CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Liam Denning

Over in the power sector, Vistra Energy Corp.’s CEO, Curtis Morgan, fielded a similar question for similar reasons. While professing “faith” in public markets, he added that going private must be considered if the stock’s perceived discount doesn’t ultimately close.

There are specific reasons why this question was asked of these two companies. Hamm owns almost 77% of Continental anyway, so the free float is currently valued at just $2.8 billion. Vistra, meanwhile, has private equity deep in its DNA, being one piece resulting from the 2007 buyout of TXU Corp. and run by an alumnus of Energy Capital Partners LLC.

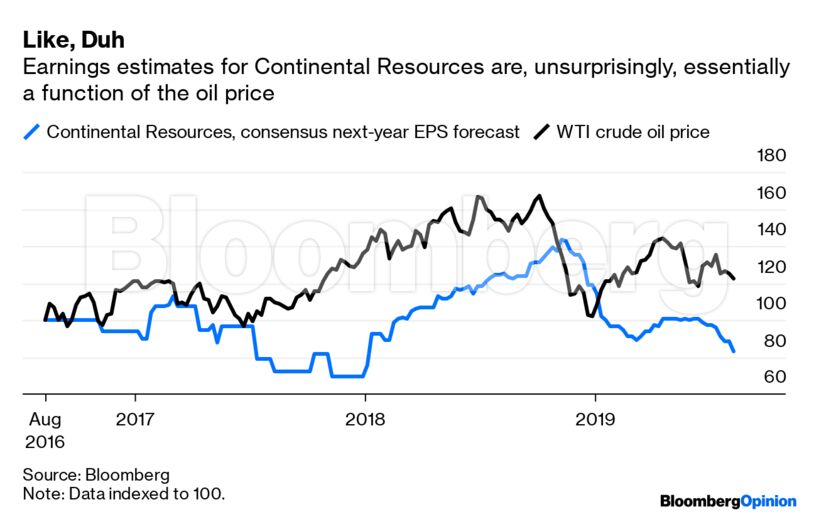

Public markets aren’t paragons of rationality, with the wisdom of the crowd repeatedly giving way to the mania of the mob. But it’s tough to argue the market is “broken” here. After all, if it’s irrational now, then wasn’t that also the case five years ago, when Continental traded at about $80 just as oil prices began to slip? Recall the company sold its hedging book around that time, ditching its insurance against an oil crash, with Hamm in November 2014 telling, coincidentally, the same analyst:

… We feel like we’re at the bottom rung here on the [oil] prices and we’ll see them recover pretty drastically, pretty quick.

Clearly, there isn’t a public-market monopoly on getting stuff wrong.

The private market has its own checkered record in energy. There have been obvious blowups, such as KKR & Co. Inc.’s forays with Samson Resources Corp. and, of course, TXU. Vistra’s sector, merchant generation, has a long history of keeping bankruptcy judges busy, which is precisely why it’s one of only two public companies left – and why both are diversifying into more stable retail operations.

Continental and Vistra have sold off for similar and quite rational reasons. Oil and gas prices are in the tank, and forecasts for Continental’s earnings take their cue from that. Similarly, as expectations of a hot and profitable summer in the Texas power market have cooled off, so Vistra’s stock has dropped with power futures.

This cuts both ways, and investors with a bullish view on energy prices are free to swoop in. They haven’t. That may reflect such ordinary things as fear of a recession, but I think it has more to do with a deterioration in one longstanding reason to own energy stocks: gaining exposure to the underlying commodity.

Chalk it up to a mixture of hindsight and foresight. Investors have noticed, especially with E&P companies, that past windfalls generated by price rallies tended to accrue to drilling budgets and executive compensation instead of them. Looking ahead, fundamental shifts in the energy market – from shale to renewables to peak demand forecasts to trade wars – inject volatility and raise doubts about long-term pricing. Rather than put a big multiple on future earnings tied to commodity prices and growth, investors prioritize near-term free cash flow that can underpin dividends – show me the money, in other words.

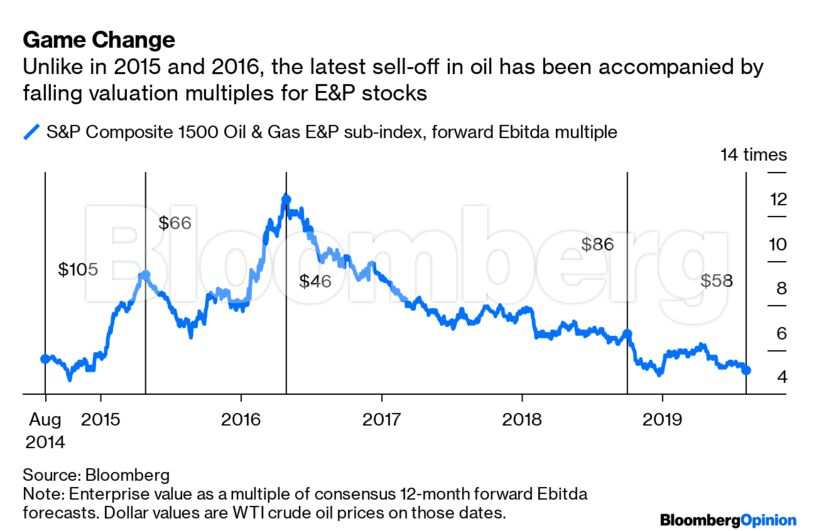

You can see this in E&P valuation multiples. Traditionally, these swung low when oil prices were very high, in anticipation of an inevitable cyclical downswing, and rose when prices fell, pricing in the next recovery. In this latest cycle, however, that relationship has changed. When oil prices fell sharply in 2015 and 2016, valuation multiples soared (and equity issuance spiked). But when oil dropped in late 2018 and this summer, multiples fell alongside it.

Similarly, while Bloomberg NEF reports Texas’ wholesale electricity market is the tightest it’s been since the lucrative summer of 2011, investors aren’t paying up for the option in Vistra’s stock. That may be a trust thing, in part, as the timetable for deleveraging set by Vistra when it bought Dynegy Inc. has slipped. But it also reflects the quite reasonable concern that new renewable capacity, especially solar power, could loosen Texas’ electricity market quite quickly – as has happened in the past.

The higher risks around energy earnings and damaged trust means investors demand more to buy into them – meaning a higher cost of capital expressed in lower valuations.

Herein lies a lesson for Saudi Arabian Oil Co., to give it its full name. The seemingly endless saga of Aramco’s IPO has been dogged by the $2 trillion market-cap target voiced by Prince Mohammed Bin Salman in 2016. As I wrote here, that number reflected a simplistic valuation of Aramco’s vast reserves, even though today’s oil investors prioritize dividends partly because they suspect barrels not due to be produced for another few decades may never see the light of day. Just like earnings streams for Continental and Vistra, the benefit of the doubt, expressed as a high multiple, has diminished.

Talk of an Aramco IPO was revived, somewhat jarringly, in the same week Saudi officials were trying to talk up sagging oil prices. Maybe the IPO talk remains just that, but it could also mean Saudi Arabia may actually go ahead, even if that finally buries the $2 trillion fantasy. Facing chronic deficits, Riyadh could use the money; and, as cynics often contend, the public market is where the dumb – that is, cheap – money is to be found. The one catch is that, when it comes to energy, the dumb money looks a little wiser these days.

Share This: