CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Energy dominance begins at home, and that includes any beachfront property you might have.

The Interior Department unveiled on Thursday a draft proposal for leasing areas of the U.S. outer continental shelf for oil and gas drilling between 2019 and 2024. As five-year plans go, it’s an ambitious one, envisaging leasing on fully 25 out of 26 planning areas — from sea to shining sea, as it were:

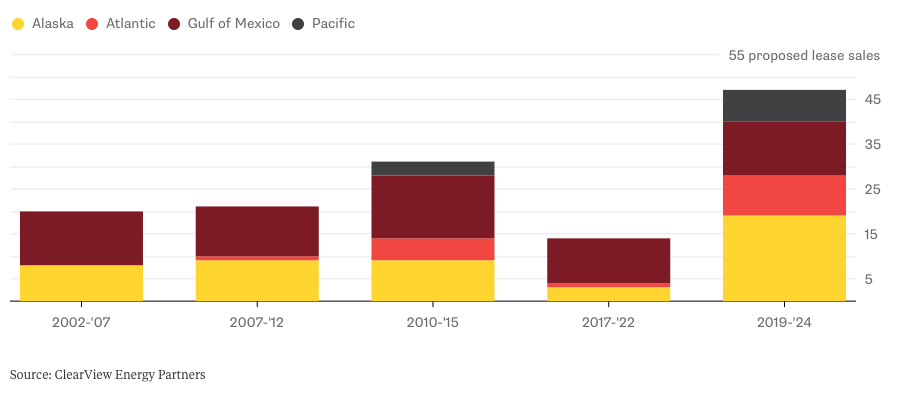

Rigged

The latest draft proposal for leasing drilling rights on the outer continental shelf of the U.S. is much more ambitious than prior efforts, both in scale and spread

ClearView Energy Partners (which provided the data for that chart) points out in a report published on Friday morning that the proposal is probably padded for a purpose. Interior knows the list will get whittled down over time, so it’s starting bigly.

For an oil and gas industry seeking new prospects, that makes the proposal at least partly a mirage.

It’s not that there aren’t potentially good prospects out there. Alaska and the Gulf of Mexico are obviously well-developed in certain areas already. The waters off southern California are also tempting. Meanwhile, using a little Pangaean jigsaw-puzzling, West Africa’s prolific fields suggest there may be similar riches off the Eastern Seaboard.

And it’s not like major oil companies are brimming with exploration prospects right now. The energy crash crushed spending on discoveries, with 2017 seeing the fewest on record, according to Rystad Energy, a consultancy. Another firm, Wood Mackenzie, estimates just $37 billion will be spent on exploration this year, down more than 60 percent from 2015.

There are two big complications when it comes to capitalizing on America’s federal waters, though: politics and time.

Kevin Book of ClearView Energy Partners says one of the biggest potential prizes is the eastern Gulf of Mexico. This is, roughly speaking, the area to the right of an imaginary line drawn down from the border of Alabama and Florida. These waters have the advantage of relative proximity to both the known geology and infrastructure of existing fields elsewhere in the Gulf.

Unfortunately for the oil industry, they also have proximity to Florida. On Thursday, Governor Rick Scott, not widely known as a bleeding heart, joined other state politicians in opposing the proposal. He has good reason to, given he is expected to challenge Democrat Bill Nelson for his Senate seat in November and the two will likely duke it out to see who can portray themselves as the more valiant defender of Florida’s beaches.

Furthermore, in keeping with the padding strategy in Interior’s proposal, the White House may well be willing to cut a deal that keeps the region out of bounds if it helps Scott win an extra Senate seat, given Republicans’ recent loss in Alabama took them to a razor-thin majority in the chamber. It may seem strange to join a set of dots that somehow link President Donald Trump, Steve Bannon, Roy Moore, and the continued absence of rigs in sight of Sarasota, but all I can say is: 2018, baby.

Much of the East and West Coasts also constitute politically hostile, or at least difficult, territory. In theory, a driller could develop a prospect using a self-contained floating, production, storage and offloading vessel, dispensing with the need to secure state permission for pipelines and terminals to bring oil and gas ashore. In practice, that would be prohibitively expensive, even with oil having crept back above $60 a barrel.

Apart from absolute dollars of expense, it’s the risk premium that would deter a rush into many of these areas. An oil company bidding for a lease off the coast of, say, Georgia, would have to factor in the best part of a decade for exploration and development, even before factoring in the brake of legal challenges. And if a lot can change in just a year or so, then a hell of a lot can change in five or 10 years.

Exacerbating this timing issue is the industry’s own recent experience. As I wrote here, oil majors paid a heavy price for tying up capital in giant, multi-year projects, trashing their returns and threatening their dividends when prices crashed. Added to this, intimations of oil demand’s eventual mortality have crept into strategic thinking. Mega-projects are decidedly unfashionable at this point. Short production schedules — such as in shale — are hot.

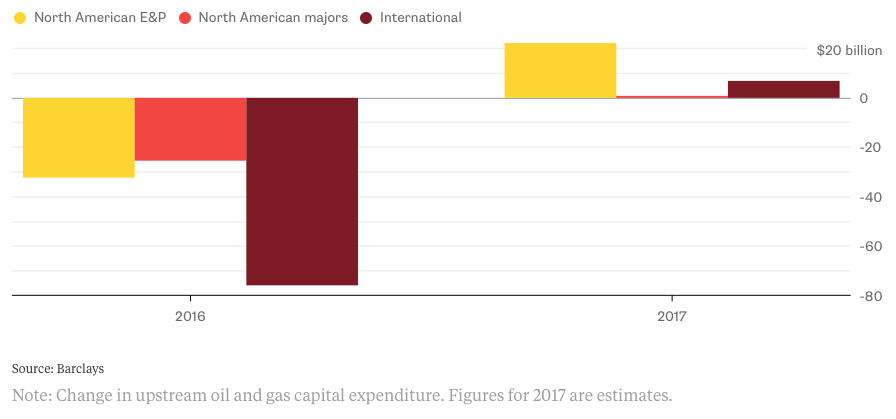

You can see that in spending trends. While capital expenditure in North America by both independent exploration and production companies and oil majors fell heavily in 2016, the region accounted for the vast majority of extra spending last year. And most of it came from smaller E&P companies focused on shale:

A Kind Of Energy Dominance

Spending on North America shale development plunged in 2016 but has led the charge back

Offshore spending isn’t dead. Some operators, such as Norway’s Statoil ASA, have worked hard to cut costs and shorten schedules to make projects work at lower prices.

In the Gulf of Mexico, William Turner of Wood Mackenzie authored a recent report forecasting oil and gas production to reach a record of 1.94 million barrels of oil equivalent per day in 2018.

However, he cautions that exploration spending there will remain flat this year and activity will focus on less-ambitious projects, such as those tying back to existing fields and infrastructure. Current energy pricing, and the renewed focus on staying nimble when it comes to deploying capital, are powerful restraints.

And these challenges would be magnified in new, relatively undeveloped areas. Turner points out, for example, that the swiftness of the Gulf Stream, a wide current running parallel to the Eastern Seaboard, could present big challenges to drilling on the Atlantic shelf.

These are the obstacles confronting the administration’s latest push to advance its “energy dominance” mantra, especially in the near term. Similar to what we’ve seen with efforts to revive coal in the face of cheap natural gas the immediate political gratification is obvious. Translating it into reality in the face of an implacable marketplace is altogether different.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Share This: