CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

(Bloomberg) Another shockwave is about to rip through a world economy already reeling from the coronavirus.

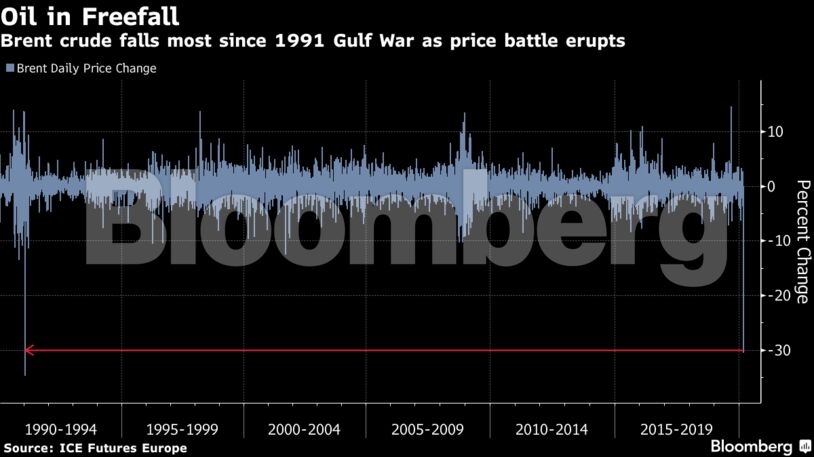

Oil prices plunged after the dramatic breakdown of talks between OPEC and Russia prompted Saudi Arabia to launch a price war. Brent crude tumbled by almost a third to $31 a barrel on Monday, as Goldman Sachs Group Inc. told clients it could quickly dip into the $20s.

Such an extraordinary slump, if sustained, would savage national budgets from Venezuela to Iran, threaten the heartland of America’s shale revolution and upend politics around the world. For central bankers, the prospect of destabilizing prices are an added complication as they try to model the impact of the coronavirus epidemic on the economy. And a long period of cheap oil prices could even hurt the fight against climate change by slowing the transition to renewable energy.

“Something like this could have more global repercussions than a trade war between China and the U.S. because oil touches so many things in the world economy,” said Rohitesh Dhawan, director of energy, climate and resources at Eurasia Group in London.

There are winners from rock-bottom oil prices — among them China, the world’s largest oil importer, whose recovery from the virus will be key for the global economy.

But this time is different. The U.S. — once a winner from low oil — is now an exporter rather than a buyer. And the hit to economic demand from the virus dulls the impact of any stimulus that cheap oil might provide. Oil shocks — on the way up — used to be feared for their impact on inflation. Now in a world where central bankers desperately pursue price growth, the opposite dynamic is at play.

“Lower oil prices will still not get people back in trains, planes, and automobiles, and stimulating the economic sectors most heavily hit,” said Stephen Innes, chief Asia market strategist with Axicorp Ltd. “But now we have a financial disaster brewing in the form of the shale industry meltdown.”

Russian Strategy

The crisis was precipitated when Russia refused to yield to a Saudi-led gamble to force Moscow to join OPEC in production cuts. OPEC presented a take-it-or-leave-it plan to slash production and throw a floor under prices. But Russia had another idea: its strategy was to squeeze American shale producers, which have flooded the market in recent years as OPEC+ nations held back their own production.

Now many of those U.S. operators will be losing money on every barrel of oil they produce and, unless there’s a dramatic recovery in the price, face bankruptcy. Even before Friday’s catastrophic meeting, banks were expected to restrict lending to shale drillers and a chunk of high-yield energy debt is already trading at distressed levels.

The last bust in the U.S. shale industry — when prices went as low as $26 — contributed to a manufacturing recession in 2016, when industrial regions, many in states likely to swing this year’s presidential election, saw a slowdown in orders from new shale oil projects.

Russia was willing to walk away from talks with OPEC in order to hurt U.S. rivals as it’s more resilient to lower prices. It has a floating currency — unlike Saudi Arabia — and can sustain its budget with lower oil revenues.

“Russia and President Putin are in a better position to fight this war than is Saudi Arabia or its Crown Prince,” said Chris Weafer, CEO of Macro Advisory, a Moscow-based consultancy.

The threat of economic — and even political — self-harm didn’t dissuade Saudi Arabia from launching a price war on Saturday in response to Russia’s refusal to cut production. But crown Prince Mohammed bin Salman will see his plan to retool the economy undermined as he moves to cement his political dominance.

Aramco Rout

Saudi Aramco — the national oil company listed on the stock market last year in a deal that put the prince’s credibility on the line — saw its shares plunge 9% on Sunday and another 10% on Monday in a sign of the instability ahead.

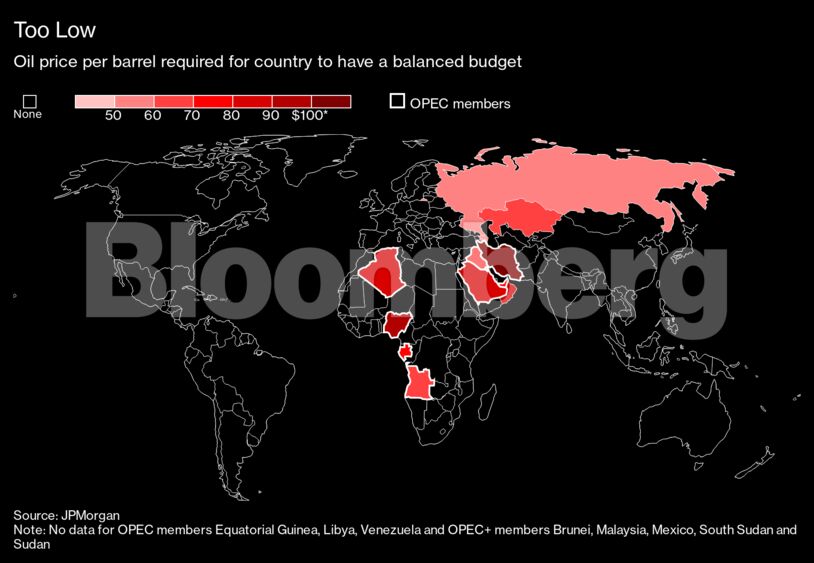

“Oil prices at sustained lows of $40 for five years is crisis time in Oman first, then Saudi Arabia and Bahrain, with defaults, peg devaluations, hefty spending cuts and higher taxes, with deep recessions and insolvent banks,” said Rory Fyfe, chief economist at MENA Advisors. At $20, it would force political change in Saudi Arabia and the region, he said.

The crash means Gulf powers may also end up with less cash to spend on conflicts in the wider region, according to Steffen Hertog, a Gulf specialist at the London School of Economics. That could favor Russia, which has been playing an increasingly prominent role in the region.

More immediate will be the shock to oil majors such as BP Plc, and their response will have ramifications well beyond their investors. Chief Executive Bernard Looney is trying to transform his company in the face of climate change, while also reducing debt and maintaining a generous dividend.

The payout is all but sacred — as it is for Royal Dutch Shell Plc — though market gauges already indicate investors doubt it’s sustainable. Looney vows he can maintain the dividend and become a greener company at the same time, though he underlined last month the need for a healthy oil and gas business to fund the transition. A price crash will push balance sheets to the limit.

“Sharply lower oil prices for a sustained period with a concurrent OPEC+ driven supply shock and virus demand shock almost certainly means oil majors’ energy transition plans and climate ambitions will be obstructed or slowed, at least in the near-term,” said Will Hares, an analyst at Bloomberg Intelligence. “In the face of oil at $40 or lower, these companies will be battening down the hatches. The first priority is protecting the dividend.”

The crash imposes another body blow for credit markets, thanks to the energy industry’s outsize share of U.S. high-yield securities. America and Europe were already shutting down to new debt issuance, and the oil crisis now threatens to trigger an outright funding squeeze should distressed borrowers prove unable to roll over maturing debt. Premiums on U.S. junk bonds soared last week to 550 basis points over Treasuries, the highest since 2016.

Going Green

A slowdown in green plans isn’t the only risk the price crash could pose for the transition to a cleaner economy. Cheap fossil fuels tend to encourage their use — increasing emissions — and dissuade users from switching to alternatives.

On the flip side, lower oil prices could allow governments to cut subsidies and increase taxes on fossil-fuel consumption and use revenues to invest in renewable projects, said Ivetta Gerasimchuk at the International Institute for Sustainable Development. And for Europe — which is leading the charge on climate change policies — the impact of cheap oil is still an economic boost, potentially giving governments more room to fund green projects.

The key question is how long the rout continues. OPEC+ members appear to be keeping the channels of communication open and Russian Energy Minister Alexander Novak said the alliance wasn’t dead even as he swept out of Vienna on Friday, leaving his counterparts in shock. But each side wants the other to blink first.

“The Saudi intention is to force Russia back to the negotiating table by engineering an oil price collapse. Most structural indicators suggest, however, that Russia is more resilient to lower oil prices than Saudi Arabia, so it’s not clear this will work,” said the LSE’s Hertog, author of ‘Princes, Brokers, and Bureaucrats: Oil and the State in Saudi Arabia’.

“In the end, this will be Putin’s decision, but we could be in for a lower-for-longer oil price scenario.”

Share This: