CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Liam Denning

In demand. Photographer: Callaghan O’Hare/Bloomberg

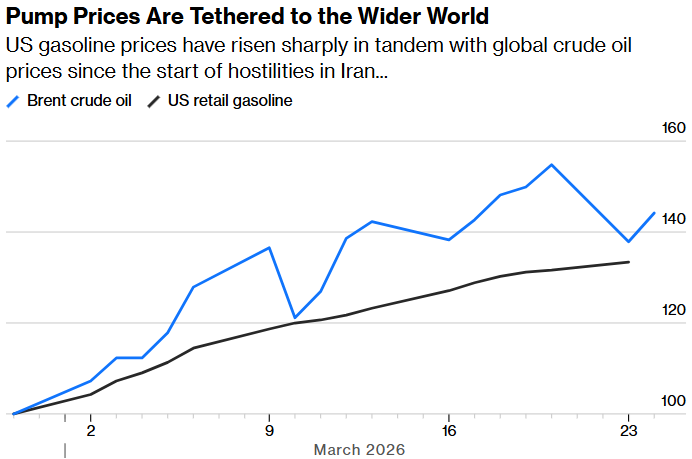

The conflict in Iran represents both an expression of US “energy dominance” and a profound test of it. Resurgent domestic oil and gas production promised insulation against the fallout from a new war in the Middle East. The same war is casting doubt on that promise.

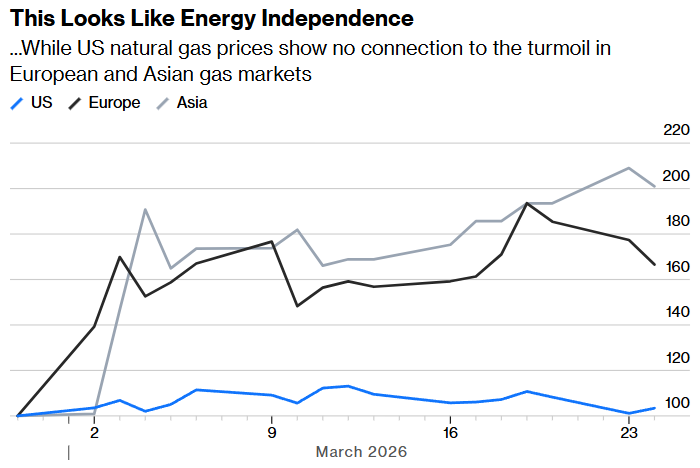

The issue of American energy independence — the older, slightly less ambitious cousin of dominance — has tended to center on oil due to the legacy of the 1970s’ supply shocks. Yet, despite the US now being firmly established as a net exporter of oil, gasoline looks set to cross the $4-per-gallon Rubicon just a few weeks into this war. Natural gas, not oil, is where the US really stands aloof from the world’s troubles.

Note: Prices indexed to 100 on February 27, 2026.

Source: Bloomberg

Note: Reference front-month futures prices for Henry Hub, TTF and JKM benchmarks, respectively, indexed to 100 on February 27, 2026.

Source: Bloomberg

Oil is defined by the global tanker trade whereas markets for natural gas, which is much harder to transport and store, remain largely regional. Linkages between those have strengthened with the rise of liquefied natural gas on ships, but such cargoes still only account for about 14% of global consumption. Moreover, US LNG terminals were running flat out at the end of 2025 as it was. That left no spare capacity to react to the spike in European and Asian prices and thereby transmit the impact of that back to domestic prices — for now, anyway.

Like war itself, America’s gas “dominance” could have its own unintended consequences.

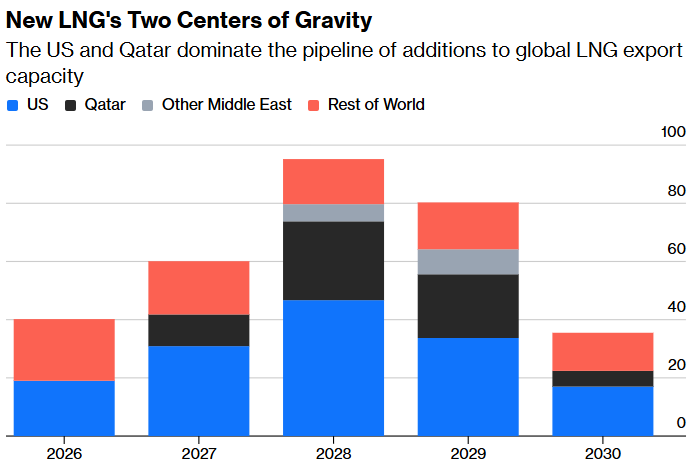

Iran’s effective closure of the Strait of Hormuz and damage inflicted to Qatar’s flagship Ras Laffan LNG export complex have affected roughly a fifth of the world’s LNG flows. Until the outbreak of war, the outlook for LNG pricing was relatively subdued. Export capacity is booming, projected to expand by about 311 billion cubic meters of gas equivalent by 2030, equal to more than half of current global LNG demand. Of that new capacity, almost half relates to US terminals, with another quarter coming from the Middle East, primarily Qatar. The outlook was for a glut in the closing years of this decade.

Note: Data are billion cubic meters of gas equivalent per year.

Source: International Energy Agency

The war throws those projections into doubt. Even if the conflict were to end relatively soon, the damage done to Qatari infrastructure and, more importantly, to the notion that Middle Eastern LNG supplies are safe enough to sign 20-year supply contracts, will linger. When an unthinkable such as a Hormuz closure becomes reality, prior conceptions evaporate. A grim irony of this war is that the US may not merely be insulated from its immediate impacts on natural gas prices, but it may also be able to capitalize on it if competing capacity in the Middle East gets delayed or canceled in the new environment.

This is where dominance could, strangely enough, portend higher domestic prices for natural gas down the road.

Over the past decade, LNG exports have been something of an escape valve for excess gas production from shale, given relatively slow growth in domestic demand (see this). But now the US faces a sustained period of expanding LNG export capacity even as demand for electricity to power datacenters for artificial intelligence also ramps up, with much of it centered on gas-fired generation. This draw on US gas by Big Tech and a wider world seeking to replace Middle Eastern LNG — plus, in Europe, Russian gas, due to be banned entirely by the end of next year — would tighten the domestic market, all else equal.

As it stands, the Department of Energy’s long-term projections have gas demand from power plants actually declining slightly by 2030, a forecast that is surely due for an update when new figures arrive next month. Meanwhile, LNG exports are expected to rise by the equivalent of 80 billion cubic meters per year by 2030. The latter, however, implies average utilization for all that new US export capacity of only about 50% or so, which no operator would want.

Even under these relatively tame conditions, the DoE expected US natural gas prices to rise in real terms. A combination of AI ambitions and higher demand for US LNG, tying the home market more closely to global disruptions, would surely portend a bigger increase.

Notably, bearish analysts at Goldman Sachs Group Inc., who have been forecasting cancellations of US LNG projects amid an expected glut, just raised their domestic gas price forecasts for 2028 and 2029 by 30%-40%.

If the lesson here, as with gasoline, is that global energy connections can short-circuit dominance via pricing, it would be remiss to overlook another potential unintended consequence. This war is changing perceptions about the security of Middle Eastern fuel exports and the US may benefit from that for a while. But large importers such as China, India and the European Union may similarly balk at increased reliance on a mercurial, and prickly, US in the long term.

As I wrote here, energy’s new ‘ESG’ of economics, security and geopolitics will push countries to at least limit their exposure to US LNG, and possibly diversify away from natural gas in general where alternatives including renewables, nuclear power and even coal are feasible. Such was the hard lesson learned by OPEC members after their brief imperium of the 1970s. It is quite possible that US natural gas dominance portends higher prices at home in the next few years, followed by a demand backlash against such dominance itself.

This column reflects the personal views of the author and does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Share This: