CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Julian Lee

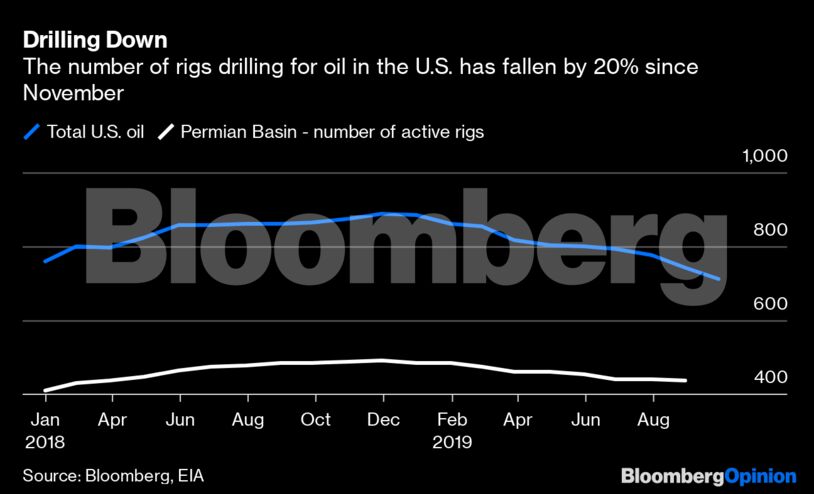

The number of rigs drilling for oil in the U.S. has fallen in each of the last 10 months, dropping by a total of 20% since November. And productivity gains are waning. Drilling in the Permian, the most prolific of the shale basins, fell by 11% in the nine months to August, according to the EIA.

The development of the U.S. shale patch is a bit like that of a person. During the first growth spurt in the four years to 2014 the industry was in the toddler phase. Everything was new and exciting, the toddlers stuck their fingers (or in this case their drill bits) into everything, just to see what would happen, and they pushed the boundaries in every direction. The toddler developed quickly, but the outside world taught it a hard lesson with a crash in the oil price in 2014.

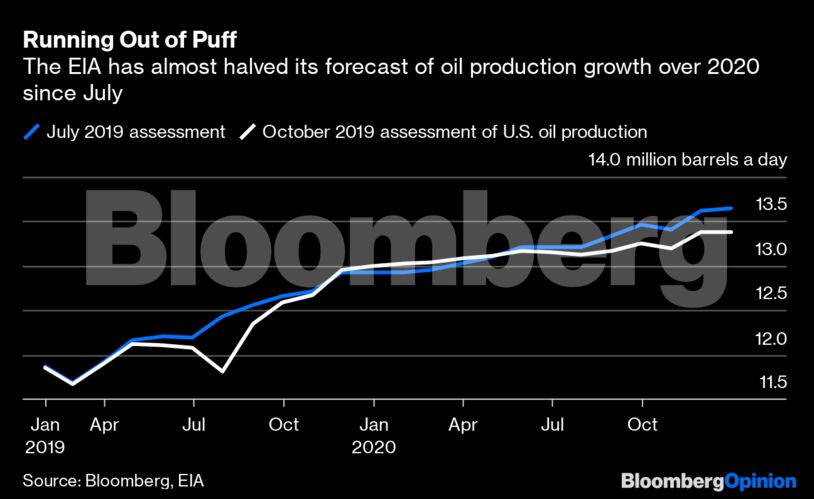

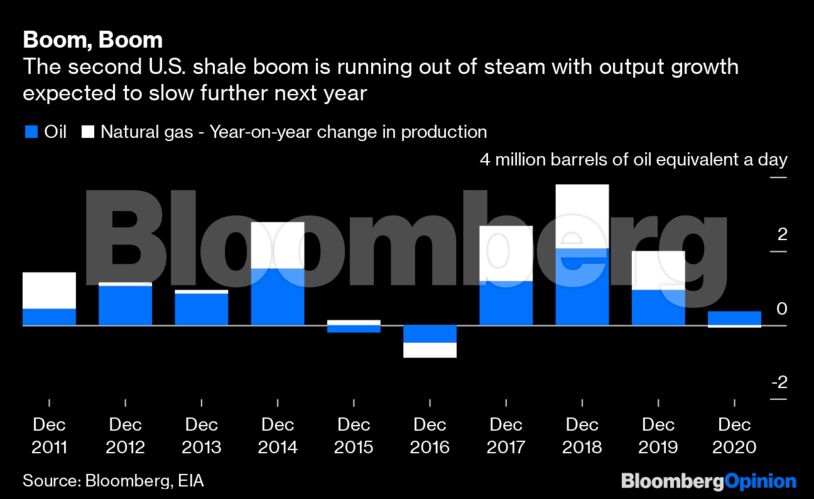

The second boom from 2016 has been more like the adolescent phase. After picking themselves up and learning to live in their changed world, the young adults developed their muscles and concentrated only on the things that interested them (the sweet spots in the shale deposits) to the exclusion of everything else. This focus has brought bigger output gains than the first boom. In the three years between December 2016 and December 2019 output is expected to have increased by 4.2 million barrels a day, compared with 3.9 million barrels a day between December 2010 and December 2014.

The biggest challenges of the second shale boom have been identifying and exploiting those sweet spots, consolidating acreage to enable the use of longer wells, and building infrastructure to move the gas and liquids to markets (including overseas).

But with a WTI oil price of about $50 a barrel, some in the shale patch are struggling. Shale companies are being forced to produce more to service their high debts, but they aren’t making any surplus profit to cut their borrowing or pay shareholders. Now those investors are starting to demand more of a return.

With the crude price seemingly stuck close to where it is — despite the tensions in the Persian Gulf region which flared up again on Friday — the next round of discussions between the shale producers and their lenders could be difficult. Some mergers may follow.

Yet fans of U.S. oil shouldn’t be disconsolate. The end of the second shale boom will usher in a third: the period of young adulthood. This will bring a range of new skills, but production will grow at a more measured pace.

This third boom will be driven by the international oil majors and will be characterized by a focus on better extraction, rather than rapid output growth. The application of enhanced oil recovery techniques, consolidation of ownership, automation of drilling, and rationalizing of supply chains will increase the volume of oil extracted over the lifetime of a well and reduce costs. But it won’t deliver the same pace of growth as seen recently.

The recovery rate of oil from shale deposits is typically about 5%-10%, but ConocoPhillips has pushed recovery as high as 20% in some parts of the Eagle Ford shale play in Texas, and it could reach 40% under the right circumstances. The upside to the lifetime recovery rate from Eagle Ford would be huge, potentially extending higher production rates for longer.

The third shale boom is coming. Just don’t expect it to look like the first two.

Share This: