(Bloomberg) Oil dropped as risky assets began the week on the back foot and the dollar gained ahead of a Federal Reserve meeting that’s expected to see stimulus scaled back.Futures in New York fell to trade below $71 a barrel amid a broader decline in stock markets. The dollar rose for a third day, making commodities priced in the currency less attractive to investors. Policy makers are poised to start laying the groundwork for reducing monthly asset purchases when the Fed meets for two days from Tuesday, while markets are also weighing the risk of spillover from China Evergrande Group’s woes.“Oil prices are down as the new week of trading gets underway,” said Carsten Fritsch, an analyst at Commerzbank AG. Prices are facing a “headwind today from the firm U.S. dollar in particular, which is showing signs of strength ahead of the Fed’s meeting.”

Alongside the bearish start to the week, traders are continuing to monitor the energy crunch in Europe amid talk of switching from gas to oil. There are expectations diesel demand will expand in Asia during winter, while the use of oil to generate power in the U.S. may jump. Prices for fuels used in heating like liquefied petroleum gas have surged to multi-year highs.

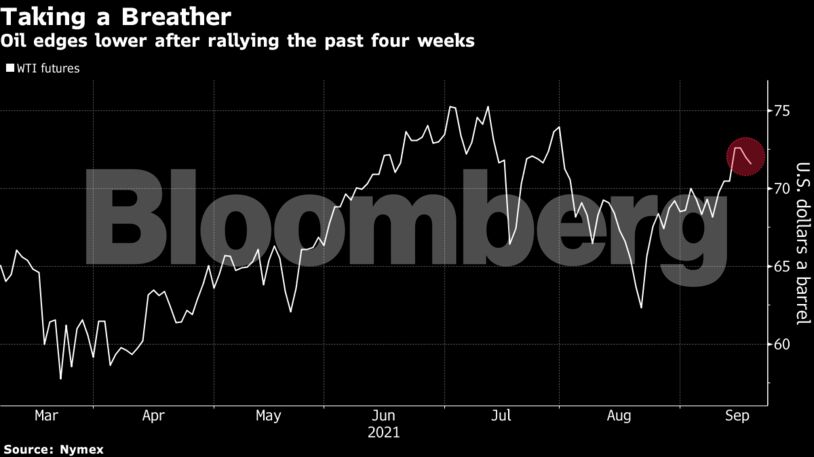

Prices

West Texas Intermediate for October delivery dropped 1.6% to $70.80 a barrel at 9:36 a.m. London time

Brent for November settlement slid 1.4% to $74.32

The prompt timespread for Brent was 78 cents a barrel in backwardation — a bullish structure where near-dated contracts are more expensive than those further out. That followed a surge ahead of Friday’s settle.

Get the Latest US Focused Energy News Delivered to You! It's FREE: Quick Sign-Up Here

Iraq expects oil prices to be around $70 a barrel in the first quarter of next year, with the market kept in balance by supply increases from the OPEC+ cartel and demand continuing to recover from the pandemic.

Other market news:

China’s shipments of gasoline and diesel slumped to the lowest since 2015 last month as Beijing’s reluctance to permit overseas sales meant that local refiners ran short of export quotas.

The long-serving head of Libya’s state-run oil company will remain in his post, Prime Minister Abdul Hamid Dbeibah said in a decree, looking to end a feud between two key oil officials.

Nigeria’s President Muhammadu Buhari has ordered that the process to incorporate the state oil firm as a private company should begin immediately.

CDN NEWS |

CDN NEWS |  US NEWS

US NEWS