CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Sam Potter, Anchalee Worrachate and Justina Lee

In that time, tens of trillions of dollars of value was wiped off global stock gauges, corporate borrowing costs exploded, and access to short-term funding all but evaporated.

It was nothing to what was happening in the real world. On Feb. 19, when the S&P 500 Index was at its peak, the U.S. had about a dozen confirmed cases of the coronavirus. Now America has the highest number of infections in the world and more than 1,000 dead.

That global markets just had a decent week despite all that can make chronicling their progress seem like a callous undertaking. Asset prices move according to their own logic — maybe the best thing that can be observed right now is they are often clues to the future. Just like in the real world, extreme measures have been taken to contain their fallout. This week investors got their first clues as to whether it is working.

Based on coverage from across Bloomberg News, this is the story of another five days of history unfolding on Wall Street and beyond.

‘Sell Everything’

Monday 23 March: The Senate is stuck. Republicans are trying to rush through an emergency package to rescue the American economy from the impact of the pandemic and the measures needed to contain it. Democrats argue the bill as presented delivers a corporate bailout with poor oversight and not enough cash for hospitals.

All the while, confirmed virus cases climb alongside the death toll. With the rescue bill stalled, U.S. equity futures fall the most allowed in Asian trading hours. Most stock gauges in that region follow suit, as do those in Europe. Treasuries and the yen gain.

“A lot of what advisers are dealing with right now are clients saying why don’t we just sell everything and wait this out,” says Jeff Mills, chief investment officer for Bryn Mawr Trust in Berwyn, Pennsylvania. “Can we get back in when the dust settles? This is the question that we get every single week.”

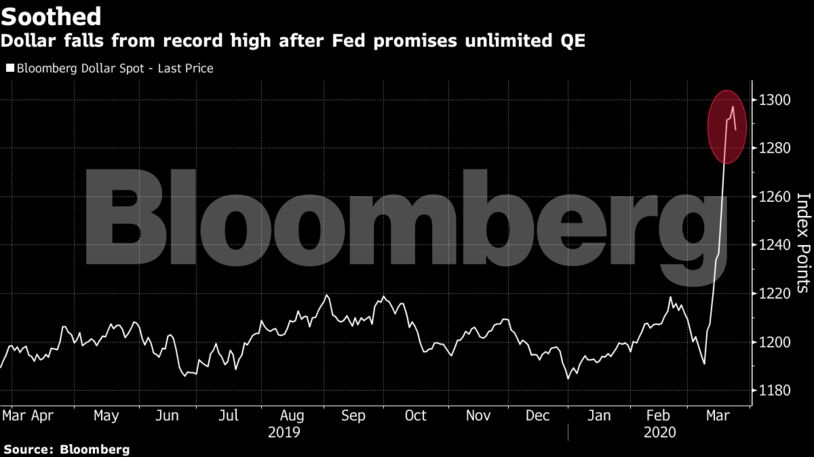

Washington may be paralyzed, but Jerome Powell and his colleagues are not. At 8 a.m. in New York, as many on Wall Street are arriving at their now-virtual desks, the Federal Reserve unleashes another wave of support for America’s battered economy. For the first time, the central bank says it will directly finance U.S. companies, and it promises to buy unlimited amounts of Treasury bonds and mortgage-backed securities.

The scale of the pledge is mind-boggling. It will take time for the markets to absorb it, but there are encouraging early signs. Funding tensions cool in the U.K. and euro area. There’s a decline in credit-default swaps, which provide protection in case a country or company fails to repay its debt.

It’s not much, but even glimmers of hope are important at this point. Everything the Fed has tried before today has failed to stop the pain spreading through the financial world. It has now reached the $16 trillion market for U.S. mortgages, which was at the heart of the last crisis.

Back then, these loans were exporting trouble as risky mortgages went bad — it was a financial crisis that spread to the real world. Now they’re on the receiving end, as the virus threatens both residential and commercial repayments and nervous investors try to pull cash from funds and vehicles that invest in the debt.

It is a real world crisis spilling into finance, and it is unquestionably getting worse. The U.K. bans all unnecessary movement of people for at least three weeks, joining the list of countries initiating lockdowns across Europe. The global death toll tops 16,000 as confirmed cases approach 400,000.

The collapse in consumer demand has been almost instantaneous, and today the line of companies slashing forecasts and cutting workers grows by the hour. A gauge of worldwide earnings revisions crashes to its all-time low. Economists say the U.S. faces the worst quarterly economic contraction on record.

This is why the Fed response has no precedent. In another first, the central bank says it will buy exchange-traded funds that invest in bonds. Those ETFs are going to have a very good day.

The notion of stimulus without end also spurs appetite for an asset that has proved its ability to store value for millennia, and gold jumps the most since 2016.

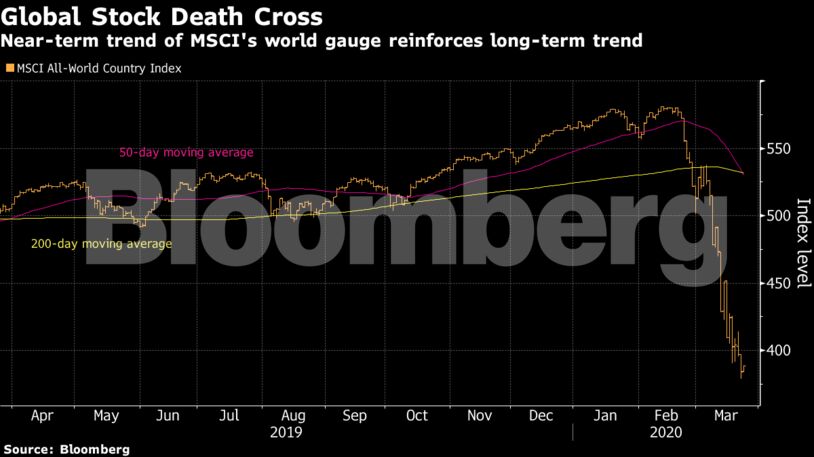

It seems nothing can lift the mood in stocks, however. By the end of the day, both the Dow Jones Industrial Average and an MSCI Inc. gauge of global stocks have posted a signal known as a death cross.

Technical analysis is a touchy subject in the financial markets; some swear by it, others at it. The main thing to note about these crosses is quite simple though — the 50-day moving average for each gauge is falling faster than the 200-day, which is also falling. In other words, the gloomy long-term trend has been accelerating.

One sliver of good news for those equity investors who need it: For the second trading day in a row, the index of expected stock volatility known as the VIX has fallen alongside the S&P 500. It could mean the most frenzied days of selling are behind us.

Lockdown, Limit Up

Tuesday 24 March: They call it “turnaround Tuesday” for a reason. S&P 500 futures are limit-up as the day begins, and it looks like being the third week in a row that the U.S. stocks will rebound strongly from a Monday slide.

That pattern could be important. It tells investors two things: First, there is no guarantee today’s move is the start of a meaningful rebound. Second, it isn’t necessarily being driven by the day’s news.

The headlines are supportive, however. China announces an intention to end the lockdown of Wuhan, the epicenter of the coronavirus. Despite bickering and delay, U.S. lawmakers are close to agreeing the rescue package for the world’s largest economy.

These are market positive, for sure. But there is evidence to suggest other, more technical processes could be behind this bounce.

Short covering is one. This occurs when investors rush to close their bets against equities, which they may be apt to do if more than $2 trillion in fiscal stimulus is hours away.

Another is a weakening of the loop by which price swings cause volatility-sensitive investors to adjust their portfolios, thereby creating more swings. The Fed actions have reassured some traders about what lies ahead. Selling has slowed. Expectations of more volatility are decreasing.

All of these and the promise of more stimulus help settle nerves. The dash to cash abates, relieving upward pressure on the dollar which in turn eases stress across a host of asset classes. The same feedback loops that helped fuel the violent sell-off in recent weeks begin to work in the opposite direction.

Pockets of market dysfunction live on, however. Both the S&P 500 and gold record their best day since 2008. Safe havens typically don’t rally on days when risk appetite is high.

Once again, thank the Fed. As well enhancing gold’s appeal as a store of value, the central bank’s actions are starting to alleviate the funding strains that had prompted traders to sell whatever they could to raise dollars. Investment flows have turned back toward the yellow metal.

At the same time, price discrepancies in the Treasury market are lessening. Even credit markets appear to be coming back from the brink, with new bonds being sold and measures of risk recording the first back-to-back declines since the meltdown began.

The Fed’s success is prompting calls for the European Central Bank to do more. Europe’s policy makers have acted, but not on the same scale, and tensions in the market and beyond are very high.

Data shows the amount of cash circulating in the euro area has increased by the most since the crisis. Back then it was believed to be people hoarding notes and coins in case of a bank collapse, but now the ECB puts it down to increased spending as they stockpile because of the virus.

Italy is worst hit, and now has the highest death toll in the world. Fabrizio Fiorini is working from his home in Modena after his office in Milan was closed. The chief investment officer of Pramerica SGA SpR lives close to the park, which not too long ago was full of families and happy children but is now empty.

“Coping with the tragedy that’s going on in Italy is far, far more difficult than dealing with the volatile market,” he says.

But Fiorini is feeling optimistic on both fronts. The Fed and ECB actions were the right ones, he reckons, and opportunities are emerging for money managers. The recession forecasts going around may be too pessimistic. Late on Monday Italy reported a decline in deaths for the second day running.

“The fall in the death rate in Italy is encouraging,” he says. “It gives hope that the tough measures taken by the government, painful as they might be, are starting to work. The Italian markets will probably recover soon. That will be a good message to others.”

Other investors share his optimism, it seems. Somehow equities shrug off data showing the biggest economic crisis in the euro zone’s history is underway, and European stocks post the largest gain since 2008.

It’s only after the markets close that Italy delivers the news that will be heart-breaking to Fiorini: The rate of deaths is rising again.

At about the same time, President Donald Trump is talking about re-opening the world’s largest economy within a month, against the advice of health professionals.

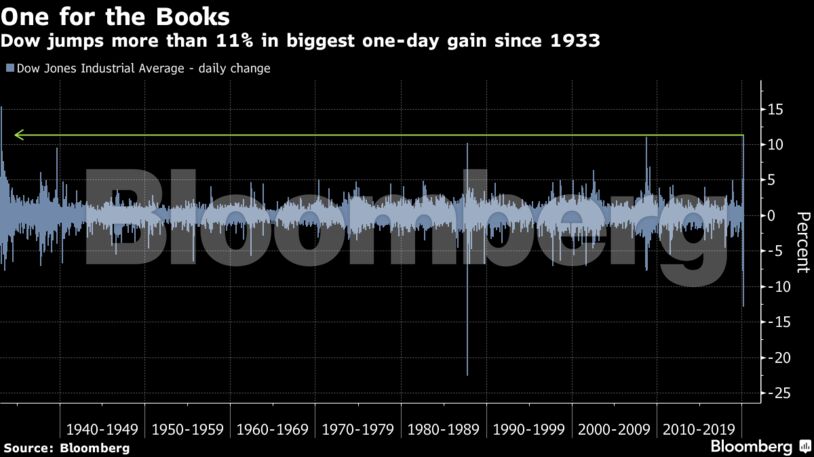

And the Dow Jones Industrial Average has its best day in more than eight decades.

‘No One Rings a Bell’

Wednesday 25 March: One question dominates every corner and conversation in the market: Have we bottomed out?

An extraordinary amount of focus is about to be expended on whether the S&P 500 can finish in the green for a second day, something it hasn’t done in six weeks — a lifetime ago, before this turmoil started.

“You don’t know when the dust settles, that’s the problem,” says Mills in Pennsylvania. “No one rings a bell at the bottom. It’s very difficult to make that call to get back in.”

This is the human side of markets, plain and simple. It doesn’t really matter much in the scheme of things whether U.S. stocks can rise for two days in a row. But psychologically speaking it has become important.

Equities have a lot of reasons to gain today. More than 2 trillion, in fact, which is the size in dollars of the rescue package agreed by U.S. lawmakers. No one knows if it is enough, but there has never been stimulus on this scale before.

Read more: What’s in Congress’s $2 Trillion Coronavirus Stimulus Package

The deal reverberates across assets. Big companies are issuing fresh debt as credit risk gauges extend a retreat. Municipal bonds, which started a rebound when the Fed pledged support earlier in the week, surge the most in three decades. The currency market looks like it is headed for calm.

Volatility in the world’s safest assets is declining, too. European equities cap their biggest back-to-back rally since the crisis. Bonds in the region also rally as the ECB scraps most of the limits of its bond-buying program to boost its firepower to fight the virus fallout.

“Things have calmed down,” says Athanasios Vamvakidis, head of G-10 currency strategy at Bank of America Merrill Lynch. “It’s too early to tell if this is a start of a turning point. We have to wait to see if the containment measures really work. It will be very important to see infection and death rates dropping.”

The signs are not encouraging. Spain suffers its deadliest day of the outbreak, with hospitals overloaded. Britain’s Prince Charles becomes the latest high-profile infection. German health authorities warn this is just the beginning as Europe’s largest economy mulls an additional stimulus plan.

There are tiny warning lights still flashing lights deep in the world’s financial machine. Those places that seem hard to reach, like the Japanese repo market, where rates hit a record. Or the high-yield market in Europe, which hasn’t seen a single new bond sale in a month. Or emerging markets, where investors stuck in illiquid bonds are dashing to protect themselves.

Demand for the greenback remains elevated. The three-month London interbank offered rate for dollars — a benchmark for securities around the world better known as Libor — rises for the ninth session in a row to the highest in three weeks.

The Fed’s measures were always going to take time to filter through the system. But right now the spread of U.S. high-yield bonds to Treasuries remains more than 1,000 basis points. The amount of debt trading at levels that most consider distressed has quadrupled in a week to nearly $1 trillion.

Late in the evening, the credit rating of Ford Motor Co. is cut to below investment grade by S&P Global Ratings because of turmoil in both production and demand within the auto industry. The 116 year-old American corporate icon and pioneer of mass manufacturing now falls into a category generally known in investment circles as “junk.”

Less than an hour earlier, the S&P 500, of which Ford is a member, closed in the green for a second day.

Three Days, 3 Million

Thursday 26 March: It’s claims day, when the U.S. government reports the number of people seeking jobless benefits. State filing systems have seen an exponential surge in applications, so investors are braced for bad news.

The price of containing the coronavirus is a blow to the economy the like of which has never been seen before — that is what central bankers and government are racing to cushion against. Yet with their trillions in stimulus and promises of unlimited support, they have created a dislocation between financial markets and the real world.

This will surely be the only day in history when the number of Americans claiming unemployment benefits is confirmed to have surged by 3 million in a single week and the S&P 500 finishes up 6.2%, capping the best three day gain since 1933.

“Call it a rally of hope,” says Robert Greil, chief strategist at Merck Finck Privatbankiers AG. “It’s predominantly driven by sentiment supported by central bank and government aid measures. It’s also partly a technical rebound like we’ve seen in the past in extreme crises.”

Read more: Technically Speaking, the Dow Just Rocketed Out of a Bear Market

The defiantly upbeat tone goes beyond stocks. The credit market sees 34 issuers in the U.S. and Europe selling a combined $64.8 billion of debt. Mortgage-backed securities are rebounding as the Fed scoops them up. The central bank is buying corporate bonds, too, fueling a dash for credit ETFs. A knock-on effect of this support in one part of the market is that selling pressure eases elsewhere, and spreads on some collateralized loan obligations are cut in half.

But in the age of the coronavirus there are some areas where neither monetary policy nor stimulus is likely to help. After three days of modest gains oil turns lower when the head of the International Energy Agency describes global demand as in “freefall.”

It’s not surprising — by some estimates about a third of the world’s population face restrictions on movement right now. Industry and travel have come to a standstill in many major economies. Crude producers are starting to run out of places to put the excess supply.

Demand for goods and services is cratering in virtually every industry and economic sector thanks to the pandemic. As a result, S&P Global Ratings and Moody’s Investors Service are downgrading U.S. companies at the fastest pace in more than a decade. That means higher debt costs and rising odds of a wave of defaults.

Late in the evening, the U.S. surpasses China as having the most confirmed infections in the world.

And the S&P 500 just closed at about the highest in two weeks.

What Goes Up

Friday 27 March: Most stocks in Asia rally following the third day of gains on Wall Street, but this is hollow stuff. Futures for the American gauges are down and Treasuries are up. Fatigue is setting in and appetite for risk is waning.

It looks like unlimited central bank support and $2 trillion stimulus will only go so far when U.S. virus cases are overtaking those in China and the economy is in turmoil. Investors don’t need a consumer confidence survey to tell them where things stand, but they get one anyway.

Read more: Consumer Sentiment in U.S. Slumps by Most Since October 2008

Updates on the virus are dreadful. In Italy, the deadliest day yet as almost 1,000 are lost to the outbreak. The U.K. reels as Prime Minister Boris Johnson and his two most senior health officials go into isolation with symptoms and the country’s death rate jumps 30%. Workers in the world’s food supply chain are falling ill. Mayor Bill de Blasio of New York, which accounts for about a quarter of U.S. cases, says new infections will be “astronomical.”

On and on. Portugal cases up 20%. The World Health Organization warns of looming catastrophes in Libya and Syria, which have limited capacity to respond to an outbreak.

In this torrent of miserable news, Congress approves the largest stimulus package in U.S. history and sends the measure for Trump’s signature. It causes hardly a stir in the stock market, which has been front-running the passing of the rescue package for days.

Credit risk gauges tick up again. Activity in the options market points to doubt over the Fed’s plan to prop up the commercial paper. Libor rises for an 11th day. These are not the signs of a market at peace.

Still, the charts will show this week was a win for the bulls, and for the policy makers who matched the market’s velocity with action that pulled it back from the brink.

In spite of the downbeat finish, the S&P 500 gained 10% and the Dow added 13%. Measures of corporate credit risk eased the most in years amid a deluge of new issues. The dollar had the worst week in a decade as the race to liquidate everything ended.

And the bears? They will shrug and recount the rallies just like this that have occurred in most major downturns. And perhaps they will point to the weekly gains that arguably matter most: Global coronavirus cases have more than doubled in seven days to well over half a million. The number of dead is up about 150%, to 25,000.

Share This: