CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Nora Buli

- Europe’s gas storage at 5-year low

- Refilling will require extra 180 LNG cargoes y/y

- Iran conflict cuts supply, lift prices

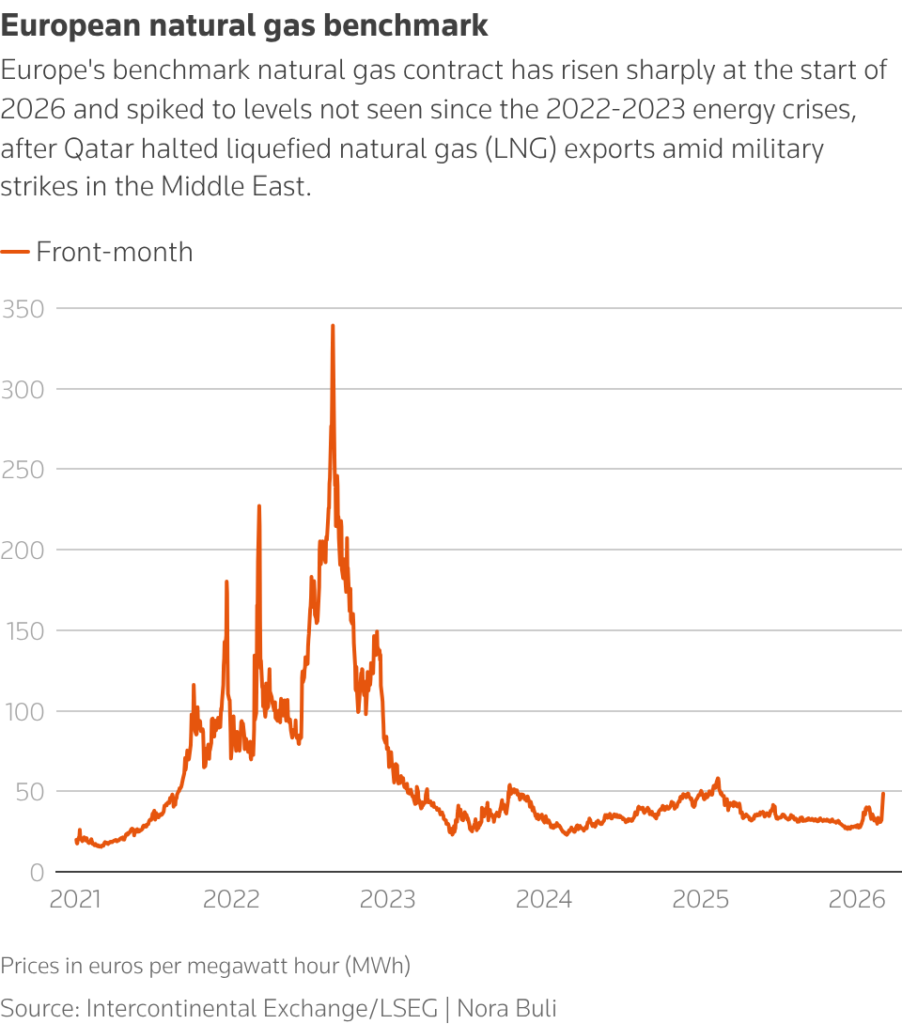

- European benchmark gas at highest since early 2023

OSLO, March 5 (Reuters) – Europe’s already huge task of refilling gas storage for next winter has suddenly become far riskier and far more expensive, as fallout from the U.S.-Israel war on Iran disrupts LNG production and shipments, tightening supply and sending prices soaring.

Gas storage allows Europe to meet winter heating and power demand, underpinning the region’s energy security. This year, stocks are set to end the heating season far below normal levels, forcing Europe to buy more gas during the summer when it refills caverns and tanks across the continent.

Europe has grown increasingly reliant on liquefied natural gas supplies to fill storage since it halted most imports of Russian pipeline gas following the invasion of Ukraine in 2022.

Prior to that, LNG made up about 19% of Europe’s gas supply. The share is expected to rise to 45%, or 174 billion cubic metres, this year, equivalent to around 1,800 LNG tankers, according to S&P Global Energy.

Buyers in Europe need to find the equivalent of around 700 cargoes of LNG, or 67 bcm, just to fill storage this summer, according to analysts at Kpler, about 180 cargoes, or 17 bcm, more than last year.

Some of that will be delivered via pipeline from Norway, Algeria and to a much smaller degree from Russia, but most of it will be LNG cargoes.

Prices of both pipeline gas and LNG have jumped since the start of the Iran conflict.

Benchmark gas prices in Europe briefly hit their highest since early 2023 and are up nearly 50% this week after Qatar shut its gas fields, which account for a fifth of global LNG supply.

The global benchmark LNG contract, the Japan-Korea Marker, was also up by as much as 68% as buyers scrambled to replace lost Qatari volumes.

Europe’s bill for the extra 180 cargoes had increased to about $10.1 billion on Wednesday from $6.7 billion last Friday, Reuters calculated. For the full 67 bcm summer refill, the price has risen by some $13.6 billion to $40 billion.

A line chart tracking the price of Europe’s benchmark natural gas contract since 2021, showing prices have risen to a one-year high in 2026, but remain records seen in 2022.

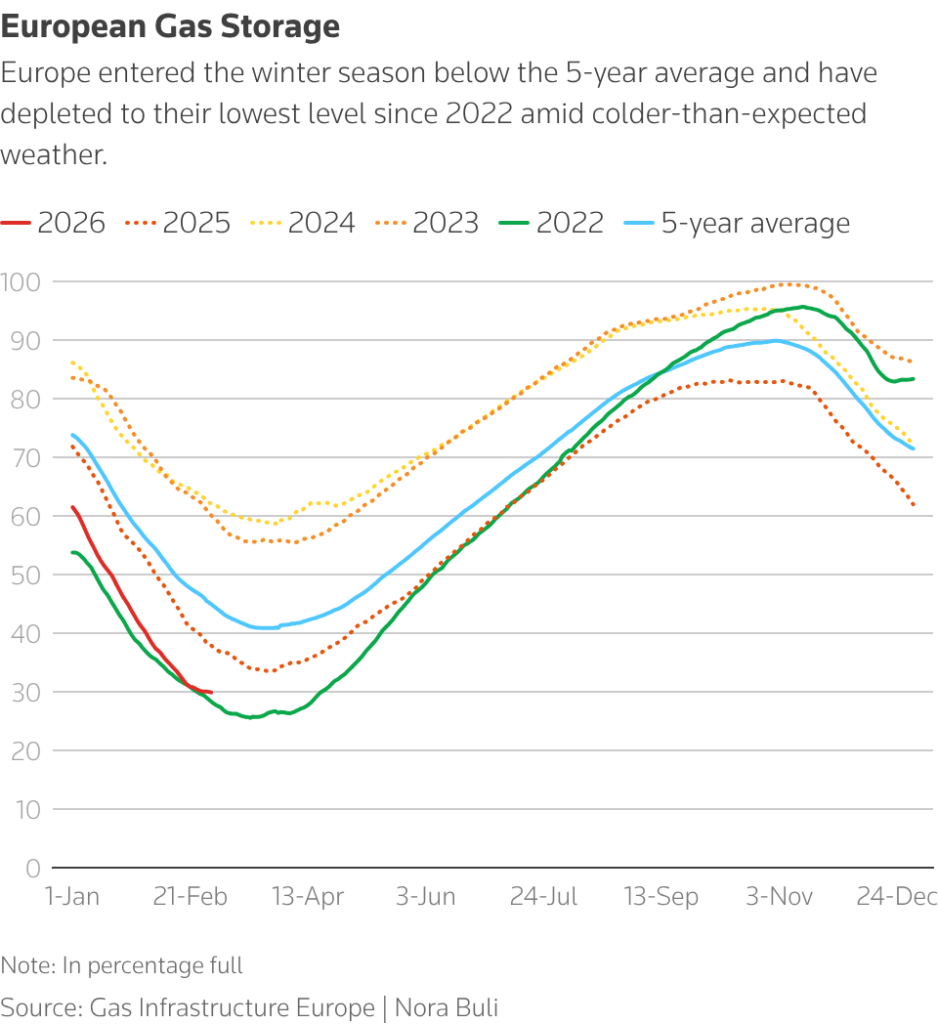

European gas storage will be around 22-27% full at the end of March, according to four analysts, compared with a 5-year average of around 41%. Should less LNG arrive in the next four weeks because of disruption to supplies from the Middle East, then stores could be even emptier.

Line chart of European gas storage levels (% full) by date, comparing 2022–2026 with the five-year average. Storage enters winter below average and falls to the lowest level since 2022, reflecting colder-than-expected weather.

If the shipping paralysis in the Strait of Hormuz lasts for one month, European inventories could fall to a historic low by the end of winter and result in lower end-October filling levels, Energy Aspects analyst Erisa Pasko said.

Some 120 bcm per year, or roughly 20% of global LNG supply passes through the waterway, with four-fifths of deliveries heading to Asia, according to analysts.

Also based on one month of disruption, SEB Research commodities analyst Ole Hvalbye said roughly 7 million tons of LNG, about 9.7 bcm, would be removed from the global market and Europe could effectively lose around 5.5 million tons, or 7.6 bcm, due to competition from Asia for available cargoes.

That would push European gas prices firmly above 60 euros per megawatt hour, compared to around 50 currently and 32 at the end of last week. A prolonged shutdown at Qatar’s Ras Laffan LNG complex would risk a squeeze similar to the 2022 energy crisis, Hvalbye said, warning that

prices of 100 euros/MWh or more could not be ruled out, with demand destruction acting as the main balancing mechanism.

Norway, Europe’s biggest gas supplier, is already pumping at maximum capacity, and while the gas injected into storage this summer will be a mix of pipeline and LNG, the additional demand will need to be met from LNG.

Higher prices will limit incentives to store gas with expectations that prices will eventually fall as the conflict subsides and more LNG supply comes online, Energy Aspects’ Pasko said.

Europe’s dependence on LNG

The United States is the top supplier of LNG to Europe and ranks as the region’s second‑largest gas supplier overall.

While Washington has pressed the European Union to buy more of its LNG as new projects come on line and increase available supply, there is little it can do to lift output quickly enough to compensate for lost Qatari volumes.

European Commission data shows Qatar accounted for 3.5% of EU gas supply in 2025, while the U.S. share stood at 25.4%.

Global LNG supply is forecast to grow by more than 7%, or 42 bcm, in 2026, the International Energy Agency said in January, with the biggest additions coming from the United States.

Reporting by Nora Buli; editing by Nina Chestney, Simon Webb and Kirsten Donovan

Share This:

COMMENTARY: Charting the Widening Impact of the Iran Crisis on Energy Markets