CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

- Pockets of carbon capture projects are emerging in U.S. and Europe as developers capitalize on surging power demand and public funding initiatives but costs remain too high for the sector to boom.

March 30 – Google’s recent deal to purchase electricity from a planned 400 MW natural gas plant with carbon capture and storage (CCS) in Illinois has shone a spotlight on the potential for CCS in the United States.

The Broadwing project is the first in a long-term collaboration between Google and developer Low Carbon Infrastructure (LCI) to build future CCS facilities in the U.S. and demonstrate commercial-scale deployment, Michael Terrell, Head of Advanced Energy at Google, told Reuters Events in December.

“Our long-term goal is to accelerate the path for CCS technology to become more accessible and affordable globally, helping to increase generating capacity while enabling emission reductions,” Terrell said.

In December, NextEra announced a partnership with ExxonMobil to develop gas-fired plants with carbon capture that will supply power to data centers.

These CCS investments come as power-hungry Big Tech companies are increasingly choosing on-site natural gas generation to source power for their data centers.

Despite the announcements by Google and NextEra, most Big Tech companies have “put CCS on the back seat” for now due to its high costs and longer timelines compared with other power technologies,” Peter Findlay, Director of CCUS Economics at Wood Mackenzie, told Reuters Events.

The cost of adding CCS to U.S. gas plants is estimated at $20 to $30 per megawatt hour (MWh), potentially doubling the cost of power production. Building these projects in the early stages of global CCS deployment would take time and “might slow them down,” Findlay said.

Download our exclusive report on how energy investors are capitalizing on soaring power demand.

Microsoft, for example, is involved with numerous direct carbon capture technology projects worldwide but is yet to commit to U.S. power generation with CCS to decarbonize its soaring power demand.

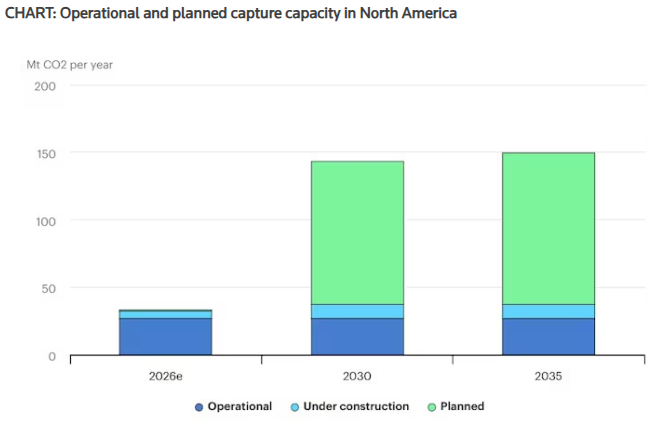

Source: International Energy Agency (IEA), 2026.

U.S. CCS developers benefit from lower gas and energy prices than in Europe as well as large land areas and geological features that offer greater potential to develop underground storage facilities.

But they also face policy uncertainty. President Trump dented U.S. CCS growth hopes by cancelling grants worth $1 billion for as many as 95 carbon capture projects that were allocated by former President Joe Biden, according to a Clean Air Task Force (CATF) report published in November.

At the same time, Trump’s One Big Beautiful Bill preserved tax credits for CCS projects that start construction before 2033 ($85/metric ton) and increased credits for projects that convert carbon into useful products, such as urea and synthetic fuels, from $130/metric ton to $180/metric ton.

The tax credits are not enough to incentivize CCS for steel and cement plants, and as a result “we’re not seeing a lot of projects going forward on their own economics,” warned Findlay.

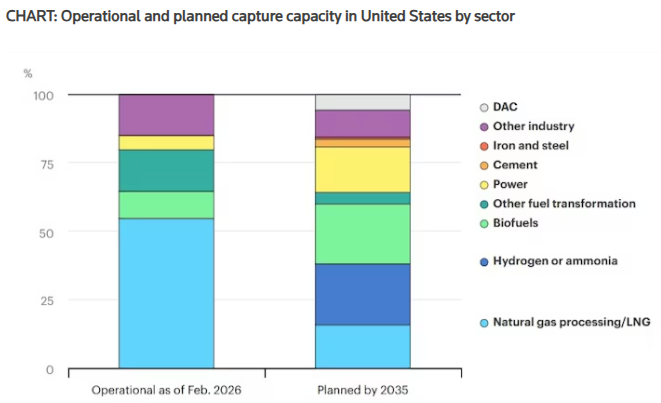

Source: International Energy Agency (IEA), 2026.

The tax credits are a boost however for CCS at ethanol facilities, which produce gaseous waste that is over 90% carbon, whereas power facilities typically emit under 10% of CO2 that is hard to separate from other impurities, including nitrogen. As a result, the costs of CCS for ethanol facilities typically range from $15 to $35 per metric ton of carbon, whereas for natural gas fired facilities they can reach over $100 per metric ton.

Frontier Infrastructure, owned by Tailwater Capital, is providing carbon management services for ethanol producers in the Midwest as well as developing gas-fired power plants. The company operates the Sweetwater Carbon Storage Hub in Wyoming, which has 500 million tons of storage capacity, and is developing a co-located rail terminal to receive captured CO2.

The lower costs of installing CCS in ethanol facilities mean the tax credits alone make the projects economically viable, said Robby Rockey, President and Co-CEO at Frontier Holdings.

Development of CO2 pipelines in the Midwest remains challenging and utilizing the expansive rail network “mitigates community impact and creates an economic solution for ethanol producers to pursue CCS,” Rockey said.

Europe’s transport challenge

The European Union is providing support for CCS growth to achieve its carbon emissions targets but deployment has been stinted by a lack of access to CCS transport and storage facilities.

Join hundreds of senior executives across energy, industry and finance at Reuters Events Global Energy Forum 2026.

The EU Emissions Trading System (EU ETS) incentivizes carbon capture and storage projects by forcing industries such as cement and steel to pay a price for the carbon they emit. Companies pay between 70 and 100 euros/ metric ton ($81-$116/mt) for “carbon allowances” and the EU uses the revenues raised to finance carbon capture projects through its Innovation Fund.

Grants from the fund can cover up to 60% of the capital and operational costs of CCS projects and the fund is expected to collect 40 billion euros in tax revenues by 2030.

Meanwhile, the 2024 Net Zero Industry Act (NZIA) requires EU oil and gas producers to develop a total 50 million metric tons of carbon storage capacity annually by 2030 and there are other EU and national CCS funding mechanisms designed to close cost gaps, speed project development, and expand carbon transport and storage infrastructure across industrial regions.

Heidelberg Materials used Norwegian government funding to install the world’s first industrial-scale carbon capture facility at a cement plant in Brevik, Norway.

The company has a pipeline of eight other CCS projects – six in the EU that have secured funding from the Innovation Fund and one each in the UK and Canada.

Early-stage projects in the EU need “a supportive political framework” that should include the “development of infrastructure for CO₂ transport and storage, where existing challenges must be addressed in close collaboration with all stakeholders,” a Heidelberg spokesperson told Reuters Events.

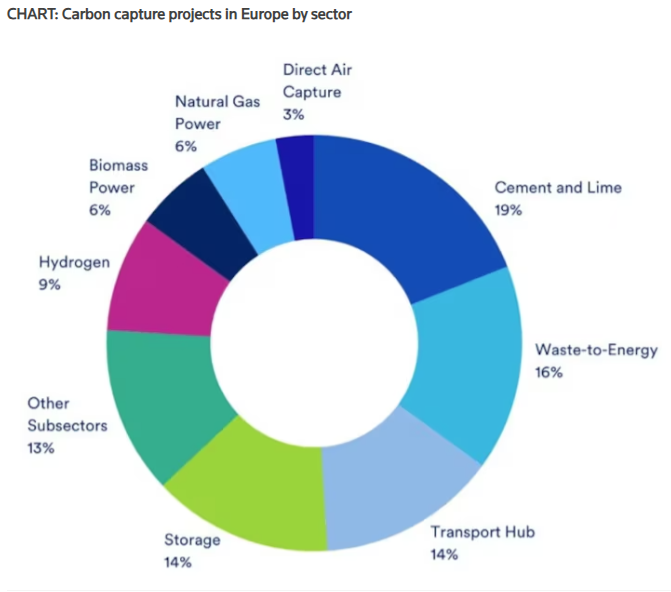

Source: Clean Air Task Force (CATF), 2026

Operational since June 2025, Brevik was made possible thanks to Northern Lights in the North Sea, the world’s first cross-border CO2 transport and storage facility developed by Equinor, Shell, and TotalEnergies with funding from the Norwegian government.

Northern Lights started receiving carbon from Brevik last summer and is slated to start taking shipments from Yara’s Sluiskil Ammonia production plant in the Netherlands and Orsted’s Asnaes and Avedore biomass plants in Denmark later this year.

Northern Lights is a catalyst for wider CCS deployment in Europe, said Jamie Burrows, the Global Segment Lead for CCS at DNV, in large part because its capacity is being expanded from 1.5 million metric tons per annum (Mt/a) to 5 Mt/a by 2028.

Early-stage CCS projects such as Northern Lights relied on public funding because of the high capital costs, technical and regulatory risks, and immature revenue streams involved, Burrows told Reuters Events.

“Over time it is anticipated that the cost of emitting CO2 will rise and the costs of CCS will reduce such that the business case for CCS deployment strengthens,” he said.

Meanwhile, the Port of Rotterdam CCS project (Porthos) will capture carbon from Air Liquide, Air Products, ExxonMobil, and Shell facilities by installing the pipeline infrastructure required to transport CO2 to empty gas fields in the North Sea where it will be permanently stored. Construction of Porthos began in 2024 and operations are slated to start later this year.

These pioneering storage projects combined with EU support mechanisms will eventually help establish other CCS hubs in Southern and Eastern Europe. Transportation and storage infrastructure will lower cost uncertainty and allow the CCS sector to “transition away from its subsidy model to one where we do see more demand for the actual thing they’re producing,” said Toby Lockwood Director, Carbon Management Practice at the Clean Air Task Force (CATF).

Suppliers of low carbon materials need strong demand signals to commit investments. In an initial step, the EU is finalizing legislation to mandate the use of materials produced through CCS and other low carbon sources in public procurements but needs more products available before it can roll out this policy, Lockwood said.

Right now “it’s difficult for governments or companies to procure a material which doesn’t exist yet,” he said.

–Editing by Robin Sayles

Share This: