CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By James Thornhill and Alex Longley

Decisions at the online gathering will form the basis of Friday’s discussions on further contributions from G-20 nations, with U.S. involvement seen as key.

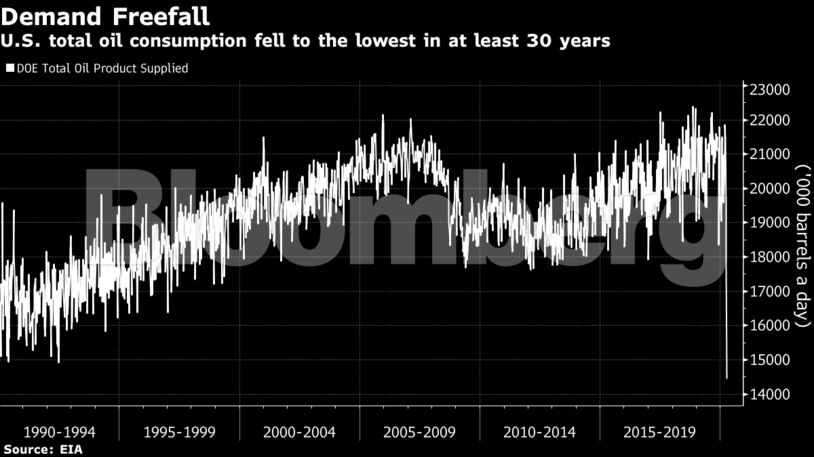

Major producers are scrambling for a deal as energy consumption has plummeted and hammered prices. Oil demand in India has collapsed by as much as 70% and some American refineries face closure as consumption fell to the lowest in at least three decades. Producers will need to agree on a deep and prolonged supply cut, or risk crude falling back again.

“The market is already pricing in a deal,” said Amrita Sen, chief oil analyst at Energy Aspects, in a Bloomberg TV interview. “Once the dust settles the demand declines are still bigger than the supply shortfall.”

See also: Global Oil Deal in Sight After Russia Signals Readiness to Cut

All but one of 26 analysts, traders and refiners surveyed by Bloomberg forecast that a production cut will be agreed this week, with the average of their estimates at 8.5 million barrels a day. While that’s a vast decrease, it would pale in comparison to the demand loss that some gauge is as much as 35 million barrels a day.

| Prices: |

|---|

|

While the anticipation of a production agreement has pushed prices slightly higher, WTI crude is still down more than 55% this year. That is giving India an opportunity to bolster its strategic reserves, while South Korea has said it will expand its storage this year.

OPEC and its allies, and the G-20, face a huge task in trying to drain the large oversupply. But there are signs that the market is banking on improved balances down the line. Volatility for the second half of 2020 has fallen sharply in recent days, indicating that the market has faith in OPEC+ restoring price stability, brokerage Marex Spectron wrote in a report.

Share This: