CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Kevin Crowley and Rachel Adams-Heard

How well shale producers will cope with this latest headwind will be a key question as quarterly earnings come out over the next few weeks. The industry also faces pressure from Wall Street to act on climate change, something BP Plc tried to address Wednesday with its pledge to cut carbon emissions.

“North America is full of companies that, on the E&P side, probably shouldn’t be here anymore,” said Marcel Hewamudalige, a Houston-based managing director at Evercore Group LLC. “There’s too much debt in the system and those guys won’t survive.”

The shale revolution unlocked previously inaccessible reserves of oil and natural gas, making America’s production of both the highest in the world. But that abundance has also helped create a global glut, keeping a lid on prices.

What’s more, the shale sector has found itself on a treadmill. Fracked oil and gas wells experience steep declines in their production compared to conventional wells, compelling shale producers to keep drilling simply to maintain output levels and cash generation, even in the face of stagnant prices.

That approach has seen the industry build up a formidable level of debt, an increasing concern for investors. Dozens of drillers went bankrupt and the capital markets are now pretty much closed for all but a few companies able to offer junk bonds. The U.S. E&P sector was one of the worst stock market performers last year amid doubts about its ability to achieve sustainable cash flows.

Consolidation may not happen anytime soon, as the M&A market is “broken,” according to Kyle Kafka, a partner at energy private equity firm EnCap Investments LP. Halliburton Co. and Schlumberger Ltd., the two biggest oil services companies, have said U.S. shale’s best days are behind it.

For many in Texas, a slowdown is already apparent. Permian employment has lagged state job growth for the first time since 2016, according to the Dallas Fed.

Still, the gloom in the Lone Star state isn’t reflected in overall U.S. output. The country is producing about 13 million barrels of oil a day, 9.2% higher than a year ago, according to the Energy Information Administration, which expects a further 1 million barrels of additional output this year. Other forecasters are less bullish, but the consensus seems clear: More oil is coming.

“The death of shale has been wildly exaggerated,” said Leo Mariani, an analyst at KeyBanc Capital Markets.

The history of American wildcatters is littered with boom-and-bust cycles, from the post-war, demand-driven expansion, through the OPEC crisis in the 1970s to the steep drop in prices during the 1980s and 1990s. But in contrast to most of those industry shocks, the current one has been unfolding slowly as investors become increasingly unwilling to fund small explorers.

Much of the current production growth is coming from the industry majors, with Exxon Mobil Corp. and Chevron Corp. ramping up output at a startling rate in the Permian. Their huge balance sheets allow them to sustain investment through entire price cycles.

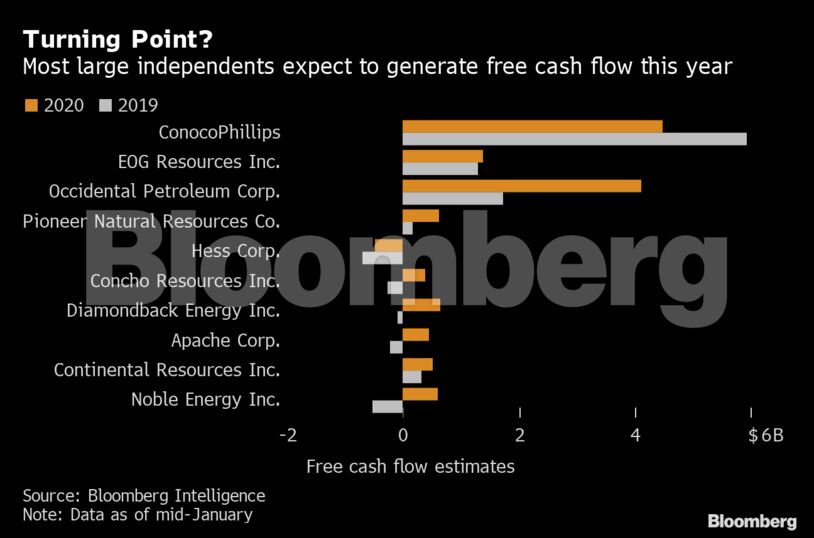

Independent U.S. operators are more vulnerable. Even the biggest in that group are trying to moderate spending while still promising investors annual production growth of more than 10%. They include names such as EOG Resources Inc., Pioneer Natural Resources Co. and Diamondback Energy Inc., which are all scheduled to report earnings later month.

Some, like EOG and ConocoPhillips, are so far managing to walk the tightrope and generate consistent free cash flow. “They cannot veer from that course,“ said Regina Mayor, global head of energy for KPMG.

The real pain is being felt among the small and mid-size publicly listed operators and private-equity backed players. Many of them were established in the early to mid-2010s when the emerging potential of fracking and horizontal drilling, combined with low interest rates and easy access to capital, fueled a land grab.

Those who got out at the right time made fortunes, like wildcatter Floyd Wilson, who raked in $12 billion selling his company to BHP Group Ltd. But for many other producers, the music has stopped, leaving them highly indebted and with a higher cost of capital than their peers.

“The founders of the shale revolution were businesses constructed to focus on finding the best assets, the best resources and flipping them for premium dollars,” Evercore’s Hewamudalige said last month at the Independent Petroleum Association of America’s Private Capital Conference in Houston. “This trend that we saw the last decade made a lot of people in this room a lot of money, but it’s changing.”

Fed up with years of poor returns from the U.S. energy sector, investors now want shale companies to produce cheaply, generate cash and hand it back to them. The ability to produce from shale rock means oil and gas are “essentially infinite” and so the market places little value on reserves, said Ken Hersh, the former chief executive officer of private equity firm Natural Gas Partners.

“There’s no more E in the E&P business,” he said. “Exploration is a thing of the past.”

Share This: