CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Catherine Ngai, Grant Smith, Javier Blas and Dan Murtaugh

“When prices spike in response to geopolitical events, producers tend to lay on more hedges,” said Ed Morse, global head of commodities research at Citigroup Inc. in New York. “The higher the price the more they hedge,” which makes any increase short-lived, he said.

West Texas Intermediate crude, the U.S. benchmark, has slipped back below $60 a barrel as the last of the gains from President Donald Trump’s standoff with Iran faded. That didn’t just reflect the easing tensions after Tehran’s retaliation for the killing of General Qassem Soleimani inflicted no U.S. casualties. It was a manifestation of how the shale revolution has changed the psychology of the market.

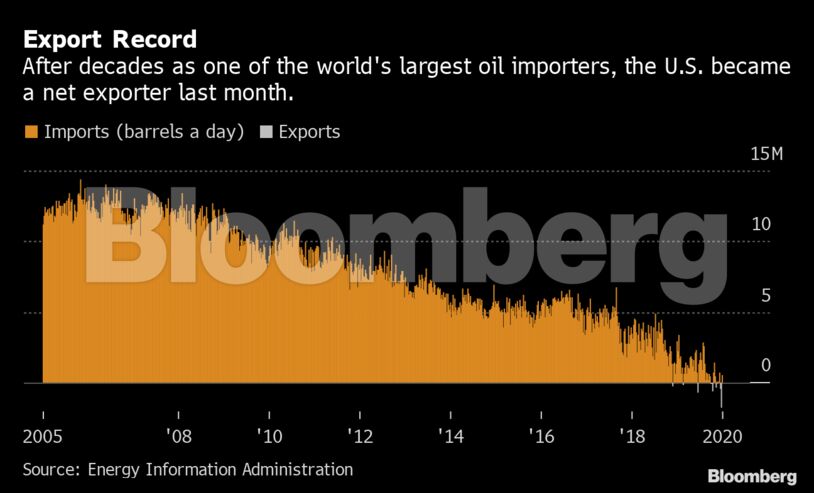

The same day that American missiles killed Iran’s most important military leader near Baghdad airport, the U.S. Energy Information Administration announced record net oil exports of 1.73 million barrels a day. That’s a historic change for a country that a decade ago was one of the world’s biggest importers, and it has changed the way the market responds to a crisis.

The shale boom that triggered this shift has been led by a multitude of independent drillers that are less able to absorb the financial impact of price swings than giants such as Exxon Mobil Corp. or Royal Dutch Shell Plc. Unlike the era that was dominated by the supermajors, any oil rally today finds a natural seller as smaller companies minimize their risks by hedging.

Crude prices are in the “sweet spot” for many North American producers, RBC Capital Markets analysts including Michael Tran wrote in a note. Many of them had been waiting, or hoping, for a chance to lock in WTI prices for 2020 at $60 a barrel, a level that was pierced after the Soleimani killing.

Occidental Petroleum Corp., one of the largest drillers in the prolific Permian basin in Texas and New Mexico, revealed this week it had increased its production hedges for 2020 from 300,000 to 350,000 barrels a day with the help of Wall Street banks.

“Hedging activity has been robust over recent weeks,” RBC said. “Volumes should only pick up as the price rally coincides with improving liquidity with the holiday season in the rear view mirror.”

Each burst of hedging gives a boost to U.S. oil producers, potentially allowing them to maintain higher output at a time when analysts are expecting shale growth to taper. Later this year, some of the crude linked to these contracts may fill the network of pipelines, terminals and ports connected to U.S. Gulf Coast, further solidifying America’s position as an energy-exporting powerhouse that offers a low-risk alternative to Middle Eastern oil.

Trump himself highlighted this shift in his Jan. 8 White House press conference after Iran’s retaliatory missile strike on a U.S. airbase in Iraq, saying that America is “independent and we do not need Middle East oil.”

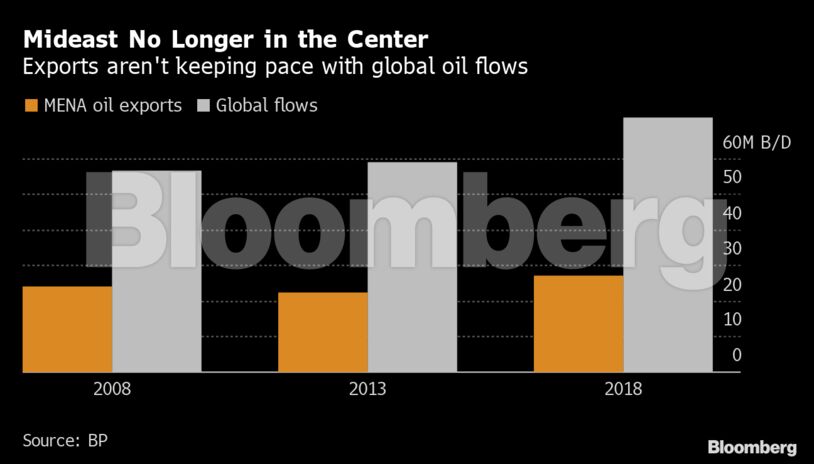

While the president’s boast is an exaggeration, the region’s dominance as an exporter has receded. Exports from the Middle East and North Africa accounted for 38% of the oil moved around the world in 2018, down from 43% a decade earlier, according to data from BP Plc.

Though some countries have boosted production capacity, others like Iran and Libya have seen theirs slashed by sanctions and conflict. In contrast, since the middle of the last decade the U.S. has seen its own oil exports soar from effectively zero to more than 3 million barrels a day—more than is shipped by any Middle East producer besides Iraq and Saudi Arabia.

A significant proportion of that crude is reaching Asia, the region that’s historically been most dependent on energy supplies from the Persian Gulf. Those alternative supplies, combined with a significant expansion in oil stockpiles, mean the region is better placed to withstand disruption.

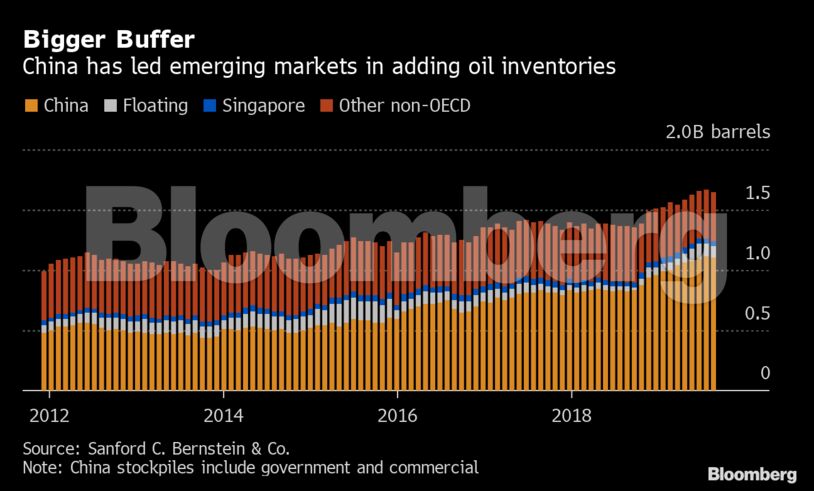

China, the world’s biggest oil importer, has built a massive government-owned stockpile that can protect it from short-term supply shocks. Its petroleum reserves have grown from about 191 million barrels in the middle of 2015 to about 800 million in September, according to Bloomberg calculations based on government statements. Saudi Arabia has also built up stockpiles in the past decade, including capacity for more than 8 million barrels on Japan’s Okinawa island.

“Emerging-market crude inventories are much higher than they have been historically, especially in Saudi and China,” Goldman Sachs Group Inc. analysts including Jeffrey Currie said in a Jan. 6 note. “Both countries are already demonstrating their willingness to use these to stabilize supply and prices.”

The muted reaction to the Soleimani crisis was the second time in just a few months that the market shrugged off serious turmoil in the Middle East. The strike on Saudi Arabia’s Abqaiq oil-processing facility in September—which the U.S. blamed on Iran—was the single biggest supply disruption in history, but the ensuing price surge fizzled out just two weeks later as the facility was repaired.

To be sure, both the attack on the kingdom and the assassination of Soleimani weren’t long-lasting crises, and fall back in prices also reflected the diminishing risk to supplies. But they were still major events compared with the kind of rumors that could send crude soaring a decade ago, such as the report of an Israeli training exercise that helped propel crude to almost $150 a barrel in the summer of 2008.

Industry veterans who cut their teeth on supply disruptions, such as the 2003 invasion of Iraq or the Gulf War of 1990 to 1991, are gradually being replaced by a younger generation whose careers developed in a world more accustomed to surplus than shortage.

Nowadays, “a rise in geopolitical tension is only good for sharp price spikes, but not for protracted strength,” said Tamas Varga, an analyst at PVM Oil Associates Ltd. in London.

Share This: