CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Liam Denning

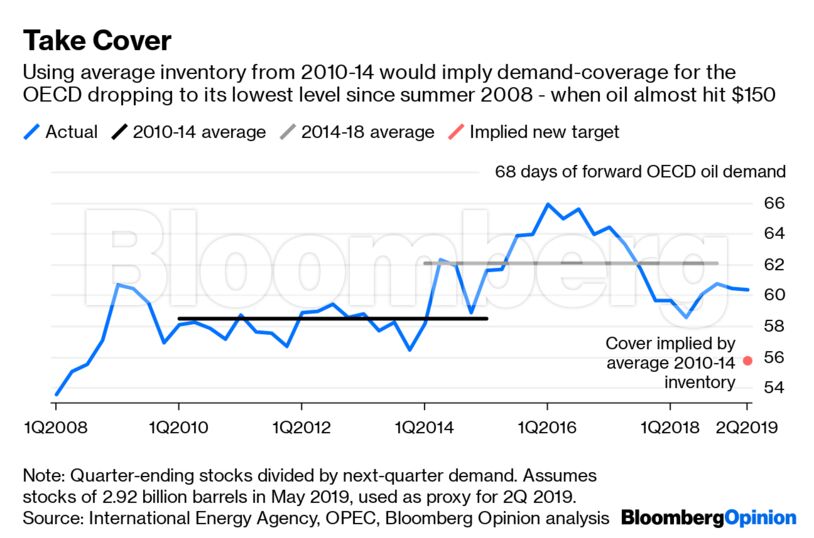

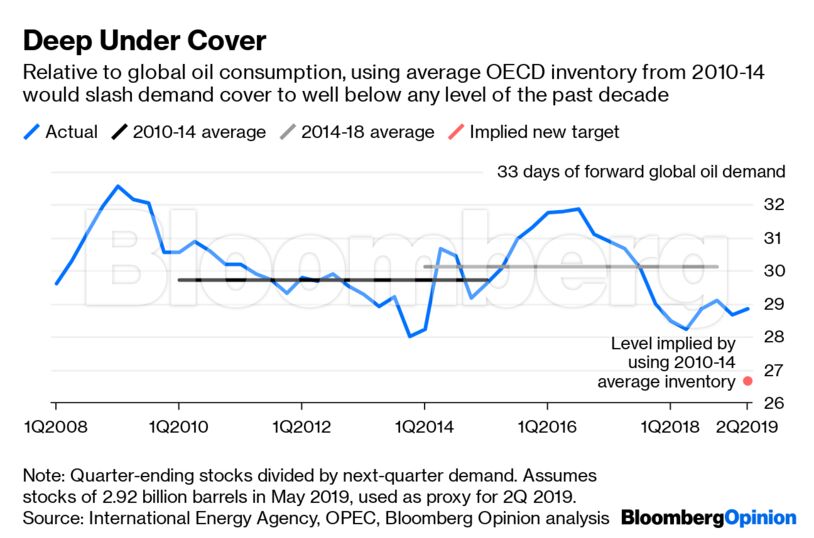

The added wrinkle is that most of the growth in oil demand this decade has been in developing economies. So the chart above likely understates the true impact of cutting OECD inventory back to pre-crash levels. Comparing those stocks to global demand implies an even tighter market if those 220 million-odd barrels drained away:

Suffice to say, targeting a level that would slash roughly the equivalent of a work week from OECD demand cover would be a very aggressive move. On one hand, it’s easy to see why Saudi Arabia would be interested in a harder turn of the dial on its time machine. The government needs higher oil prices to fund itself without continuous resort to deficits. It’s also reportedly reviving plans for an IPO of Saudi Arabian Oil Co., or Saudi Aramco. Even if that’s unlikely to hit the $2 trillion valuationbandied about originally, it would still benefit from a tailwind of higher oil prices. And Saudi Arabia provides the bulk of voluntary supply cuts for OPEC+ anyway, so its views count for a lot.

Like picking a static metric from years ago as a target, however, taking such considerations in isolation from the broader context of the oil market would border on the ridiculous.

Alexander Novak, Russia’s energy minister, sounded less enthusiastic about the idea in remarks on Tuesday, noting changes in demand ought to be considered. Moscow likes higher oil prices, too, but isn’t quite as needy as Riyadh. Moreover, Russia’s oil companies aren’t thrilled about curbing supply – even the relatively small cuts they contribute to OPEC+ – and Al-Falih’s suggestion essentially implies cuts as far as the eye can see.

Taking demand cover down that far would, all else equal, light a fire under prices – and thereby spark a bigger surge in U.S. shale production and likely deliver a knock-out blow to demand growth, which looks shaky already. Saudi Arabia may well be throwing such figures around merely to nudge OPEC+ toward a tighter target short of such a nuclear option. As I wrote here, though, supply cuts themselves carry an inherently bearish undertone. Even deeper cuts wouldn’t change that and, ultimately, would reinforce it.

With assistance from Julian Lee.

Share This: