(Bloomberg) Oil held steady as tensions between Saudi Arabia and the UAE escalated over the weekend, leaving the market with few clues about how supply talks will proceed on Monday after discussions reached an impasse last week.The Saudis are standing firm about raising output starting next month and extending the scope of the OPEC+ agreement to the end of 2022, while the United Arab Emirates wants better terms for itself. A failure by the group to raise supply may further squeeze the market, driving prices even higher and raising concerns over inflation. On the other hand, a breakdown in their unity could result in a free-for-all that crashes crude.“The market is now fearing several scenarios. One is that there is no new deal at all with no increase of production August onward with oil prices shooting much higher as a result,” said Bjarne Schieldrop, chief commodities analyst at SEB AB. “Another is that cooperation within the group falls apart altogether, for example, if UAE decides to leave the group” leading to a collapse in the oil price, he saidMost OPEC+ members backed a proposal to increase output by 400,000 barrels a day each month from August, and push back the expiry of the broader supply deal into end 2022. To agree to an extension, the UAE is seeking to change the baseline that’s used to calculate its quota, a move that could allow it to boost daily production by an extra 700,000 barrels.

Crude rose for a third month in June as widespread Covid-19 vaccinations have helped revive demand while OPEC+ has curbed supply. But prices at the highest in more than two years have raised worries over its impact on the global economy, and the White House is already voicing concern about increasing gasoline prices.

While demand signals are strong in Europe and the U.S., the virus is spreading again in parts of Asia, resulting in increased restrictions on movement.

Congestion in Jakarta was down 73% from a 2019 baseline, according to the most recent data from TomTom NV. That’s a sharper reduction than last March and April when the virus was first spreading around the world. Indonesia consumed 1.7 million barrels a day of oil in 2019, BP Plc estimates show.

Prices

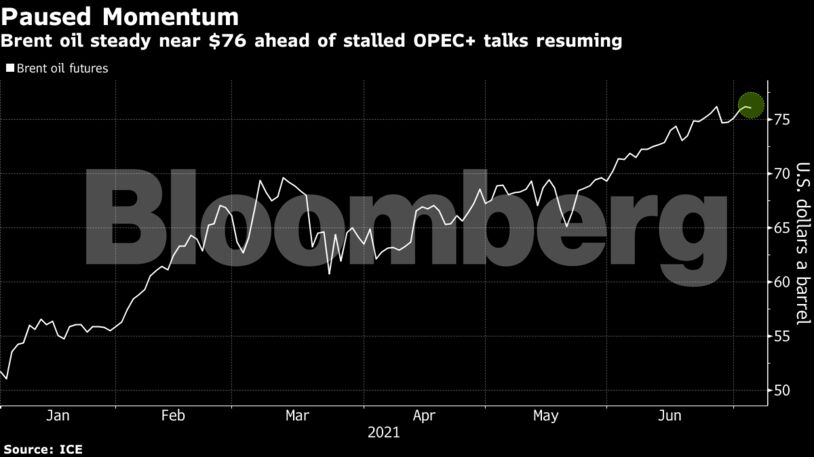

Brent for September settlement rose 0.4% to $76.48 a barrel at 10:05 a.m. in London, after gaining 0.4% on Friday

West Texas Intermediate for August delivery gained 0.3% to $75.38

Still, Morgan Stanley estimates global daily oil demand is set to increase by 3 million barrels from the May-June period to December. With little supply growth elsewhere, even the proposed increase from OPEC+ will likely keep the market in deficit. That will support Brent prices within the bank’s forecast range of $75 to $80 a barrel in the second half of this year.

Other market news:

Vitol Group, the world’s largest independent oil trader, expects the crude rally to continue on the assumption any OPEC+ output hikes will fail to keep pace with growth in demand.

Iraq said it was keen to improve conditions for international oil companies, after BP Plc and Russia’s Lukoil PJSC moved to sell down their assets in the crisis-wracked country.

CDN NEWS |

CDN NEWS |  US NEWS

US NEWS