CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

LONDON, April 27 (Reuters) – Henry Ford was right all along, it turns out.

After decades of honing just-in-time global supply networks, car companies are going back to Ford’s founding principle of self-sufficiency.

Ford’s iconic River Rouge complex in Dearborn Michigan made its own iron and steel, supplied by company freighters from its own iron ore and coking coal mines in Michigan and Kentucky.

World War One had created material shortages and disrupted logistics. Ford’s answer was to take full ownership of the automotive supply chain from mine to product.

Auto companies are facing up the same problems today, compounded by the need to go electric, which means creating totally new metallic supply chains.

While Ford worried about iron ore and rubber, his successors are battling supply crunches and soaring prices in key battery inputs such as lithium, nickel and cobalt.

If “insane” lithium prices persist, tweeted Tesla (TSLA.O) CEO Elon Musk, the company “might have to get into the mining and refining directly at scale.”

He’s not the only automotive executive thinking about minerals self-sufficiency.

“Henry Ford … was right,” according to current incumbent CEO of Ford Motors (F.N), Jim Farley. “The most important thing is we vertically integrate.” The company intends to take control of its supply chains “all the way back to the mines.” read more

LITHIUM BRAKES

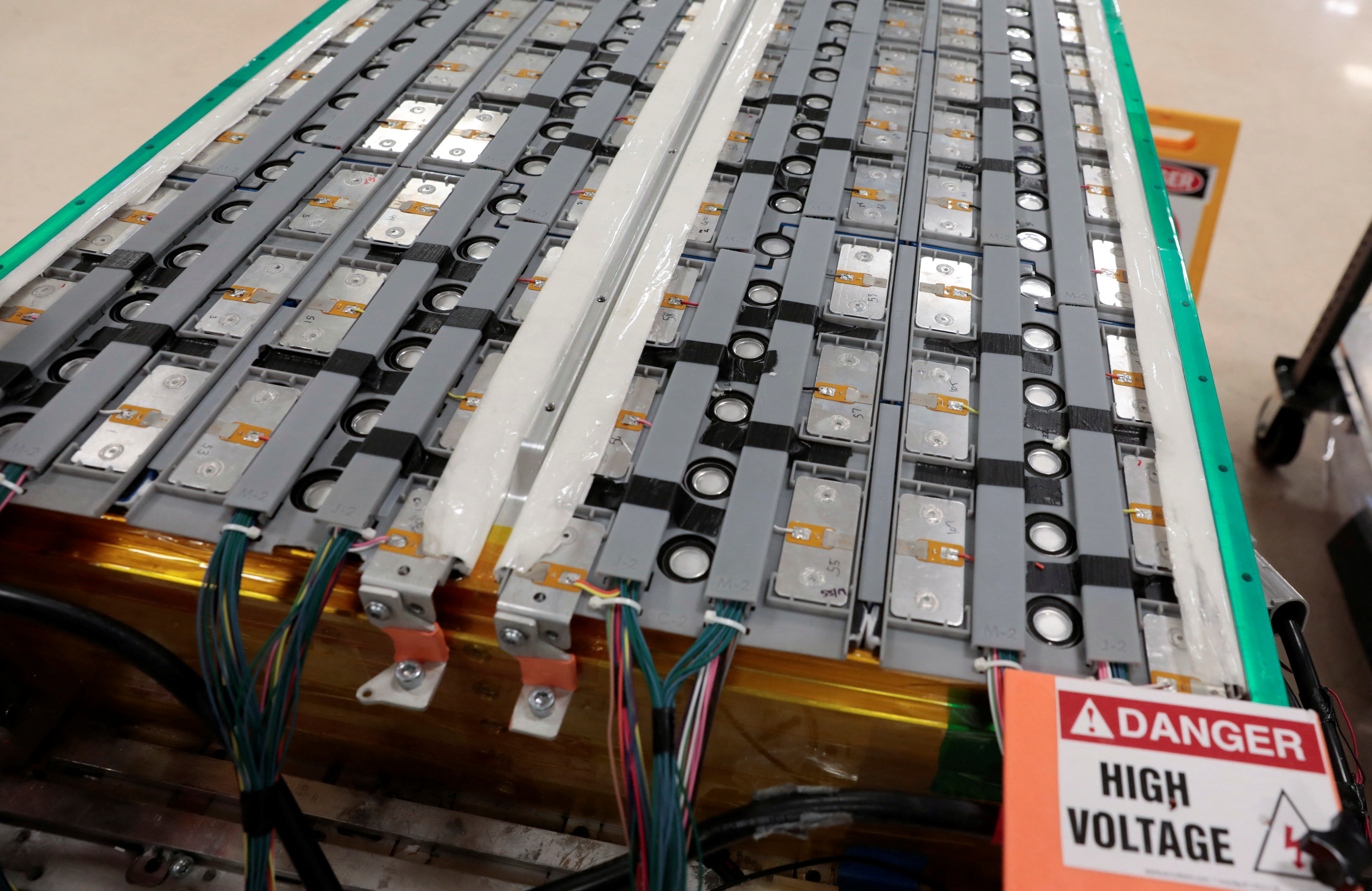

The problem facing every automotive company is the surge in the cost of lithium-ion batteries, which has forced many, including Tesla, to raise electric vehicle (EV) prices.

Battery-pack costs had previously been on a long-term downtrend riding on the back of incremental technical improvements. The sudden turnaround in EV pricing threatens the collective goal of reaching price parity with internal combustion engines.

Runaway battery metal prices are to blame.

Cobalt has nearly tripled in price since the start of 2021. Nickel turned so wild in March the London Metal Exchange (LME) had to suspend trading. At a current $33,600 per tonne it is up 59% on the start of January.

Battery-makers have responded by using more lithium-iron-posphate chemistry, which doesn’t use either cobalt or nickel, but that has only served to tighten up the lithium market itself with spot prices doubling since the start of the year.

Metals accounted for 40% of battery costs in 2015, a ratio that has risen to 80% this year, according to consultancy Benchmark Minerals.

The common theme is of supply failing to react fast enough to a step-change in demand as EV sales accelerate and the world builds ever more gigafactories to supply the necessary batteries.

Prices may lose some of their recent heat but there are few who expect a full return to previous lower trading ranges.

That’s a big headache for every automaker. But for some it may prove existential.

Benchmark Minerals warns of the potential for supply deficits to grow over the coming years. “Even in the most optimistic scenarios where every single raw material project in the pipeline comes on stream and existing operations expand aggressively, there will not be enough raw material for the battery supply chain as we go into 2030.”

Insufficient metals supply risks putting a brake on the EV revolution with those unable to source enough facing the prospect of lower output and slower roll-out times.

The industry’s current semiconductor problems “are a small appetizer to what we are about to feel on battery cells over the next two decades,” RJ Scaringe, CEO of EV start-up Rivian Automotive, told the Wall Street Journal.

METALS RUSH

Fear of high prices and fear of missing out completely are driving automakers upstream “all the way back to the mines”.

Tesla is itself something of a trail-blazer, making no secret of its ambitions to manufacture its own batteries with metal sourced directly from miners.

It has future tonnages committed from lithium projects in the United States and Australia and an off-take agreement with Talon Metals Corp’s (TLO.TO) proposed Tamarack nickel mine in Minnesota.

BMW Group has tied up both cobalt and lithium supplies for its upcoming fifth generation of battery cells and will make “the raw materials available to the two battery cell manufacturers, CATL and Samsung SDI,” the company said.

It’s an example of an automaker taking ownership of battery metals from cradle to grave and quite possibly beyond if commercial recycling of lithium-ion batteries takes off.

Volkswagen (VOWG_p.DE) has moved beyond simple off-take deals, forming an alliance with China’s Tsingshan Group and Huayou Cobalt (603799.SS) to mine and refine enough nickel and cobalt to generate 160 gigawatt hours worth of EV batteries. read more

The battery metals rush is already on and Musk’s tweet inevitably generated a few ripples across the mining stocks sector. Or at least it did before he decided to buy Twitter itself before a lithium miner.

However, the market logic of insufficient supply and elevated pricing means it may be only a matter of time before Tesla and other EV makers start getting into the dirty business of mining the stuff themselves.

The biggest headwind to more lithium and nickel supply is capital. New mines cost a lot of money and come with an extended development time of several years.

Price volatility doesn’t do anything to reassure traditional lenders and the paper market is still too illiquid to hedge the financial risk.

Automakers can deploy a lot of capital. They have already done so at the battery manufacturing stage of the supply chain. Extending that vertical integration into the mines that produce the enabling metals is now becoming a matter of urgency.

Those who miss out will risk seeing the EV revolution accelerate away from them.

The opinions expressed here are those of the author, a columnist for Reuters

Share This: