CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Alex Longley

The coalition will hold a meeting of its members by video conference on Monday. It will be open to all producers — not just members of the Organization of Petroleum Exporting Countries or its allies — though it’s still not clear who will attend, according to delegates.

A delegate said a global cut of 10 million barrels a day is a realistic goal. Russian producers are ready to participate, people familiar with the matter said.

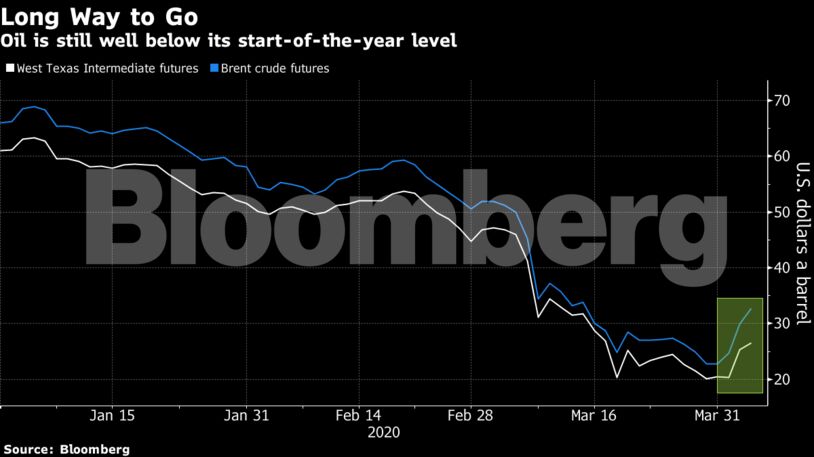

Every corner of the market has rallied over the last 24 hours, from timespreads used to gauge market health, to key North Sea swaps.

The announcement first came from President Donald Trump on Thursday, driving Brent $10 higher at one point. But those gains subsequently ebbed away in the face of the mammoth task for the producers.

See also: Trump’s Push for Huge Deal to Cut Oil Supply Draws Disbelief

Getting countries from all over the world to agree would be a tough ask. Even if that’s successful, an output reduction of the size that’s being discussed will be just a fraction of the 35 million barrels of daily demand destruction some traders now see.

Citigroup Inc. and Goldman Sachs Group Inc. have argued any supply deal would anyway be too little, too late as demand craters due to efforts to stem the coronavirus.

“There does appear to finally be collective acceptance that the market is in such an extraordinary state of oversupply that coordinated action is needed,” said Callum Macpherson, head of commodities at Investec Bank. “Given how difficult it is for OPEC+ to agree on a position, how they will manage to successfully coordinate with the U.S and other countries remains to be seen.”

| Prices: |

|---|

|

The guest list for Monday’s meeting will be crucial as Saudi Arabia has made clear it will only cut production if others, including the U.S., shoulder some of the burden. While Trump tweeted Thursday that he had spoken to Saudi Crown Prince Mohammed bin Salman, who had in turn spoken with the Russian president, a person familiar with the situation said the U.S. leader’s goal is purely aspirational and will ultimately hinge on whether Riyadh and Moscow can reach a deal.

The physical oil market continues to be weak, giving producers more urgency to react. Belarus said Russian companies are offering Urals oil for $4 a barrel. Crude in the Bakken region of the U.S. is still only worth $12 a barrel.

Share This: