CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Kevin Crowley and Kelly Gilblom

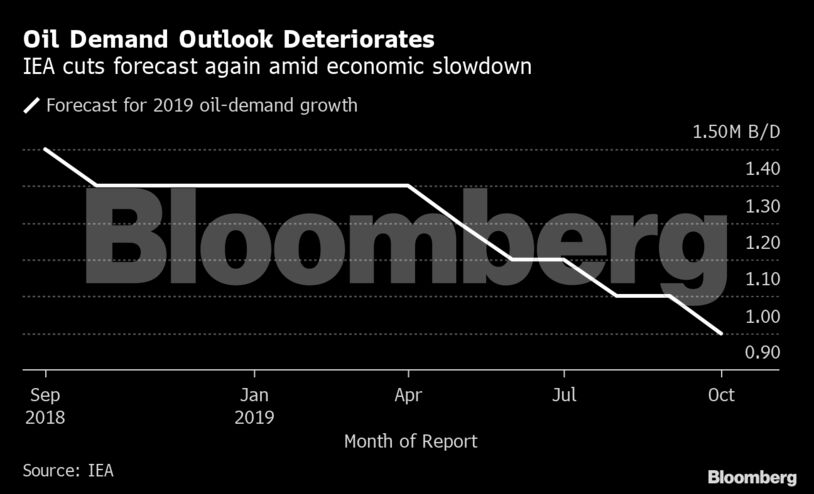

Exxon, Shell, and BP already have already taken steps to manage shareholder expectations by releasing limited data points on things like refinery repairs, asset sales and hurricane impacts on offshore oil production. Nonetheless, investors will be watching for additional color on what to expect for the remainder of 2019.

To make sense of all the moving parts in Big Oil’s earnings reports that start Oct. 29 with BP, look for these five things:

1. Surprises

Most of the bad news already should be priced in. Exxon fell 2.6% on Oct. 2 after disclosing a half-billion dollar hit from lower oil prices, a deficit that wasn’t plugged by improved refining profits.

Meanwhile, Shell warned that oil and gas output inched lower, and its refineries and chemical plants operated at about 90% of full capacity. BP warned that its tax bill rose, production declined, and it incurred an impairment on some assets it sold, factors that dampened hopes of an imminent dividend increase.

2. Petrochemicals

Long touted as Big Oil’s next high-growth opportunity, petrochemicals are languishing. The U.S.-China trade war has weakened demand for plastics amid concerns that $40 billion in planned U.S. Gulf Coast chemical plants will create a glut.

“Current trends continue to suggest a prolonged downturn” in chemicals, RBC Capital Markets analyst Biraj Borkhataria said in an Oct. 17 note. Exxon, with its giant chemical division, is the most heavily affected by this trend among peers.

What Bloomberg Intelligence Says

Chemicals may not recover materially from recent margin contraction, and overhang from oversupply amid economic slowdown is concerning.

–Fernando Valle, analyst

3. Growth

In a world awash in crude and confronted with climate change, growth is a major conundrum for Big Oil. Should these companies be expanding or winding down? Investors don’t seem to have a clear answer right now. Exxon’s stock has been punished adter the company spent too much on future projects while Chevron is regularly challenged on whether it has enough in the tank for growth after 2023.

Meanwhile there’s uncertainty whether Shell can match historic returns with investments in renewables and power, though earlier this month Total CEO Patrick Pouyanne declared the company has already achieved double-digit returns by selling electricity.

Don’t expect major pronouncements on such existential issues, but executives may offer clues to their thinking during earnings conference calls when they’re quizzed about 2020 spending and progress toward asset-disposal targets. BP’s call may get more scrutiny than most after it said earlier this month that longtime CEO Bob Dudley is handing the reins to upstream director Bernard Looney in February.

4. Shale

Exxon and Chevron each plan to more than triple production in the U.S. Permian Basin to 1 million barrels a day by the early 2020s. As for the European giants’ attitude toward shale, BP’s $10.5 billion acquisition of BHP Group Ltd.’s assets last year was a statement of intent.

Analysts will be keeping a close eye on how those companies avoid the pitfalls of smaller rivals stung by overambitious drilling programs, and how their performance stacks up against lofty targets. Despite the production boom, investors have soured on shale because of poor performance by independent producers that burned through nearly $200 billion of cash in the past decade.

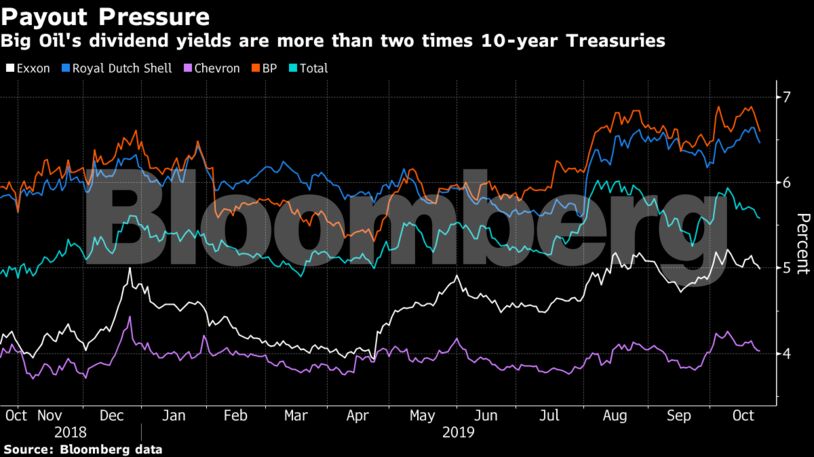

5. Dividends

The supermajors have long been among the stock market’s most generous dividend payers but in the new world of plentiful crude and anti-fossil fuel campaigns, increasing payouts and share buybacks are seen as key to retaining investors. Just as critical is whether the companies can afford them: the supermajors’ dividend yields this year surged to more than double the return on 10-year Treasury notes.

While none of the five companies’ dividend programs are in jeopardy, investors are keen to see how sustainable they are when balanced against costly drilling and construction projects, such as Exxon’s $30 billion-a-year spending program, and Shell’s investments in lower-profit renewable power.

Share This: