CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

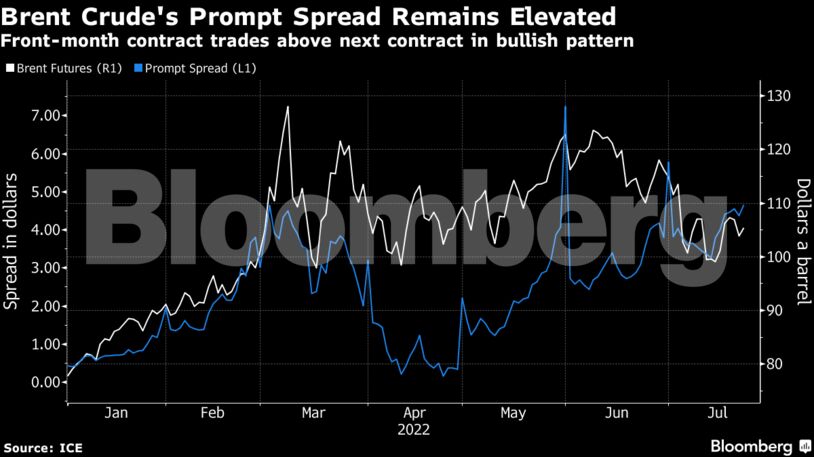

Global benchmark Brent fell as much as 0.6%, to trade near $103 a barrel, almost $2 below its high for the day. Germany’s economy is shrinking for the first time this year as inflation squeezes business and the war in Ukraine hits confidence. The dollar also climbed after the figures making commodities priced in the currency less attractive.

Traders are monitoring the impact of disruption along the Keystone pipeline. TC Energy has reduced operating rates on a segment running from Canada’s oil sands to the hub at Cushing, Oklahoma, by about 15% following a power-supply glitch. Cushing is the delivery point for WTI futures.

While crude remains more than a quarter higher this year, the bulk of the gains triggered by Russia’s invasion of Ukraine have been reversed. Central banks including the Federal Reserve have been raising interest rates to quell soaring inflation, triggering concerns of a slowdown that’ll sap demand for commodities including energy. That’s hurt investor interest in crude oil, and traders are also continuing to monitor China’s continued response to virus outbreaks.

“Recessionary fears and Covid resurgence continue to keep a tight lid on oil prices,” Keshav Lohiya, an analyst at consultant Oilytics said.

| Prices: |

|---|

|

To ramp up the pressure against Russia, the US is aiming to get an agreement on a price cap for the country’s crude. The market hasn’t yet priced in the impact of European Union sanctions aimed at Russian supplies, which adds impetus to the price-cap plan, a US Treasury Department official said.

In a phone call on Thursday, Saudi Crown Prince Mohammed bin Salman and Russian President Vladimir Putin discussed continued cooperation within OPEC+, the broad group that comprises the Organization of Petroleum Exporting Countries and its allies. “It was emphasized that a further coordination within OPEC+ is important,” according to a statement from the Kremlin.

Share This: