CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Two key findings from BP Plc’s annual deep dive on global energy statistics are that renewable electricity has grown at an extraordinary clip in the past two decades, and it still has very far to go. Solar and wind have expanded by orders of magnitude and now make up more than 10% of global electricity; that also means that these two technologies need to scale up market share by several factors — as the electricity system as a whole grows too — in order to decarbonize power substantially.

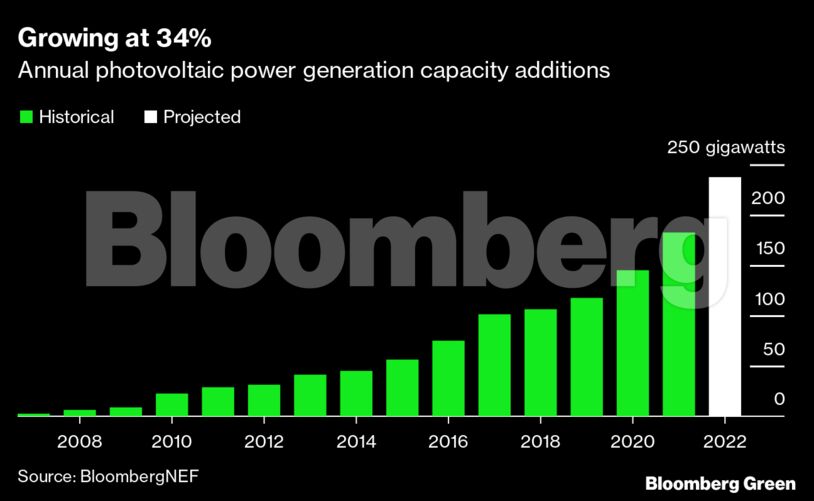

Of the two, solar is the smaller contributor, but with the faster growth rate. And what a growth rate it is. Since 2007, annual installations of photovoltaic power generation have grown from 22 gigawatts to about 240 gigawatts expected this year. That’s a compound rate of 34.5%, meaning it takes barely more than two years for annual installations to double, on average.

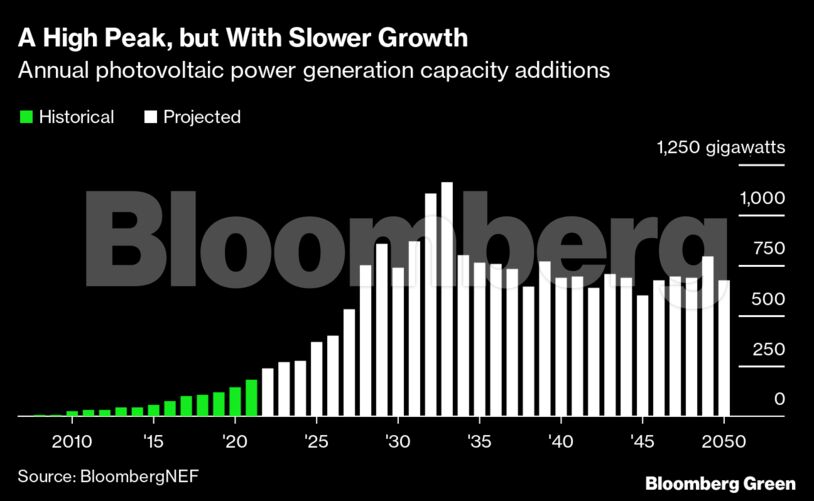

Historical growth pales in comparison to projected solar installations in BloombergNEF’s most renewables-intensive scenario for decarbonization. In that scenario, solar installations will peak more than four times higher than they are today, at more than a terawatt a year (about one-eighth the generation capacity of the global electricity system today). The pace of installations will slow by the middle of the century, but still are more than double what BloombergNEF expects in 2022.

This looks daunting — but is it really? The compound growth rate needed to meet the absolute peak in annual installations in 2033 is 15.5%, less than half the actual rate in the past 15 years. To put it another way: Reaching that annual installation target would require halving solar’s growth rate. This may seem counter-intuitive — doing much more does require more effort — but it actually requires a slower rate of growth.

Understanding that a slower growth rate is needed also makes the task less daunting because it allows us to extrapolate from the key factors that could determine actual solar growth.

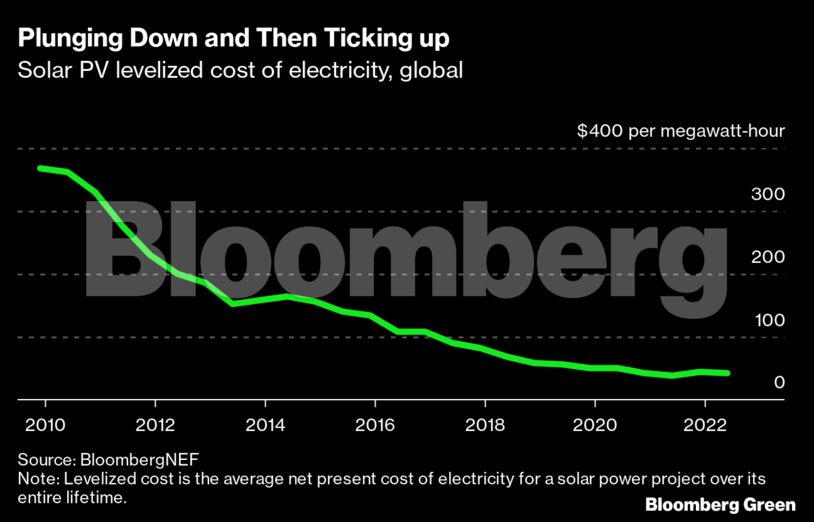

The first factor is the cost of electricity generated by installed solar power. It has gone up in the past year, thanks to commodity prices and general inflation. Even as solar costs have ticked up, solar is still lower-cost than coal- or gas-fired power. And with fuel prices rising, the gap between lowest-cost wind and solar, and coal and gas-fired power, is widening.

Land availability is another controlling factor, naturally. That said, the US could install more than 450 gigawatts of residential solar on its own. And as BloombergNEF’s Jenny Chase routinely notes, the land occupied by US golf courses could host 370 gigawatts as well.

The biggest controlling factor in the near term is probably manufacturing. It might not be quite where you think, however.

The largest companies assembling solar modules now have 50 gigawatts of capacity each, and plan to expand further this year. Each new assembly plant is bigger and more sophisticated than the one before it, and companies routinely replace plants that are less than a decade old in favor of greater automation and greater scale as a matter of staying competitive. Assembly isn’t likely to be a constraint on the solar industry in the future.

It is the production of polysilicon, the semiconductor material used for more than 90% of the world’s modules today, which is the biggest controlling factor. While there are hundreds of PV module assembly facilities, there are only a few dozen polysilicon production plants. Those plants are expensive to build, and they are also highly exposed to energy costs. Even there, though, today’s existing capacity is sufficient for more than 300 gigawatts of module manufacturing.

And as of May, there is almost double that much production capacity announced or under construction. If all of that capacity materializes (which is a bit of an “if,” given how much it is), it would add a further 600 gigawatts of annual polysilicon manufacturing capacity. That isn’t far off the more than 1,100 gigawatts of annual installations which BloombergNEF projects, in the most aggressive scenario, for 2033.

Ask any long-term energy or technology modeler about their state of mind when looking out several decades, and they will probably tell you that it toggles between imagination and disbelief. Imagination is often just an extrapolation of trend; disbelief is a cautious mind almost always saying “there is no way this trend can hold.” Solar’s math for 2050 might seem imaginative, but it really isn’t. As imagination goes it’s quite conservative. It’s mostly extrapolating from today’s extant reality while allowing for growth to slow, not increase. Solar, then, is a case where the modeler’s disbelief isn’t about allowing for more aggressive scenarios. It’s about the opposite: Acknowledging that a much slower rate of expansion can hit the mid-century mark.

Nathaniel Bullard is a senior contributor to BloombergNEF and Bloomberg Green. You can email him with feedback.

Share This: