CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

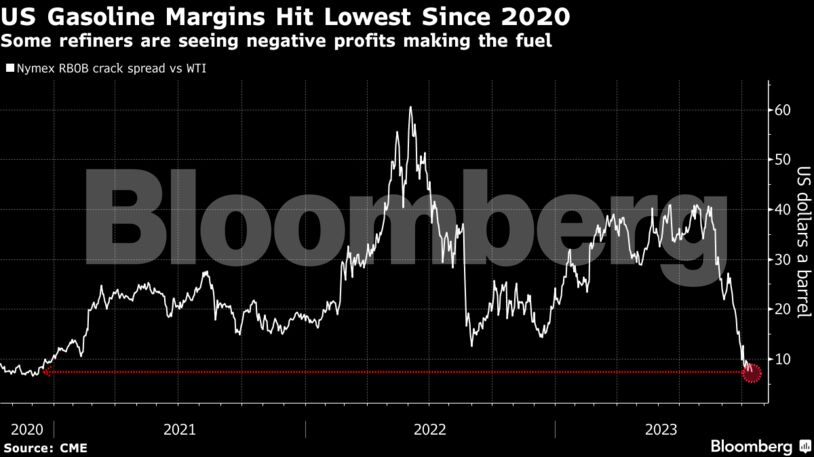

Gasoline futures are plunging even as the oil from which the fuel is made remains strong due to geopolitical conflicts and tight supplies. As a result, margins for making America’s most popular road fuel have sunk below $10 a barrel using the futures crack spread as an estimate.

Individual refineries’ margins vary depending on configuration and the types of crude they process, making it difficult to generalize. But gasoline margins dipped into negative territory for some refiners in early October and late September, according to Robert Auers, an analyst at RBN Energy. That was when the environmental compliance cost was above $5 a barrel, and its still hovering near that level.

Demand is seasonally weak, and fund managers pulling out of net-long positions in the Nymex futures contract also contributed to the gasoline selloff that’s weighing on refiners’ bottom lines, Auers said. In Asia, gasoline weakness is already tempting a Taiwanese refiner to curb oil processing.

Negative US margins are the latest sign of gasoline weakness that dragged oil and the whole energy complex down before the Israel-Hamas conflict jolted prices back up. Soft gasoline is also prone to spark worries about a boarder slowdown in economies trying to curb inflation without triggering a recession.

Such worries found corroboration in the International Energy Agency’s latest report, which pointed to “signs of demand destruction in the United States, where gasoline deliveries plunged to two-decade lows.” The US Energy Information administration also revised down its estimate for fourth-quarter consumption to show a decline from the same period last year, switching from a previous forecast of growth.

For others, including Wood Mackenzie’s principle analyst for refining and oil markets Austin Lin, strong prices may have played a role in holding back some drivers, but they weren’t high enough for long enough to cause significant change in consumer behavior. Pump prices are falling quickly in the US, dropping more than 21 cents a gallon in the two weeks leading up to Sunday, according to data from the American Automobile Association.

Refiners have a few tools to deal with soft gasoline prices: they can minimize output by diverting more feedstock streams to distillates production, and they can choose heavier crudes, an option that’s become increasingly unappealing as Saudi Arabia and its OPEC allies cut supply. Many US refiners are in the middle of a heavy maintenance season and were planning on not turning a profit with units offline. That can also lead to cutting losses when margins are low.

Recent declines in gasoline margins might seem extraordinary — they fell from more than $40 a barrel to less than $10 in just under two months — but they are a return to pre-Covid norms, Lin said. Moreover, refiners are still making historically high profits from diesel, at more than $45 a barrel. That’s enough to carry refiners through. In the meantime, gasoline stockpiles will build through the winter season, a sign that the system is rebalancing, according to Lin.

“The market still needs to grow gasoline,” Lin said.

Gasoline futures are plunging even as the oil from which the fuel is made remains strong due to geopolitical conflicts and tight supplies. As a result, margins for making America’s most popular road fuel have sunk below $10 a barrel using the futures crack spread as an estimate.

Individual refineries’ margins vary depending on configuration and the types of crude they process, making it difficult to generalize. But gasoline margins dipped into negative territory for some refiners in early October and late September, according to Robert Auers, an analyst at RBN Energy. That was when the environmental compliance cost was above $5 a barrel, and its still hovering near that level.

Demand is seasonally weak, and fund managers pulling out of net-long positions in the Nymex futures contract also contributed to the gasoline selloff that’s weighing on refiners’ bottom lines, Auers said. In Asia, gasoline weakness is already tempting a Taiwanese refiner to curb oil processing.

Negative US margins are the latest sign of gasoline weakness that dragged oil and the whole energy complex down before the Israel-Hamas conflict jolted prices back up. Soft gasoline is also prone to spark worries about a boarder slowdown in economies trying to curb inflation without triggering a recession.

Such worries found corroboration in the International Energy Agency’s latest report, which pointed to “signs of demand destruction in the United States, where gasoline deliveries plunged to two-decade lows.” The US Energy Information administration also revised down its estimate for fourth-quarter consumption to show a decline from the same period last year, switching from a previous forecast of growth.

For others, including Wood Mackenzie’s principle analyst for refining and oil markets Austin Lin, strong prices may have played a role in holding back some drivers, but they weren’t high enough for long enough to cause significant change in consumer behavior. Pump prices are falling quickly in the US, dropping more than 21 cents a gallon in the two weeks leading up to Sunday, according to data from the American Automobile Association.

Refiners have a few tools to deal with soft gasoline prices: they can minimize output by diverting more feedstock streams to distillates production, and they can choose heavier crudes, an option that’s become increasingly unappealing as Saudi Arabia and its OPEC allies cut supply. Many US refiners are in the middle of a heavy maintenance season and were planning on not turning a profit with units offline. That can also lead to cutting losses when margins are low.

Recent declines in gasoline margins might seem extraordinary — they fell from more than $40 a barrel to less than $10 in just under two months — but they are a return to pre-Covid norms, Lin said. Moreover, refiners are still making historically high profits from diesel, at more than $45 a barrel. That’s enough to carry refiners through. In the meantime, gasoline stockpiles will build through the winter season, a sign that the system is rebalancing, according to Lin.

“The market still needs to grow gasoline,” Lin said.

Share This:

COMMENTARY: 2025 Review of Global Energy Consumption – William Lacey