CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Laura Hurst

Since the pandemic started, BP Plc and Royal Dutch Shell Plc have made drastic changes to their businesses, from multibillion dollar writedowns to big cuts to dividends and jobs.

They explained these moves as responses to the dual threats of the lockdown-induced oil slump and the growing pressure to cut carbon emissions. Yet the decisions say as much about the companies’ individual fragility as they do of the challenges faced by the broader industry.

The current crisis, according to some analysts and investors, has given BP and Shell the chance to clean house by reducing onerous shareholder payouts or adjusting unrealistic price assumptions.

“The BP announcement ‘kitchen sinks’ it, so that long-term investors can step in with much of the worst in the rear view mirror,” said Thomas Hayes, managing member of investment management firm Great Hill Capital LLC.

Difficult Decisions

BP announced on Monday the biggest writedown on the value of its business since the Deepwater Horizon disaster a decade ago. That came a week after the company said it would cut 10,000 jobs.

Chief Executive Officer Bernard Looney said the moves were necessary because oil and gas prices will be lower than expected in the coming decades as the coronavirus hurts long-term demand and accelerates the shift to cleaner energy.

His counterpart at Shell, Ben van Beurden, blamed the same factors for his difficult decision to cut the company’s dividend for the first time since the Second World War. Several analysts and investors predicted BP will do the same before the current crisis is over.

“There has to be a chance that Mr Looney is softening up BP shareholders for a dividend cut,” said Russ Mould, investment director at AJ Bell. “If investors really do buy into the new carbon-neutral strategy then they may be relatively forgiving of a reduction in the annual distribution, especially given the fall in oil and gas prices seen this year.”

Too High

The coronavirus pandemic and the push to cut carbon emissions each have the potential to reshape the industry, but some problems predate those twin crises.

In Shell’s case, investors were already questioning the affordability of a $15 billion annual dividend for a company that also planned to make make massive investments in clean energy.

BP faces a similar challenge, plus a few other longstanding vulnerabilities.

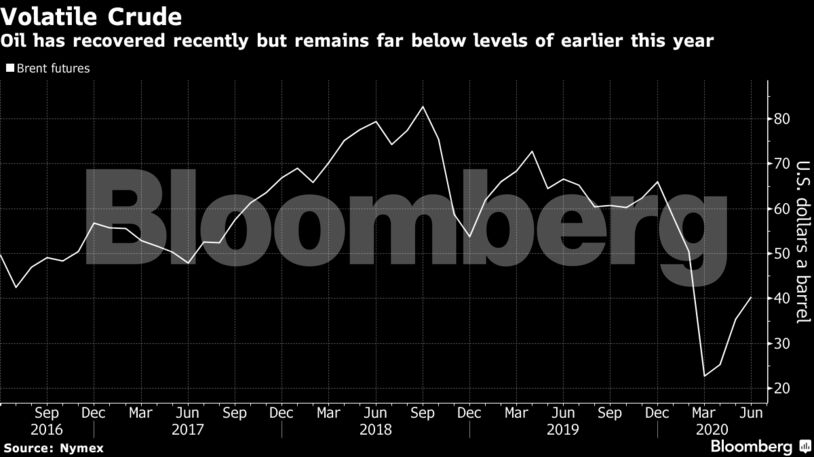

The company revised its 2021-2050 price assumptions to $55 a barrel for Brent crude and $2.90 per million British thermal unit for U.S. natural gas. Its previous long-term expectations of $75 for oil and $4 gas were already too high compared with prices in the last few years, said Allen Good, an equity analyst at Morningstar.

“In this light, the impairment charges are of little surprise,” said Good.

But BP’s assumptions aren’t the highest among its European peers. Norway’s state-controlled Equinor ASA, which has cut its dividend, assumes Brent prices of $80 a barrel for 2030. It was last updated in the third quarter of 2019 and are tested on a yearly basis against the International Energy Agency’s scenarios, the company said.

Italy’s Eni SpA has a long-term price of $70, which has remained unchanged “for the last few years,” according to the company’s latest annual report. France’s Total SA sees crude at $70 in the middle of this decade, falling to $50 by 2050.

BP, however, has also been carrying a heavier debt burden than its rivals. After the writedowns, its gearing — the ratio of debt to equity — would increase to 48%, by far the highest in the industry, according to RBC Capital Markets analyst Biraj Borkhataria.

Every company is grappling with long-term shifts in energy consumption and prices, and the recent announcements by BP and Shell are a genuine response to that challenge.

“Big picture, we see this as another step in the re-rating of oil and gas, and the journey from Big Oil to Big Energy,” said Luke Parker, vice president of corporate analysis at Wood Mackenzie Ltd.

But not all of the oil majors have the same urgent need to adapt.

BP’s “peers have more options and time to survive the current environment without a dividend cut,” Borkhataria said.

Share This: