CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By David Fickling

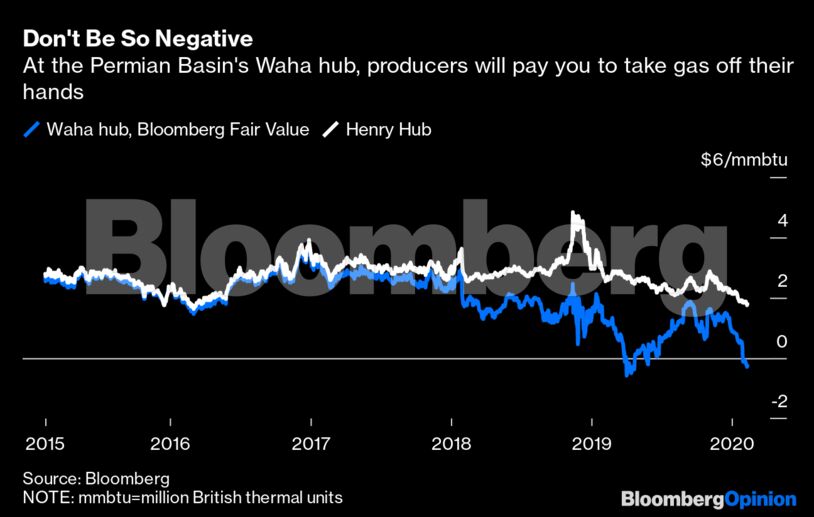

Gas prices at the Waha hub in Texas’s Permian basin fell to minus 26.8 cents per million British thermal units this week. They’re heading in an even more “aggressively negative” direction, commodities broker OTC Global Holdings told Bloomberg News, as a shortage of pipeline capacity makes producers jostle for a place in the queue.

Selling a commodity for a negative price isn’t quite as crazy as it sounds. Indeed, it’s a relatively common occurrence. Fuel oil — the gloopy fraction of crude used by boilers in ships, buildings and power stations — has hardly ever earned positive margins for refiners. Instead, they aim to make their money on gasoline and diesel, treating fuel oil as a waste product from which they can extract a few extra dollars.

That’s the current situation with natural gas in the U.S. A growing proportion of output is produced not for its own sake but as a byproduct from shale oil fields, where operators don’t care about the price of gas as long as it doesn’t stop them earning a positive margin on their crude production.

Output of this so-called associated gas has increased nearly fourfold from 4.3 billion cubic feet per day in 2006 to 15 billion in 2018, according to the Energy Information Administration, making up about 37% of shale gas production and 12% of total U.S. gas output.

With this super-cheap gas meeting the first leg of demand, the price at which the entire gas market clears is being driven lower. Thanks in part to an unusually mild winter, the Henry Hub U.S. gas benchmark has fallen by more than a third since its usual early-winter peak at the start of November, hitting its lowest level since 2016 this week.

Even this effect would have been a strictly local issue a few years ago — but as the global liquefied natural gas industry grows up, that’s changing, too. Traditionally gas prices in different regions had little relationship with each other, but the situation is giving way to one where the cost of U.S. exports, plus a margin for transport and conversion to and from LNG, is increasingly setting a unified global price.

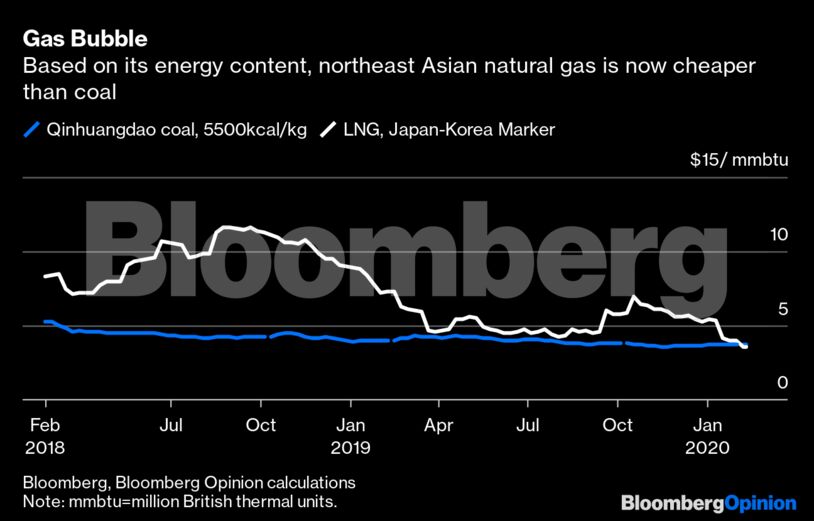

That’s likely to shake up many long-standing assumptions about the market. Asia has been mostly immune to the switch of coal-fired generation to gas which, along with the headlong growth of renewables, has caused the rapid shutdown of coal fleets in the U.S. and Europe.

Without the significant domestic gas reserves seen in those regions, prices in Asia simply haven’t been competitive enough. Except for brief periods in summer when gas demand is low, the Japan-Korea Marker gas benchmark has historically mostly priced its energy content at about twice what you’d pay for the same heating value of coal at China’s Qinhuangdao port.

That’s flipped so dramatically in recent months that even imported gas is now cheaper than coal on a heating value basis. When you take into account the greater efficiency with which most gas plants convert the energy in their fuel into electricity, the discount is even more pronounced. Any utilities expecting current low prices to be sustained ought to be looking hard at switching away from solid to gaseous carbon for any generation that renewables can’t easily supply.

There’s good reason to think this glut isn’t going away. China, a major driver of Asian gas demand in recent years, may be coming off the boil. Slowing industrial demand and a shift toward electricity rather than gas for replacing coal in centralized heating will push down demand, Morgan Stanley analysts wrote last month. Prices in Europe and Asia will potentially fall below $3 per million British thermal units, they wrote, approaching North American levels.

Add in the impact of coronavirus and Wood Mackenzie estimates demand this year will come to between 316 billion cubic meters and 324 billion, as much as 19% below the Chinese National Energy Administration’s estimates of 350 billion cubic meters to 390 billion.

LNG will take a smaller share of that shrinking pie, thanks both to rising domestic gas production and imports from Russia’s 38 billion-cubic meter Power of Siberia pipeline, which opened in December.

These conditions should cause producers to slow down — but if anything, things are going in the opposite direction. A record 71 million tons a year of LNG export capacity was commissioned in 2019, adding about 97 billion cubic meters to the global market, according to Morgan Stanley.

That pace will surely decelerate, with projects such as Exxon Mobil Corp.’s P’nyang looking increasingly unlikely to be developed. Still, should we see more success from the faltering crackdowns on flaring — the wasteful practice of burning off associated gas from oilfields — there’s another 140 billion cubic meters of gas supply out there that’s currently being vented into the atmosphere.

Rock-bottom prices for gas, wind and solar swept through the energy sector in the western hemisphere over the past decade. To date, only renewables have really made an impact in Asia. With a flood of new gas supply approaching, that dam could be about to break.

Share This: