CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Kevin Crowley

“Actions of leading operators demonstrate the financial and technical viability of ending routine flaring,” the fund managers said in the letter, which was seen by Bloomberg. “It is clear, however, that voluntary actions alone have been insufficient to eliminate routine flaring industry-wide.”

Investors and environmentalists are increasingly drawing attention to flaring because of its wastefulness and contribution to climate change. Flaring is utilized around the world as a way to deal with gas that producers can’t — or don’t want to — transport or store. Much of what’s burned, especially in the shale fields of Texas, is so-called associated gas coming from oil wells.

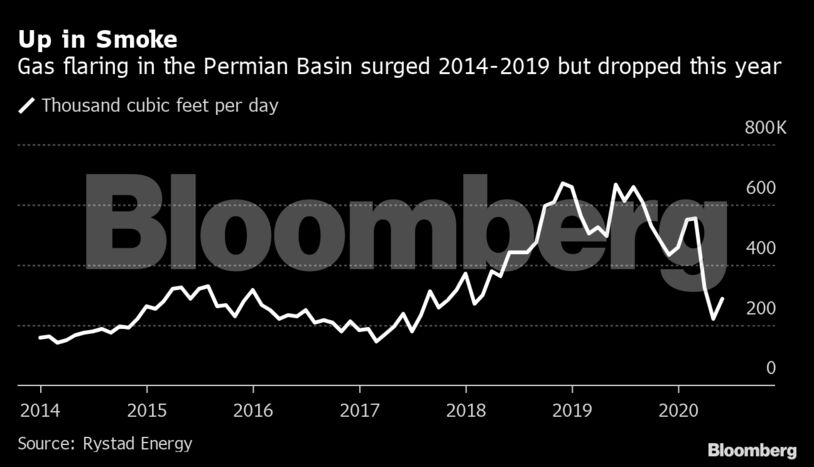

The sheer abundance of gas in the Permian Basin of West Texas and New Mexico means local prices for the fossil fuel are often so low that it’s cheaper for shale operators to burn it rather than pay for pipeline connections and storage. Last year the Permian flared enough gas to supply 5 million U.S. homes, according to Oslo-based Rystad Energy.

The Texas Railroad Commission has come under attack for allowing companies to effectively flare at will over the past decade as shale production boomed and helped make the U.S. the world’s top oil producer. The commission allows companies to flare during the start-up of wells and during emergencies. It also issues waivers that can be utilized right through the early and most productive phase of a shale well’s operation.

After more than a year of public pressure, the commission recently proposed requiring operators to provide information on why they need to flare, but it set no targets and resisted calls for an outright ban. Lower oil production due to the Covid-19 pandemic has meant flaring rates have dropped significantly this year, the commission said in a statement last month.

“Strong and effective regulatory action — beyond initial steps to improve data gathering and transparency — is essential to build stakeholder confidence and solve this challenge across industry,” the investors said in the letter, which is part of the commission’s public consultation.

A spokesman for the Railroad Commission didn’t return a request for comment.

LGIM, the U.K.’s biggest asset manager, supports the role of gas in the transition to cleaner energy sources but the industry “must get hold of its emissions challenges,” said John Hoeppner, head of the firm’s U.S. stewardship and sustainable investment unit.

The Railroad Commission had a “hands-off policy” on flaring for too long, he said. The letter aims to establish a common goal that companies, regulators and investors can rally around and help solve the problem, Hoeppner said. In May, LGIM said it would oppose the re-election of Darren Woods as Exxon Mobil Corp. chairman over what it called a lack of ambition on tackling climate change.

LGIM has about $1.6 trillion of assets under management. AllianceBernstein oversees roughly $600 billion and CalSTRS manages more than $200 billion.

Share This: