CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Enda Curran

(Bloomberg)

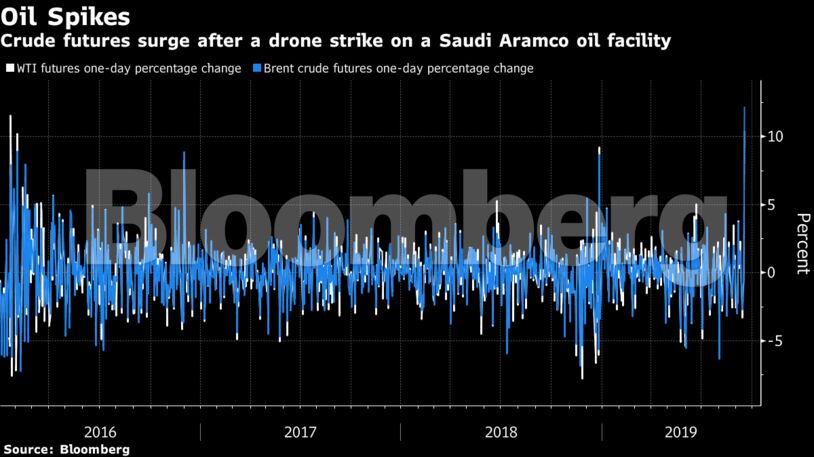

The record oil-price surge after a drone strike on a Saudi Arabian oil facility couldn’t come at a worse time for a world economy already in the grip of a deepening downturn.

While the severity will depend on how long the price spike endures, the development will further erode business and consumer confidence that already are fragile amid the U.S.-China trade dispute and slowing global demand. A manufacturing slump around the world is hammering growth in export powerhouses China and Germany.

“A negative supply shock like this, when global growth is in a synchronized slowdown with many geopolitical hotspots simmering, is just what we don’t need,” said Rob Subbaraman, head of global macro research at Nomura Holdings Inc. in Singapore.

The oil shock comes amid a flurry of warning signs for the global economy. Data Monday out of China included the worst single-month reading for industrial output since 2002. In July, the International Monetary Fund reduced its global growth outlook — already the lowest since the financial crisis — to 3.2% this year and 3.5% next; a rate of 3.3% or lower would be the weakest since 2009.

Variable Impact

The impact from the oil-price spike will vary around the world.

Emerging economies nursing current account and fiscal deficits — like India, South Africa and others — run the risk of large capital outflows and weaker currencies.

Exporting nations will enjoy a boost to corporate and government revenues, while consuming nations will bear the cost at the pump, potentially fanning inflation and hurting demand. As the world’s biggest importer of oil, China is vulnerable to rising crude prices, while many countries in Europe also rely on imported energy.

With inflation not an immediate concern in the global economy, the bigger worry is the effect a price shock will have on global demand that’s already weak.

“Inflation is not really an issue at the moment,” said Louis Kuijs, chief Asia economist at Oxford Economics in Hong Kong. “But the production shortage and price increase will choke purchasing power and thus weigh on spending at a precarious moment for the global economy.”

Dovish Response?

An IMF analysis in 2017 found that a one-year, one-standard-deviation shock to oil supply — in which the oil price jumps more than 10% — would erode world output by about 0.1% for two years.

The news from Saudi Arabia boosts the chance of additional monetary policy support from central banks in anticipation of higher energy costs that are effectively a tax on consumers, David Mann, chief economist for Standard Chartered Plc in Singapore, told Bloomberg Television.

“We would argue this adds to the reasons why we are going to see more dovish surprises from central banks over the next few weeks,” Mann said.

The Federal Reserve is poised to cut interest rates for a second straight meeting this week and its gathering will be followed by the Bank of Japan, which is under pressure from investors to loosen monetary policy further. Central banks of Brazil, South Africa, Norway, Switzerland and the U.K. will also decide policy this week.

U.S. President Donald Trump used the occasion to restate his attacks on the Fed and his demand for a large reduction in borrowing costs. “The United States, because of the Federal Reserve, is paying a MUCH higher Interest Rate than other competing countries,” he tweeted Monday. “And now, on top of it all, the Oil hit. Big Interest Rate Drop, Stimulus!”

In a hint of how emerging economy officials may react, Philippine central bank Governor Benjamin Diokno said the price shock will figure into policy makers’ discussions when they meet next week to decide interest rates. Bank Indonesia has a policy meeting scheduled Thursday, with the majority of economists surveyed before the Saudi attack predicting a 25 basis-point rate cut.

“A significant spike in oil prices is the last thing the world economy needs now,” said Shane Oliver, head of investment strategy and chief economist at AMP Capital Investors Ltd.

Share This: