CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

The industry is staring down prolonged disruptions in the Persian Gulf. Emerging economies are already paying the price.

By Ruth Liao, Stephen Stapczynski and Priscila Azevedo Rocha

Each week the world’s largest liquefied natural gas plant remains shut, the world loses the equivalent of enough energy to power Sydney’s homes for an entire year.

Qatar’s Ras Laffan plant closed earlier this month after an Iranian drone attack, the first interruption to supply in three decades of operation. Now, after further hits — in retaliation for an Israeli strike on the vast South Pars fields on Wednesday — the wider complex has suffered what Qatar describes as extensive damage, potentially significantly delaying any return to normality.

Neither the scale of destruction nor the extent of repair work required for resumption is clear. But every day the operation isn’t running, the energy strain on economies across the world increases. For emerging nations, vital growth markets for LNG, a second gas calamity in four years is already destroying industrial demand — perhaps irreparably.

Three weeks of conflict in the Middle East have upended the entire energy supply chain. With the vital Strait of Hormuz all but closed, gasoline and jet fuel prices are surging, cooking gas shortages are triggering fistfights in India and farmers are fretting about diesel and fertilizer. But with virtually no spare capacity, no strategic reserves and no easy replacements, LNG may be one of the most acute pain points in an expanding crisis.

The longer this continues, the only solution is for the world to use less gas — and that’s a major setback for a fuel promoted by the industry as a reliable and affordable bridge from dirty coal to full reliance on renewable power. Without gas, power plants curtail output, fertilizer and textile factories shut. The ripple effect from a long-term shock could be even more significant than the 2022 energy crisis, when Russia’s invasion of Ukraine forced dramatic changes in global gas flows.

“We are now well on our way to a doomsday gas crisis scenario,” said Saul Kavonic, energy analyst at MST Marquee. “Even once the war ends, the disruption to LNG supply could last for months or even years — depending how long it takes to repair the damage.”

The most immediate impact of the current crisis is that it has almost certainly erased a global gas glut that was widely expected from this year, when the world had been set to see a dramatic boost in production. The U.S. will still be ramping up, but with the Middle East hobbled, the balance quickly turns negative.

An interruption beyond one month “quickly brings a deficit,” according to Morgan Stanley. If that stretches to three months, it will be the biggest LNG outage in the industry’s half-century history.

“South and Southeast Asia are going to be the immediate casualties,” said Toby Copson, a China-based portfolio manager at Davenport Energy, which trades oil and gas. If the disruption does extend for months, he added, “we see indices going parabolic again.”

Already, the shortages are visible in emerging economies across Asia, which buys four-fifths of Qatar’s LNG and takes most of the shipments out of the United Arab Emirates.

Pakistan relies on Qatar for 99 per cent of its LNG imports and the South Asian nation’s officials have now warned there may not be enough gas to meet power requirements from mid-April. Textiles, Pakistan’s biggest export, face a double whammy, as gas is used for power generation on site at factories, and also for heat during processing, according to Aamir Sheikh, an owner of a fabrics business in Punjab.

“Production will decrease, reducing exports. The viability of remaining exports will also be reduced due to increases in cost,” he said. “The bottom line is that industry is very worried.”

The same scenario is playing out across developing Asia, where LNG is typically used for industrial processes, from fertilizer plants to glass factories.

It’s a price shock that will almost certainly force price-sensitive emerging economies to reconsider ambitious LNG expansion plans. A single shipment heading to Asia costs around US$80 million a pop — more than double the going rate before the Iran war started. Vietnam and the Philippines have effectively paused additional purchases until prices ease, while Indian firms have been pushed into some of their costliest purchases in years. Pakistan — already scarred by a 2022 spike that brought severe blackouts — is accelerating efforts to cut back.

In theory, this could be a green boon. In reality, given the nature of LNG consumption in the region, it is more often resulting in higher dependence on coal, the most polluting fossil fuel. Philippine officials are in talks with Indonesia to secure more of the black stuff, while India expects to burn a record amount this year to meet peak summer power demand.

“Instead of looking at how high gas prices can go, we are looking at the price point at which South Asian buyers drop out of the spot market entirely,” said Evan Tan, an LNG analyst at intelligence firm ICIS.

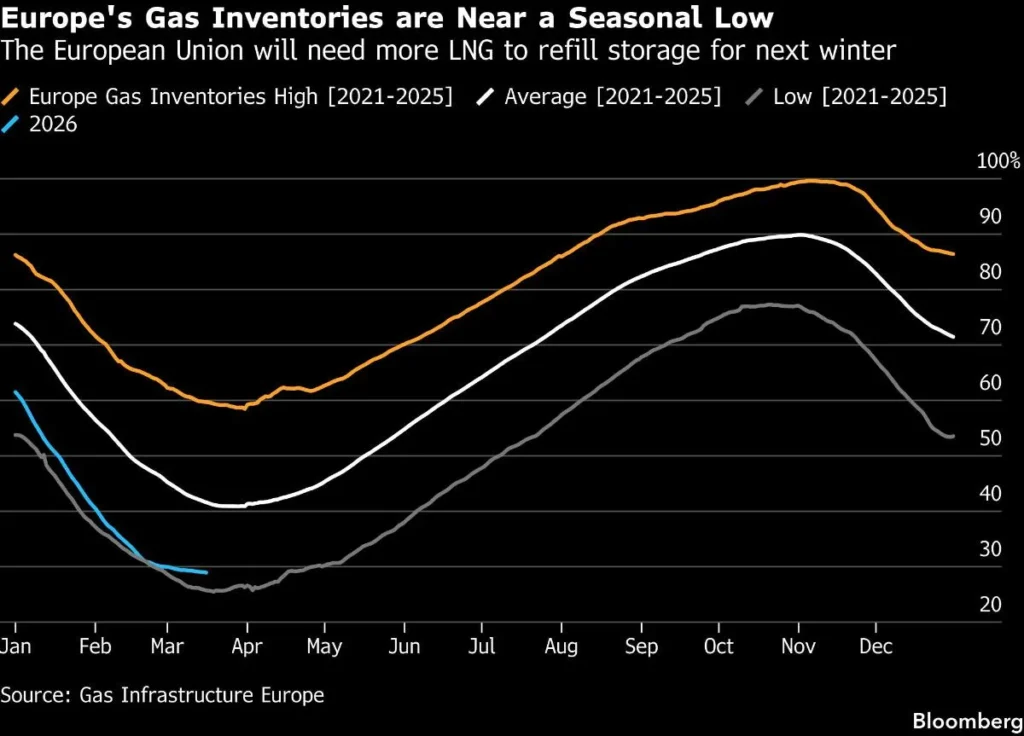

But a prolonged closure in Qatar — assuming repairs to fix damaged equipment, plus a slow restart to exports and shipments through Hormuz — is not just a problem for the poorest nations. A six-month outage means developed countries in Europe and Asia would also face pressure to cut back if gas prices test the highs seen in 2022, according to research group Rystad Energy, especially going into the time of year when they restock for the winter.

Gas buyers did take lessons from the last crisis, which saw widespread industrial demand destruction in economies like Germany. The European Union at least became all too aware of the need not to rely on one source of supply — Russia provided about 40 per cent of its gas needs in 2021, the year before its tanks rolled into Ukraine — and sought to diversify, building LNG import terminals and storage targets. China’s focus on diversification only intensified.

But that was insufficient protection against a shock as historic as the effective closure of Hormuz, which connects Persian Gulf producers to the wider world, and an outage in Qatar, which made its name as the industry’s most reliable supplier.

The heart of the issue is that the LNG, the fastest-growing fossil fuel market, still operates largely on decades-spanning contracts that provide just-in-time deliveries. And the reason is simple enough — the super-chilled gas slowly evaporates, storage is expensive and takes time to build. Everything is hyper specialized, down to the ships and import terminals, and unlike in oil, there is no global cluster of strategic reserves.

When the system works, such costs appear unnecessary. When it doesn’t, it’s already too late.

Yukio Kani, an executive with over three decades in the industry, describes this crisis as akin to 2022, or the 2011 Fukushima disaster, which forced Japan to shut its nuclear plants almost overnight and dramatically increased LNG consumption.

“It has only just started, so we don’t yet know whether it will surpass those events or not,” Kani, the chief executive officer of Jera Co., Japan’s largest LNG importer, said on the sidelines of a conference in Tokyo last weekend. Gas prices have surged, but even after the repeated hits on Ras Laffan had yet to hit the peak seen four years ago.

Those who can afford it are already preparing, though. Taiwan — a chip-manufacturing hub whose energy vulnerabilities have been left particularly exposed, as it depends on LNG imports — is rushing to secure shipments, buying enough for April and half of its May requirements. South Korea is scrambling to replace lost Qatari shipments, and is lifting its operating cap for coal power plants.

The real risk starts with the summer, when inventories are refilled.

“Ultimately we will need more demand rationing because there’s not enough gas,” said Francisco Blanch, head of global commodities and derivatives research at Bank of America. Inventories in Europe “are very low coming out of a cold winter. And you need to rebuild those stocks in the next two, three months and that’s when the pressure is gonna start coming in.”

Curbing gas consumption in Europe usually starts with industries most dependent on the fuel — chemical makers and large industrial users. Since 2022, closures of such plants have surged sixfold and investments in the sector have tumbled by more than 80 per cent, according to a report by consultancy Roland Berger for industry group Cefic.

Granted, even in a crisis of this magnitude, not everyone loses. Upheaval in the Persian Gulf benefits other major producers seen as safer bets, including Australia and especially the U.S., so far largely insulated from price surges. Then the question becomes whether either has the capacity to significantly boost output and serve new customers at short notice.

Asian countries are already knocking, U.S. officials say. Taiwan’s government is seeking to boost U.S. LNG purchases from June, while officials in Bangladesh have been exploring a possible deal to receive additional shipments. Japan’s energy minister asked Australia’s minister to unlock more supplies, a move some industry experts see as wishful thinking — the producer is already maxed out.

Under pressure, more outlandish projects on global drawing boards start to look possible, even the proposed Alaska facility backed by Trump and dismissed as fanciful by many in the industry.

The interest has always been there, according to U.S. Interior Secretary Doug Burgum, because of a shipping distance of just eight days to Tokyo, as opposed to 24 to 28 days from the Middle East across to Japan. “Eight days, but five days — over half the trip — you’re still in U.S. waters.”

“The big swing suppliers were us and Qatar,” said Michael Sabel, CEO of Venture Global Inc., one of the top US LNG developers. “And so we still have availability and then there’s incremental supply slowly coming online.”

The next U.S. project slated to come online in the next few months is Golden Pass in Texas, which is being co-developed by QatarEnergy and Exxon Mobil Corp. The disruption at Ras Laffan may force Qatar to think about expanding further investments overseas to help hedge against future disruptions. “A global gas crisis only increases US export revenue and drives more gas-intensive manufacturing and jobs into the U.S.,” said MST Marquee’s Kavonic.

Another potential winner is Russia, which has been steadily ferrying LNG to China to work around tighter Western restrictions and the loss of Europe as a top gas buyer. China’s latest five-year plan, published earlier this month, calls for advancing work on the China-Russia central-route natural gas pipeline — a likely reference to Power of Siberia 2. Until recently Moscow had promoted the project with far greater enthusiasm than Beijing, which has long been more concerned with diversifying supply.

In the meantime, Europe and Asia also risk competing for scarce supply, raising the prospect of a price war between the Atlantic and Pacific basins. That creates a lucrative opportunity for traders with uncommitted cargoes — and could even incentivize some to walk away from long-term contracts to capture higher spot prices, as seen in 2022.

While Europe has enough supply for the next month, some officials are anxious about a situation that continues for longer and pits them against Asia, according to people with knowledge of the matter. Europe secures much of its supply from the spot market, which makes it susceptible to price shocks or even diversions, if Asia is willing to pay up.

“Once the price spikes set in, the more affluent countries can continue to bid. The less affluent countries get squeezed out,” said Menelaos Ydreos, secretary general of the International Gas Union. “We cannot make up what’s lost coming out of the Strait.”

With assistance from Dan Murtaugh, Jennifer A Dlouhy, Ewa Krukowska, Yusuke Maekawa, Sing Yee Ong, Elena Mazneva, Tooba Khan and Shoko Oda.

Bloomberg.com

Share This: