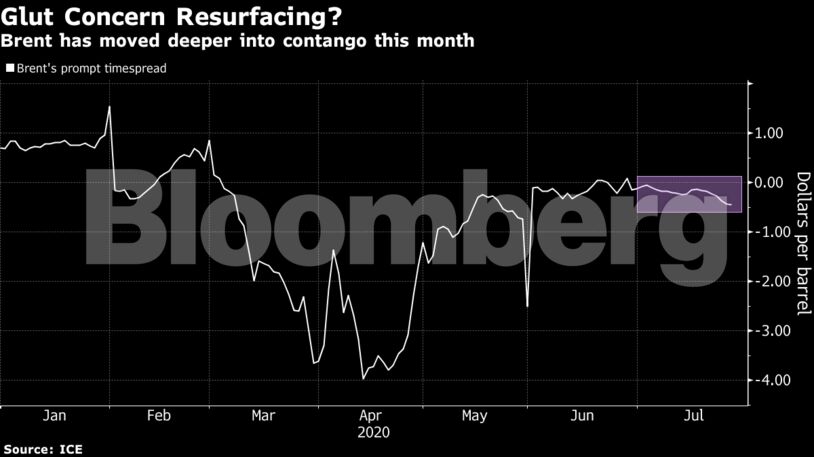

(Bloomberg) Oil slipped to near $41 as investors weighed worsening relations between Washington and Beijing alongside flare-ups in coronavirus outbreaks across the world. Futures in New York edged lower after a 1.7% gain last week. Chinese authorities took over the U.S. consulate in Chengdu on Monday as tit-for-tat tensions continue to simmer between Beijing and the U.S. At the same time, second waves of the pandemic are popping up from Spain to China, casting new potential clouds over the demand outlook, though the surge in cases in the U.S. was easing.The most notable market moves in recent days have come in the shape of the oil futures curve. Brent’s prompt spread is trading in its largest contango structure since May, a sign of oversupply, while contracts based on the value of Russian and North Sea crude were both weaker last week. Its the latest signal that the market’s re-balancing appears to have taken a pause for breath in recent sessions.

Crude has been trading in a tight range near $40 a barrel since early June after its rapid recovery from lows in April petered out as many countries struggled to bring the virus under control. A drop in the dollar has also supported prices this month, although investors are bracing for fresh supply from the OPEC+ alliance when it relaxes its output curbs from August.

“On the one hand, the risks of a less robust recovery of demand due to coronavirus, and the political tensions between the US and China, are weighing on prices,” said Commerzbank AG analyst Carsten Fritsch. “On the other, prices are finding support from the weak U.S. dollar and hopes of further corona aid.”

Get the Latest US Focused Energy News Delivered to You! It's FREE: Quick Sign-Up Here

Prices

West Texas Intermediate for September delivery fell 0.2% to $41.23 a barrel as of 10:42 a.m. in London

Brent for September settlement declined 0.2% to $43.27

The pace of the recovery in global oil demand is set to slow to below 1 million barrels a day from August through December, Goldman Sachs Group Inc. analysts wrote in a report. That stalling return is likely to leave crude prices range bound in the second half of the year, they said.

There is also evidence North American crude production may be starting to recover. U.S. output rose for the first time since March in the week through July 17 after correcting for the impact of Tropical Storm Cristobal, which tore through the Gulf of Mexico in June, while Baker Hughes Co. data released Friday showed the first expansion in drilling in American fields in four months.

Other oil-market news

Reliance Industries Ltd. toppled Exxon Mobil Corp. to become the world’s second-largest energy company after Saudi Aramco as investors piled into the conglomerate lured by the Indian firm’s digital and retail forays.

Money managers have increased their bullish Nymex WTI crude oil bets by 5,564 net-long positions to 362,500, weekly CFTC data on futures and options show. The net-long position was the most bullish in three weeks

CDN NEWS |

CDN NEWS |  US NEWS

US NEWS