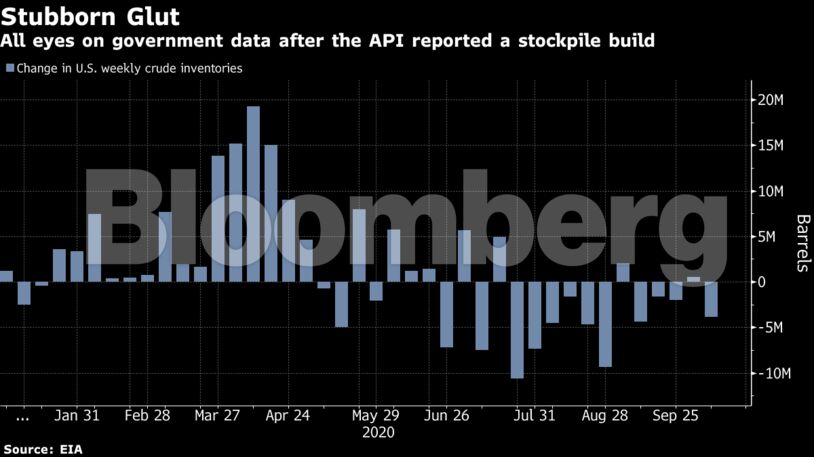

(Bloomberg) Oil dropped after an industry report pointed to a surprise increase in American crude stockpiles, countering optimism over a potential U.S. stimulus agreement. The American Petroleum Institute reported crude inventories climbed by almost 600,000 barrels last week, according to people familiar with the data. That contrasts with a stockpile decline forecast in a Bloomberg survey, before official figures later on Wednesday. Brent crude futures were 1.3% lower, reversing the previous session’s gains that were driven by hopes of the economic stimulus.

A resurgent coronavirus and expanding Libyan supply are keeping oil in check. While China is supporting demand, there are signs of weakening consumption in western Europe and OPEC+ has warned of a precarious market outlook. The coalition of producers will have to decide next month if it will stick with plans to raise production in January, or heed industry warnings about an imminent glut if it does so.

Brent “remains stuck in the low $40s with the weaker dollar and the potential for a stimulus having no positive impact,” said Ole Hansen, head of commodities strategy at Saxo Bank. The market is focusing on inventories, and “overall it makes sense that crude is struggling while the demand outlook remains murky.”

Get the Latest US Focused Energy News Delivered to You! It's FREE: Quick Sign-Up Here

Prices

Brent for December settlement lost 58 cents to $42.58 a barrel as of 1:37 p.m. in London, after gaining 54 cents on Tuesday

West Texas Intermediate for the same month fell 57 cents, or 1.4%, to $41.13

The November contract expired Tuesday with a 1.5% gain

Crude stockpiles at the American storage hub of Cushing increased by 1.17 million barrels last week, the API reported. That would be a fifth straight gain if confirmed by government data. Gasoline and distillate supplies declined, according to the API.

Other oil-market news:

The two most senior commodities executives at Morgan Stanley are leaving after compliance breaches linked to the use of communications tools such as WhatsApp, according to two people familiar with the matter.

Libya’s crude output will increase to 1 million barrels a day by the year-end, and will be at about 550,000 a day by the end of October, Reuters reported, citing an interview with Ahmed Maiteeq, deputy prime minister of the Government of National Accord.

The series of mergers reshaping the beleaguered U.S. shale oil industry accelerated Tuesday when Pioneer Natural Resources Co. agreed to buy Parsley Energy Inc. for $4.5 billion in stock, creating one of the largest producers in the Permian Basin.

CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

COMMENTARY: 2025 Review of Global Energy Consumption – William Lacey