CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Sharon Cho and Grant Smith

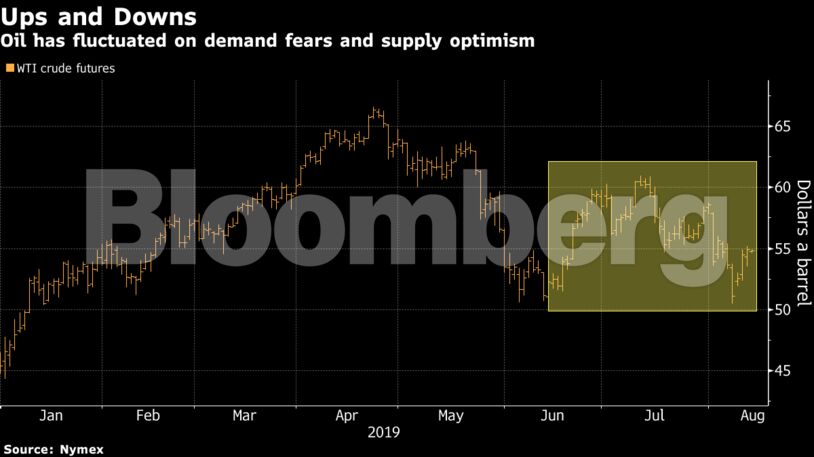

Oil is still down more than 6% so far this month on concern that global demand will continue to slacken as economic growth cools, and may fade further if the U.S.-China trade dispute intensifies. That worry has kept a lid on prices even as Saudi Arabia and Russia signal that the OPEC+ alliance remains committed to output cuts, and as the kingdom indicates it may be prepared to do even more.

“We still have an undecided oil market,” said Ole Sloth Hansen, head of commodity strategy at Saxo Bank A/S in Copenhagen. “That may be surprising, given the renewed verbal intervention from oil producers increasingly frustrated to see that their medicine — production cuts — isn’t having the desired effect.”

West Texas Intermediate crude for September delivery slipped 5 cents, or 0.1%, to $54.88 a barrel on the New York Mercantile Exchange as of 10:49 a.m. London time. The contract advanced 43 cents to settle at $54.93 on Monday, the highest close since Aug. 2.

Brent for October settlement lost 18 cents to $58.39 on the ICE Futures Europe Exchange. The contract closed little changed on Monday after rising 4.1% in the previous two sessions. The global benchmark crude traded Tuesday at a $3.66 premium to WTI for the same month, close to the narrowest since March 2018.

U.S. crude inventories have declined by about 9% since early June to stand at around 439 million barrels as elevated summer demand whittles away supplies.

| Other oil-market news: |

|---|

|

Share This: