CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

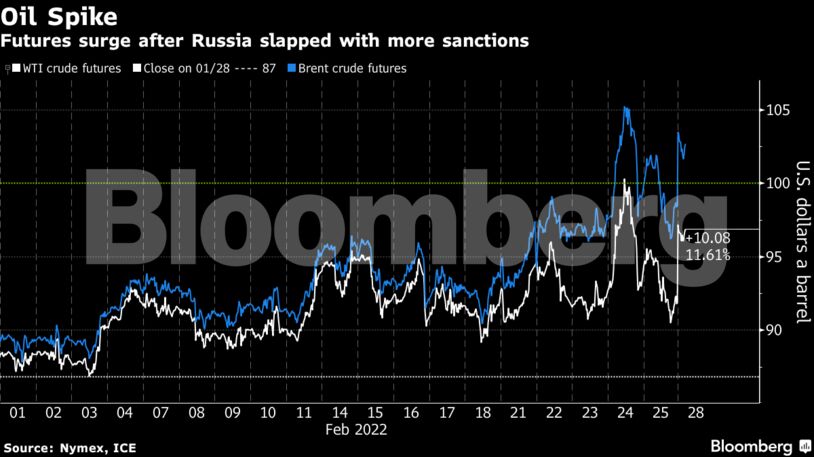

Brent futures jumped as much as 7.3% on concern that oil supply — already stretched amid rebounding demand — may tighten further should Russian flows be disrupted. Some customers have paused purchases of the country’s flagship Urals grade, while Asian buyers are trying to secure more Middle Eastern crude.

Western nations agreed over the weekend to exclude some Russian lenders from the SWIFT bank messaging system, and targeted the central bank’s foreign reserves. BP Plc also moved to dump its holding in oil giant Rosneft PJSC, taking a financial hit of as much as $25 billion.

“Removing some Russian banks from SWIFT could result in a disruption of oil supplies as buyers and sellers try to figure out how to navigate the new rules,” Andy Lipow, president of Lipow Oil Associates in Houston, said in a note.

Russia’s invasion of Ukraine has roiled markets from energy to metals and grains, heaping more inflationary pressure on a global economy already grappling with soaring costs. At least two of China’s largest state-owned banks are restricting financing for purchases of Russian commodities, underscoring the limits of Beijing’s pledge to maintain economic ties with one of its most important strategic partners in the face of Western sanctions.

Against this volatile and fast-moving backdrop, OPEC+ faces a trickier task than usual when it meets on Wednesday to discuss supply policy for April. Despite the invasion, the cartel will probably stick to its plan of gradually increasing oil production, according to delegates. The group will also have to take into account the halt of some Iraqi output.

| Prices |

|---|

|

Demand destruction is the only thing that can stop oil shooting higher after additional curbs were unleashed on Russia, according to Goldman Sachs Group Inc. The bank raised its one-month forecast for Brent to $115 a barrel from $95, with significant upside risks on further escalation or longer disruption.

Brent is still deep in a bullish backwardation structure, highlighting investor nervousness over supply. The global benchmark’s prompt spread was $3.83 a barrel in backwardation on Monday, compared with $1.39 at the start of the month.

Russia pumped 11.3 million barrels of oil a day in January, according to data from the International Energy Agency. The IEA pledged last week to help ensure global energy security, while India said it would support initiatives to release emergency oil reserves to help calm prices.

The surprise move by BP indicates how far the West is willing to go to punish President Vladimir Putin for the invasion. The oil major has been in Russia for three decades and was staunchly defending its presence there just weeks ago. Norway’s Equinor ASA also said it would pull out from joint ventures in Russia.

Societe Generale SA and Credit Suisse Group AG stopped financing commodities trading from Russia, according to people familiar with the matter. The two banks, key financiers to commodity trading houses, are no longer providing the money needed to move raw materials such as metals and oil from Russia.

Share This:

REALITY: Trump Says America Does Not Need Canadian Energy. The Facts, and His Own Policies, Say Otherwise