

- West Texas Intermediate crude declined 2% to $39.04 a barrel.

- Gold was little changed at $1,901.69 an ounce.

Share This:

COMMENTARY: 2025 Review of Global Energy Consumption – William Lacey