CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Takeaways by Bloomberg AI

- TotalEnergies SE is under pressure to show it can sustain payouts and deliver returns from its push into low-carbon energy as debt climbs and shares lag behind peers.

- The company has cut its quarterly stock repurchase program to $1.5 billion from $2 billion and warned it could fall as low as $750 million next year due to a net debt that about doubled to $26 billion.

- TotalEnergies’ shift to low-carbon energy, including onshore and offshore wind, solar and batteries, has not yet yielded stellar returns, leaving some investors questioning profitability compared to traditional hydrocarbon projects.

TotalEnergies SE is under mounting pressure to show it can sustain payouts and deliver returns from its push into low-carbon energy as debt climbs and shares lag behind peers.

The French supermajor on Wednesday announced it was cutting its quarterly stock repurchase program to $1.5 billion from $2 billion and warned they could fall as low as $750 million next year.

On Monday, Chief Executive Officer Patrick Pouyanné will meet investors and analysts in New York with a host of thorny questions to address: an underperformance of the firm’s shares against peers, as well as France’s CAC 40 index; ballooning debts; whether a refocus to oil and gas — like rival BP Plc is attempting — might be necessary. Even political chaos in France is on the agenda for some investors at home.

At the same time, the 62-year-old CEO has poured capital into onshore and offshore wind, solar and batteries — so far without stellar returns. The shift appeals to some European investors but leaves others questioning profitability compared with its traditional hydrocarbon projects.

“There’s been some disappointment on first-half cash flows, and hence on metrics like net debt,” said Pierre Alexis Dumont, chief investment officer at Sycomore Asset Management in Paris.

There will also be pressure to give a timeline of oil and gas projects that will feed cash flow in coming years, progress on divestments and so-called farm-downs of up to 50% stakes in renewables assets.

Wednesday’s decision to cut buybacks is designed to help TotalEnergies to contend with a net debt that about doubled to $26 billion in the 12 months through June, and a challenging outlook for the oil market, in which the International Energy Agency is anticipating a record supply-demand surplus next year. A glut in liquefied natural gas is also looming in a few years as Total and rivals are building new export facilities in the US, Qatar and elsewhere.

“Without clear communication on profitability or capital discipline, its diversification is no longer reassuring investors, but instead making them nervous,” Isabelle Zhang, an analyst at AlphaValue, said in a note. “Without clear monetization of low-carbon investments or margin recovery in LNG and Downstream, the equity may increasingly be valued not as a ‘green premium,’ but as a conglomerate discount.”

To curb borrowings, Pouyanné said in July that Total may divest $3.5 billion of assets by the end of the year. That would include new stake sales of solar and wind projects at various stages of development with a view to boosting the firm’s return on green investments. That’s as the firm has gone deeper into renewables than its European peers BP Plc and Shell Plc.

Oil and Power

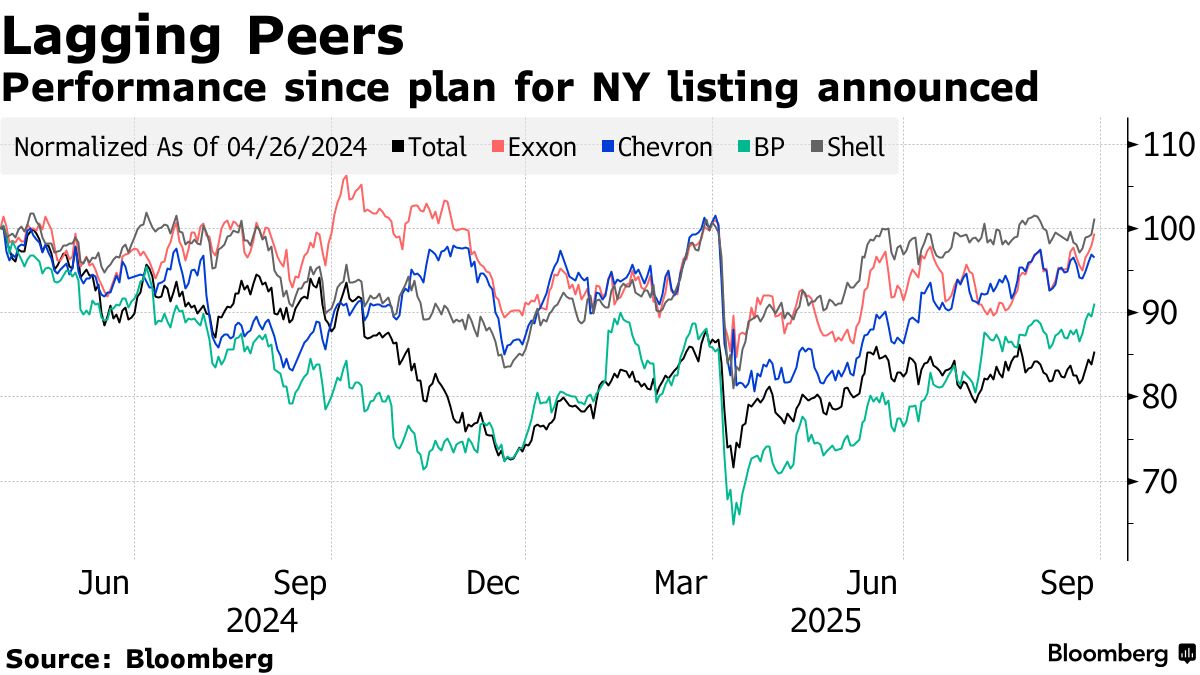

Total’s stock has been under pressure for months. Since April 2024, when it said it would change its American Depositary Receipts listed in New York into ordinary shares in an effort to attract US investors, they have underperformed those of other majors.

Shares in the French company have dropped about 15% in that time in dollar terms as it grappled with issues at some of its refineries, weaker European petrochemical markets, and lower trading profits in hydrocarbons. The CAC40 slipped slightly while the STOXX Europe 600 Index gained in the same timespan. TotalEnergies declined to comment on the company’s relative performance.

Power Investments Weigh on TotalEnergies

Capital employed in billions of dollars, and return on average capital employed in %

Note: Figures are for the 12 months ended June 30, 2024 and June 30, 2025

The slide in TotalEnergies stock has also coincided with a tumultuous period in French politics.

Two months after Total’s ADR announcement last year, President Emmanuel Macron dissolved parliament and called snap elections, ushering in a period of instability that’s driven government borrowing costs higher and prevented the CAC40 from joining a broad rally in European equities fueled by defense and bank stocks.

“The demand is for global or US indexes, not French indexes,” said Amundi Chief Investment Officer Vincent Mortier, who argued that an increase in passive investing through ETFs is a major problem for the biggest French stocks. “We’re in a phase where they buy the STOXX 600 but they don’t buy the CAC.”

— With assistance from Mitchell Ferman

Share This: