CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

It’s clear that a boom is following the bust, and the timing couldn’t be worse for the Saudi-led oil cartel.

By Javier Blas

Moving right along. Photographer: Mauro Pimentel/AFP/Getty Images

The Brazilian coffee and oil industries have something in common. Espresso connoisseurs know the country’s coffee production follows a natural biennial cycle, alternating periods of low and high output. One year, the trees funnel most of their energy into growing new branches; another, into producing fruit. The country’s oil industry also appears to follow similar cyclicality, even if arbitrarily. Disappointing years, when growth underperforms even the most pessimistic expectations, are quickly followed by spectacular expansion periods.

After a very poor 2024, the Latin American oil giant is entering one of those phases of rapid growth. On current trend, Brazil will become the second-largest source of incremental non-OPEC+ oil production this year, only behind the US and ahead of Guyana, the other South American oil star that typically gathers more attention, and Canada. The timing couldn’t be worse for OPEC+, already battling with an oversupplied market and falling prices.

For some time, the Saudi Arabia-led oil cartel has tried to pull Brazil into its orbit, knowing that the latter nation was becoming a huge rival to its efforts to keep oil prices inflated. But all OPEC+ overtures — to successive right- and left-wing governments in Brasilia — have failed. The most Riyadh has achieved is for Brazil to cement its freeriding status: Since February, it’s been a formal member of the group’s so-called declaration of cooperation, joining the likes of Russia and Kazakhstan, which formed an alliance with OPEC+ nearly a decade ago. But unlike them, Brazil isn’t bound by any production obligations. Effectively, it got everything it wanted: access, influence and intelligence about what other oil nations are up to without giving away anything. That the cartel accepted the deal speaks volumes about its desperation to keep ties with Brazil alive.

Source: IEA

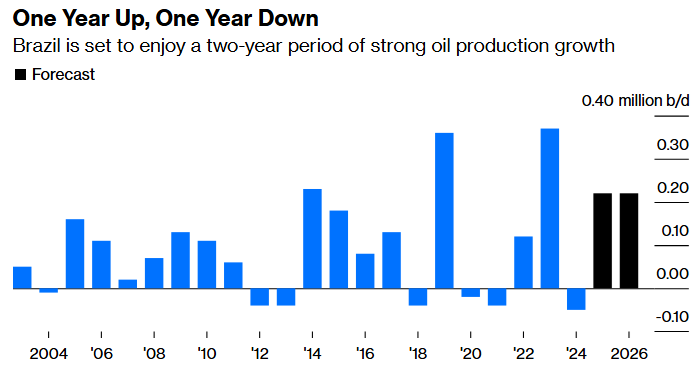

With friends like Brazil, OPEC+ doesn’t need any enemies. The Latin American nation will add about 450,000 barrels a day of extra production in 2025 and 2026, equal to about a quarter of incremental demand during the period. The increase nearly matches the record 490,000 barrels a day it added in the 2022-2023 period. With a bit of luck, Brazil may even post its fastest growth period ever.

Differing from the US shale industry, where low oil prices quickly translate in less drilling, Brazilian petroleum production is largely immune to short-term changes in oil prices. Whatever the cost of Brent in 2025 and 2026, the extra Brazilian barrels are coming. Only future projects, perhaps as late as 2028 and 2029, would be affected. For now, state-run Petroleo Brasileiro SA and its foreign partners plan to develop a string of offshore oilfields, including the multiphase Buzios oilfield, which is on track to become Brazil’s largest by output, overtaking Tupi. Other notable developments include the Mero and Bachalao oilfields, where Shell Plc, TotalEnergies SE and Equinor ASA hold stakes.

The oil market went into 2024 also holding high expectations for Brazilian output. But a combination of delayed drilling approvals due to a strike by environmental officials, supply-chain glitches and widespread maintenance meant that production fell to an annual average of 3.44 million barrels a day, down from 3.49 million in 2023. Excluding the period during the Covid-19 pandemic, it was the largest annual decline in at least 25 years.

Understandably, the events of last year meant the market felt some trepidation about betting that Brazilian output will grow this year. By now, however, it’s clear a boom is following the bust. The strike by officials at the Brazilian Institute of the Environment & Renewable Natural Resources, which President Luiz Inácio Lula da Silva has described as “a government agency that seems to be against the government,” ended last June, opening the door to drilling. Petrobras, as the national oil company is known, has largely solved its supply-chain problems, as it started to order kit well ahead of when it needs it. And the extended maintenance of last year means that Brazilian oilfields need less annual work this time.

Source: Bloomberg calculations based on IEA and UK Energy Institute data

The result is that — to the surprise of the most cautious observers — Brazil has this year brought new oilfields into production not just in time, but also ahead of schedule. Last month, Petrobras and its partners recently announced the first oil from a new facility at the Mero field, compared with an initial guidance that pointed toward the end of the year. First oil from the Bacalhau field also appears imminent, slightly ahead of schedule.

Still, there are risks. Brazil must run rather fast to stay still. With a base production decline rate of more than 10% a year due to aging oilfields, the nation needs to add two new so-called floating production, storage and offloading units every year simply to keep output unchanged. Each is a marvel of engineering, measuring more than 350 meters (1148 feet) long by 65 meters wide, about the size of the US largest aircraft carrier.

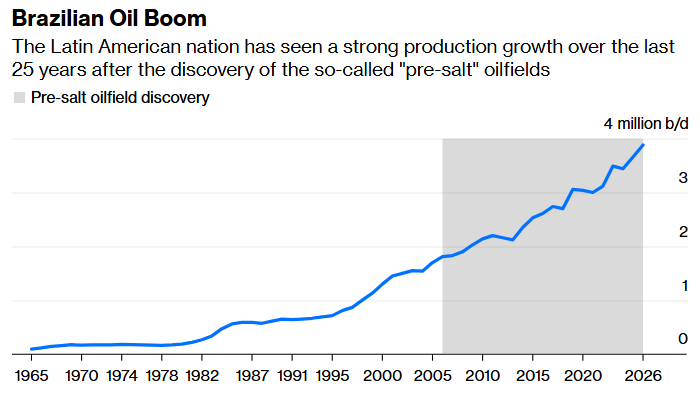

But if all those monsters of the seas come online on time, Brazilian monthly oil output will surpass the record high set in late 2023 at some point this summer, likely in August or September. By the middle of 2026, the country’s output is likely to top the 4 million barrels a day mark for the first time. At that level, it would rival every OPEC+ member other than Saudi Arabia, Russia and Iraq. Perhaps the cartel wasn’t trying to lure Brazil into its orbit but was following the old axiom of war: Keep your friends close and your enemies closer.

This column reflects the personal views of the author and does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Share This: