CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Higher oil prices set to trigger wave of deals as private sales accelerate

CALGARY, Alberta (May 13, 2026) — Enverus Intelligence® Research (EIR), a subsidiary of Enverus, the leading energy data analytics platform, has released its summary of recent U.S. upstream M&A activity and market outlook, highlighting a strong start to 2026 followed by a volatility-driven slowdown that is expected to reverse.

U.S. upstream deal value reached $38 billion in 1Q26, the highest quarterly total in two years, before activity slowed sharply in March amid increased crude price volatility. Despite the pause, higher oil prices are expected to accelerate a rebound in dealmaking, particularly by enabling more private E&Ps to pursue sales while supporting continued corporate consolidation.

“The market entered a temporary holding pattern as volatility clouded the outlook for oil prices, but the case for higher-for-longer oil prices is strengthening and creating the setup for an M&A rebound. We expect that to translate into more private companies coming to market, something we are already starting to see, and continued consolidation among public operators,” said Andrew Dittmar, principal analyst at Enverus Intelligence Research.

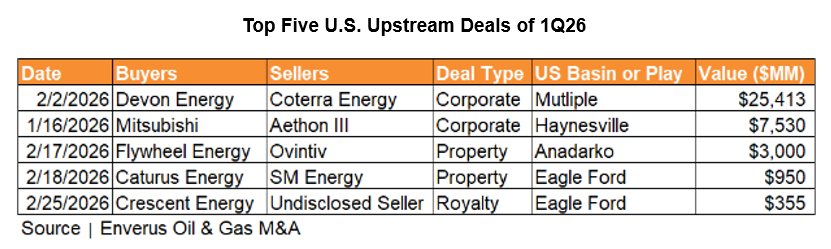

Activity in early 2026 was driven largely by corporate consolidation, including a $25 billion merger by Devon Energy and Coterra Energy that contributed about two-thirds of quarterly deal value. Over the past six months, total deal value exceeded $60 billion as the market continued to build momentum. However, transaction count declined in 1Q26, with only eight deals over $100 million recorded, tying a post-2020 low. The slowdown in volume reflects less active deal flow in March given uncertainty in oil markets once the Iran conflict commenced.

Buyer composition continues to evolve, with asset-backed securitization (ABS) financing playing a growing role in production-weighted acquisitions. Recent transactions underscore sustained demand from ABS-linked buyers, including Ovintiv’s $3 billion sale of Anadarko Basin assets in the first quarter to Flywheel Energy, a buyer that has deployed ABS financing in past deals. Diversified Energy’s recent $1.175 billion acquisition of Anadarko Basin assets from Camino Natural Resources was publicly linked to an ABS placement and demonstrates continued appetite for cash-flowing production from this buyer pool.

International capital remains active, particularly in gas-weighted regions. Gulf Coast-adjacent assets, including those in the Haynesville, continue to attract strong interest from Asian buyers, with Mitsubishi’s purchase of Aethon Energy for $7.6 billion highlighting this trend. Limited remaining Haynesville targets are likely to push buyers to evaluate alternative regions such as Appalachia despite infrastructure constraints, or even gassier portions of the Permian once a pipeline buildout helps alleviate extremely poor gas pricing in the region. Outside the U.S., Shell’s 2Q26 $16.4 billion acquisition of ARC Resources in Canada highlights renewed interest from European supermajors returning to the market as buyers, with its interest likely linked to the completion of LNG Canada Phase 1, with a final investment decision on Phase 2 pending.

Higher oil prices are also shifting seller behavior, increasing the likelihood of private sales. Better pricing is expected to encourage more private E&Ps to bring assets to market, including a handful of remaining targets in the Permian, while also making mature plays like the Eagle Ford and Williston significantly more economic to develop. Reports that Eagle Ford producer WildFire Energy is going to market, as well as the recent acquisition of Zavanna Energy by Kraken Resource in the Williston Basin, underscore this trend. Public companies that have participated in large-scale M&A, like ConocoPhillips, Devon Energy and SM Energy, are likely to take advantage of higher prices and a hot asset market to trim non-core portions of their portfolios.

Inventory pricing remains a central theme. Pricing for oil-weighted inventory remained resilient in 2025 even in a lower crude price environment, and rising oil prices are expected to further lift inventory values as buyers rush to secure remaining opportunities.

Looking ahead, EIR expects deal activity to follow historical patterns, where periods of volatility-driven slowdowns are followed by sharp recoveries once markets stabilize. A material shift in crude prices higher will add fuel to this rebound. “We are likely heading into another tsunami of consolidation as higher oil prices supercharge both private companies going to market and public E&P appetite for deals, both corporate consolidation and private asset sales,” added Dittmar. “This, combined with strong appetite from private capital, both ABS and traditional private equity, this sets up the market for a very busy rest of the year.”

EIR’s analysis pulls from a variety of products including Enverus ONE®.

Share This: