CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Oil extended declines as the International Energy Agency highlighted the difficulty that OPEC and its allies face in balancing the market.

Futures declined as much 2.2% in New York. The Organization of Petroleum Exporting Countries and its friends face a daunting task next year as supply from competitors grows, the IEA said. Following a meeting in Abu Dhabi, the producers group put pressure on its members to implement their promised output cuts amid growing concerns the oil market will tip back into surplus. Crude was also pushed lower by a stronger dollar after the European Central Bank started a stimulus program.

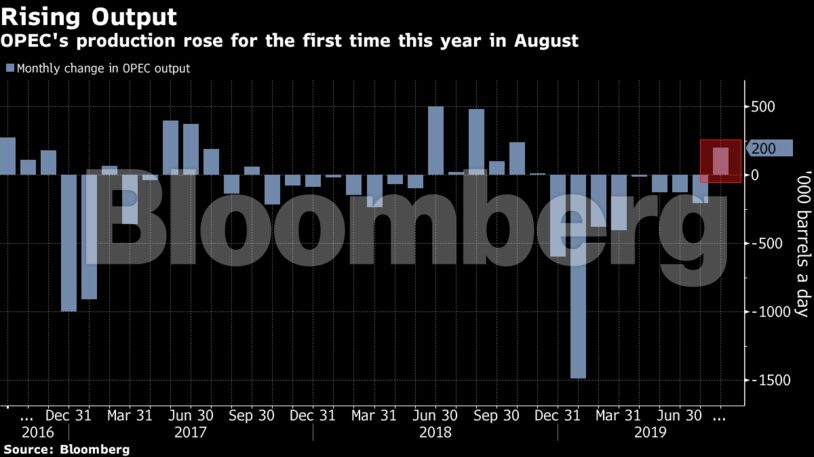

Oil has fallen more than 15% from its April peak as the prolonged U.S.-China trade spat has dented the outlook for global demand. The IEA’s report on Thursday highlighted the scale of the challenge facing producers as supply is expected to surge in countries — including America — that aren’t part of the OPEC+ agreement.

“The market is giving up on OPEC+ being able to support the price,” said Ole Hansen, head of commodities strategy at Saxo Bank A/S. “They can control production but not demand.”

West Texas Intermediate crude for October delivery lost $1.11, or 2% to $54.64 a barrel on the New York Mercantile Exchange as of 8:56 a.m. local time. Brent for November settlement fell $1.38 to $59.43 a barrel on the ICE Futures Europe Exchange, and traded at a $4.85 premium to WTI for the same month.

See also: Oil Demand Downturn Sets Downbeat View at Asia’s Premier Event

Demand for OPEC’s crude in the first half of next year will be 1.4 million barrels a day below its August output as production surges from competitors, the IEA said. The group and its allies didn’t discuss deepening the supply curbs set out in last year’s agreement, although they could revisit the issue in December, Oman’s Oil Minister Mohammed Al Rumhy told reporters after the meeting in Abu Dhabi.

| Other oil-market news: |

|---|

|

Share This: