CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Ann Koh and Grant Smith

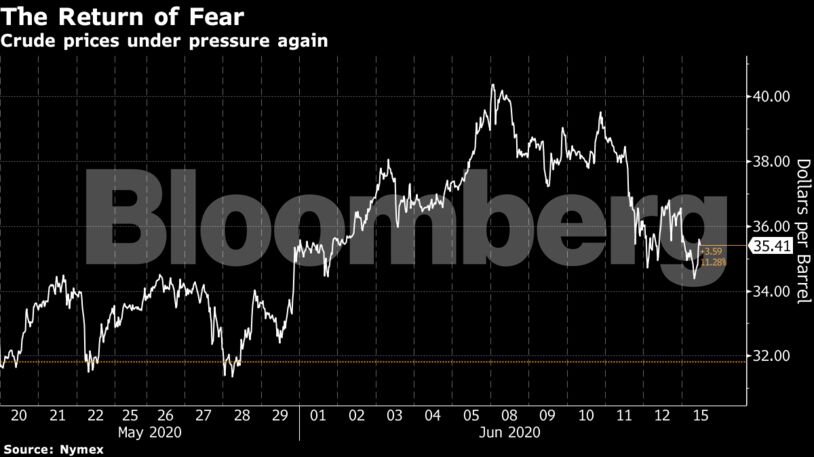

Crude’s six-week rally fizzled last week amid concerns the worst of the virus isn’t yet over and as the Federal Reserve warned the pandemic could inflict lasting damage on the American economy. BP Plc’s announcement on Monday that it will write down the value of its business by the most in a decade reinforced the picture of an industry in turmoil.

West Texas Intermediate crude for July settlement fell 2.2% to $35.46 a barrel on the New York Mercantile Exchange as of 10:44 a.m. in London. It has lost 11% since closing at a three-month high on June 10. Brent for August delivery declined 54 cents to $38.19 a barrel on the ICE Futures Europe exchange after dropping by 8.4% last week.

Still, there are signs that the physical oil market is tightening.

OPEC and its allies have agreed to maintain production cutbacks amounting to about 10% of global supply into next month, and will hold committee meetings on Wednesday and Thursday to assess their impact. Iraq, which has typically lagged in implementing its agreed cuts, instructed BP to reduce output by 10% at the country’s biggest oilfield.

Active drilling rigs across the U.S. fell for a 13th week to the lowest in more than a decade, data from Baker Hughes showed on Friday. On the demand side, Chinese official figures showed refinery runs in Asia’s largest economy rose last month on a year-on-year basis.

Chinese refineries ran 13.69 million barrels a day in May, according to Bloomberg calculations based on figures from the nation’s statistics bureau. That was 7.5% higher than in April and 8.2% more than a year earlier.

| Other oil-market news |

|---|

|

Share This: