CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Golnar Motevalli, Natalia Kniazhevich and Fred Pals

Unless Moscow cuts output, “there will be no deal,” his Iranian counterpart Bijan Namdar Zanganeh said on Thursday.

“Unlike his predecessor Khalid al-Falih, Saudi Energy Minister Prince Abdulaziz is more willing to walk away if Russia does not contribute,” said Amrita Sen, chief oil analyst at consultant Energy Aspects Ltd.

The standoff is the biggest crisis since Saudi Arabia, Russia and more than 20 other nations created the OPEC+ alliance in 2016. The group, controlling more than half of the world’s oil production, has underpinned prices and reshaped the geopolitics of the Middle East, but is now under significant strain. The risk for the Saudis is that if their gamble to corner Russia into a production cut backfires, they have more to lose as they need higher oil prices to fund their budget than Russia does.

Despite OPEC Secretary-General Mohammad Barkindo’s efforts to strike a conciliatory tone by praising Russia as a dependable ally, the oil market braced for more drama. Talks in the Austrian capital on Friday were serious and difficult, with Novak still resisting OPEC’s proposal for deeper curbs, said a delegate.

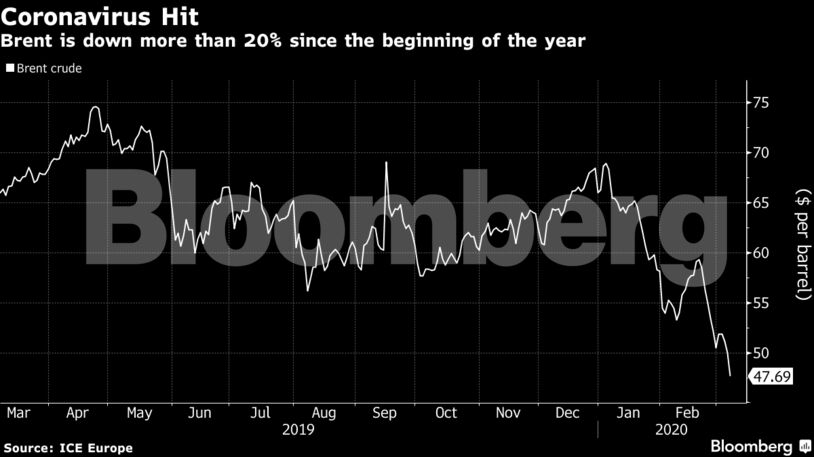

Crude fell as much as 5.9% in London to $47.02, the lowest since July 2017.

“Panic is worsening, demand forecasts are falling, this is a no-kidding emergency and they’ve got to get Russia to ‘Yes’,” Bob McNally, president of consultant Rapidan Energy Group, said in a Bloomberg Television interview. “If they commit an epic policy failure by not cutting production, I think we can easily see a re-visitation of old lows, in and around $26.”

“None of them can afford a price collapse,” said Roger Diwan, a veteran OPEC watcher at consultant IHS Markit Ltd. “This is a battle of egos against reality.”

The current version of the OPEC proposal calls for the cartel to cut 1 million barrels a day of its production, contingent on non-OPEC nations led by Russia reducing their output by 500,000 barrels a day. Ministers initially proposed the curbs for just three months, from April to June, but hours later, in a rare move even by the chaotic standards of OPEC meetings, the group reworked its plan and suggested the cuts stay in place until the end of the year.

Only in July, Russia and Saudi Arabia touted their alliance as a marriage to “eternity”. Fast forward less than a year, and the view among traders is that the couple may be on the verge of divorce. Still, it’s not the first fight between Moscow and Riyadh, and both sides have been able to find a satisfactory solution in the past.

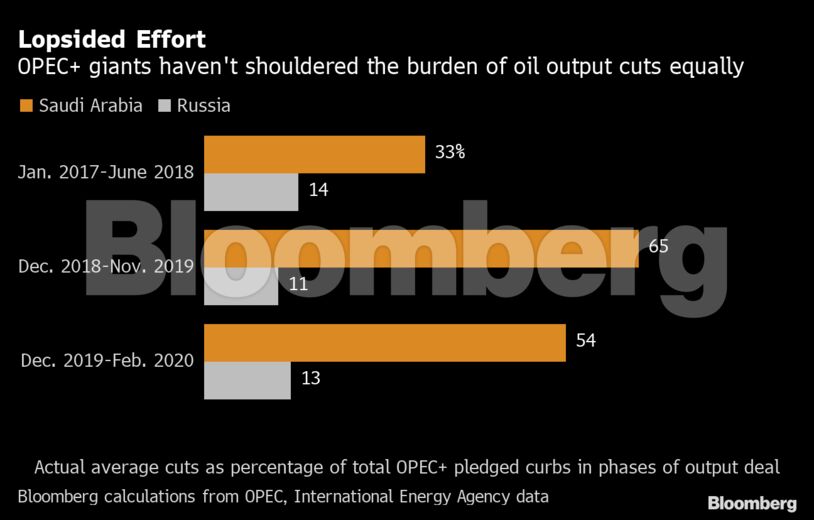

The Kremlin has gained a lot from its cooperation with OPEC. The country has been the biggest financial beneficiary of the cuts, largely because it’s borne a lesser share than Saudi Arabia. The alliance has also significantly enhanced President Vladimir Putin’s presence on the world stage and his political clout in the Middle East.

Following the collapse in oil prices this year as the economic impact of the coronavirus saps demand, the risks for the Friday meeting between OPEC and Russia are high. Not just for their alliance, but for the entire energy industry, from Exxon Mobil Corp. to smaller shale drillers in Texas, and oil-rich nations in Africa and Latin America.

The stakes in this game of diplomatic poker are huge — 1.5 million barrels a day of fresh oil cuts, plus 2.1 million of existing curbs OPEC+ agreed on last year that expire at the end of this month. That’s equivalent to the consumption of Germany and France combined.

Moscow appears to be betting that the oil market would re-balance by itself over the next few months as low prices take their toll. In particular, Russia believes that the U.S. shale industry is about to go in reverse. Exxon on Thursday announced it was slowing the pace of its flagship project in the Permian Basin.

Goldman Sachs Group Inc. earlier this week became the first major Wall Street Bank to forecast a contraction in consumption this year, suggesting that an even large cut may not arrest the drop in oil prices.

“Cutting production, 1.5 million barrels a day in April or May, is not really going to save you in the current environment,” said Jeffrey Currie, global head of commodities research at Goldman. “The demand damage is happening today, right now.”

Oil is now trading far too low to balance the budgets of most OPEC members. Riyadh needs more than $80 a barrel, according to the International Monetary Fund. Russia only requires a price of about $40 a barrel to balance its budget.

Share This: