CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

After a short meeting on Monday, ministers ratified a 400,000 barrel-a-day supply hike for November. While the cartel was simply sticking to its well-established plan to gradually roll back output cuts, traders reacted with alarm, pushing crude to the highest in almost seven years in New York.

After a relatively quite summer, oil is now joining natural gas, coal and a host of other vital commodities in a potent rally that threatens to upend the world’s recovery from the coronavirus pandemic by spurring inflation and disrupting industries.

The Organization of Petroleum Exporting Countries and its allies aren’t standing idly by while this happens. They already boosted production by almost 2 million barrels a day this year — about 2% of world demand — and have promised to add 400,000 barrels a day each month until September 2022.

Yet the incremental approach the cartel agreed back in July sits increasingly uneasily alongside a spiraling global energy crisis. In the governments and central banks of the world’s largest economies, there’s palpable anxiety about the coming winter.

“It’s not that OPEC+ does not recognize the coming supply shortage,” said Bjornar Tonhaugen, head of oil markets at Rystad A/S. “The group is well aware of the global inventory draws, maintenance work and rising demand, but chose to wait until later this year to adopt a bolder supply approach.”

Going into Monday’s OPEC+ talks, there had been speculation that the cartel could opt for a larger supply increase. There was widespread anticipation “that it was going to be an 800,000 barrel-a-day temporary boost in November,” said Rob Thummel, a portfolio manager at Tortoise, a firm that manages roughly $8 billion in energy-related assets.

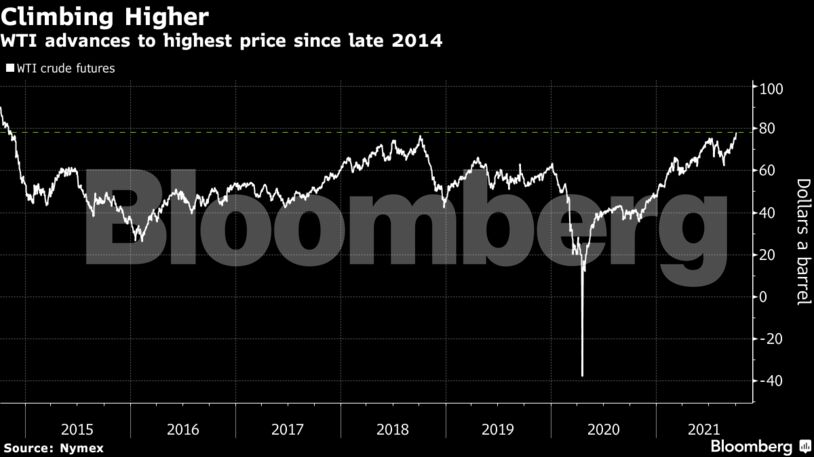

However, no such proposal was made, OPEC+ delegates said, asking not to be named because the meeting was private. When it became clear that the group wasn’t going to give any extra, West Texas Intermediate crude jumped as much as 3.3% to $78.38 a barrel in New York, the highest since November 2014.

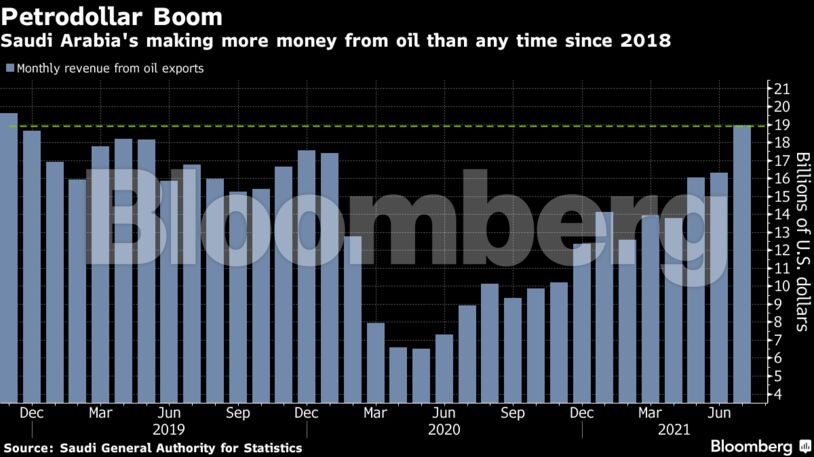

Despite the misplaced expectations, the current oil market is looking good for OPEC+. Crude is trading at multiyear highs without prompting a surge in rival supplies. Saudi Arabia’s oil revenue is the highest since 2018.

All this means the kingdom is “keen to tweak the current OPEC+ deal of monthly increases as little as possible,” said Amrita Sen, chief oil analyst and co-founder of consultant Energy Aspects.

Getting every member of the 23-nation coalition to agree to the current output policy was no mean feat. The deal was forged in a series of acrimonious meetings that exposed deep fissures between Saudi Arabia and the United Arab Emirates — two of the group’s closest allies.

That long ordeal was the climax of more than a year of tumult and hardship — from a historic slump triggered by the pandemic to a vicious price war between Russia and Saudi Arabia.

Yet the delicate balance that OPEC+ has achieved is at risk due to spillover from external crises.

The shortage of natural gas, which has sent prices of the fuel to the equivalent of $190 a barrel, is spurring a switch to oil products for heating and manufacturing. That trend could boost overall demand by about 500,000 barrels a day, according to Amin Nasser, chief executive officer of Saudi state oil company Aramco.

At the same time, U.S. oil production is still struggling to recover from Hurricane Ida, which has knocked out a total of almost 35 million barrels after slamming the Gulf of Mexico a month ago. That’s the equivalent to almost two full months of OPEC+ supply increases.

Goldman Sachs Group Inc. said its base case is for Brent crude to rise as high as $90 a barrel, from about $81 currently, Damien Courvalin, the company’s head of energy research, said on Bloomberg TV. Oil inventories are about to reach the lowest in 10 years, he said.

See also: OPEC+ Should Worry About Shortfalls, Not Surpluses: Julian Lee

In this environment, the oil market is looking to OPEC+ for guidance, but there was no press briefing after the meeting.

“We anticipated the group would signal prices may have overreacted lately, or that it would indicate crude exports from the Middle East are likely to increase over the coming months,” said Giovanni Staunovo, a commodity analyst at UBS Group AG, said in a note. “But neither issue was addressed.”

There’s little sign so far of the kind of political pressure that could get the cartel to change course. Before Monday’s meeting, Washington told Riyadh it was satisfied with the current pace of OPEC+ supply hikes, a U.S. official said, asking not to be named because the talks were private. The Americans did make clear that they want the group to remain attentive to the market, particularly any spillover from natural gas, said the official.

“OPEC+ have to be careful not to allow prices to inflate too much,” said Rystad’s Tonhaugen. “Otherwise we may see an adverse reaction that could negatively impact post-pandemic economic growth.”

Share This: