CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Dean Foreman

Posted May 21, 2020

After crude oil futures prices plunged into negative territory for a day last month, there was a good deal of speculation that the same thing could happen this month. Some even pointed to the April futures meltdown as a “doomsday” scenario for U.S. natural gas and oil.

Well, a number of things happened on the way to oil’s “doomsday.”

At the outset, let’s note that what happened with futures in April didn’t repeat this month. Oil futures prices for June delivery of West Texas Intermediate crude, whose contracts expired Tuesday, closed at $32.50 per barrel – about 300% higher than they did for those contracts a month ago. Let’s explore why.

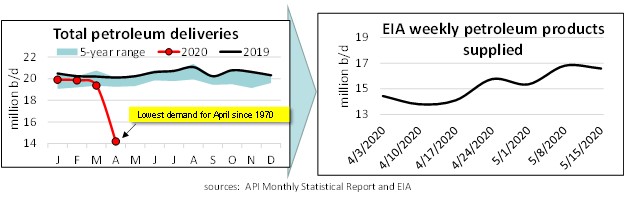

To start, demand for oil – actually, demand for key products made from oil, such as fuels – has increased as the majority of states now are at some stage of reopening. The U.S. Energy Information Administration (EIA) reports petroleum product demand rising to 16.6 million barrels per day (mb/d) the week ending May 15 from a low of 13.8 mb/d the week ending April 10:

Increased demand also has been reflected in crude oil storage decreases over the past two weeks – the shortage of which was paramount in last month’s futures price decline. Crude oil inventories declined to 526.5 million barrels (mbbls) for the week ending May 15, a decrease of 5.0 mbbls from the prior week. Stock building may have now ceased both due to lower oil production and the Strategic Petroleum Reserve (SPR) picking up another 2.9 mbbls last week for a recent total acquisition of 6.7 mbbls of crude oil.

Inherent in these data points and others is something we said last month – that even amid a sharp slide in futures prices in April, oil retained value. Indeed, as we see a quickening in economic activity, we’ve seen demand for fuels increase, because economic recovery requires energy. Global financial markets have also stabilized a bit, which has helped oil prices.

So that’s where we are. There could be more twists and turns as the U.S. and the world continue to cope with COVID-19, and the business climate for natural gas and oil remains challenging. Still, it appears the worst for industry as a whole may have passed – which is good for the country, because natural gas and oil are economic drivers that are fundamental to many other sectors as well.

To be clear, the actions of traders in futures markets generally help those markets diversify risk and increase liquidity. But these financial instruments always entail risk, as the U.S. Commodity Futures Trading Commission reminded market participants with a warning in the wake of April’s volatility.

The circumstances in April have never occurred before, and the fact that the WTI futures contract for May delivery expired on April 21 at a positive value of $10.01 per barrel and also avoided a return to negative prices through May 20 showed that participants have learned and adapted even during these extraordinary times, which really is the strength and differentiating characteristic of U.S. domestic markets. Resilience by any other name …

About The Author

Dr. R. Dean Foreman is API’s chief economist, specializing in energy and global business. With a Ph.D. in economics from the University of Florida, he came to API from Saudi Aramco Strategy & Market Analysis in Dhahran, where he managed short-term market monitoring and the long-term oil demand outlook. Foreman has more than 20 years of industry experience in corporate strategic planning, forecasting, finance / risk management and regulatory policy at ExxonMobil, Talisman Energy and Sasol North America.

Share This: