CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Kevin Crowley

In addition to dropping vast swaths of gas assets from the development queue, Woods is capping capital spending at $25 billion a year through 2025, a $10 billion reduction from his pre-pandemic target.

This year has been particularly bruising for America’s most-iconic oil explorer. Exxon lost money for three consecutive quarters, an unprecedented streak, the shares dipped to an 18-year low and the company was ejected from the bosom of blue-chip stocks, the Dow Jones Industrial Average. Woods also plans to cut 15% of the company’s workforce by the end of next year.

From being the largest company in the S&P 500 Index as recently as 2012, Exxon now ranks just inside the top 50 as energy lost its luster and technology giants grew. Chevron Corp. now has a larger market valuation than Exxon.

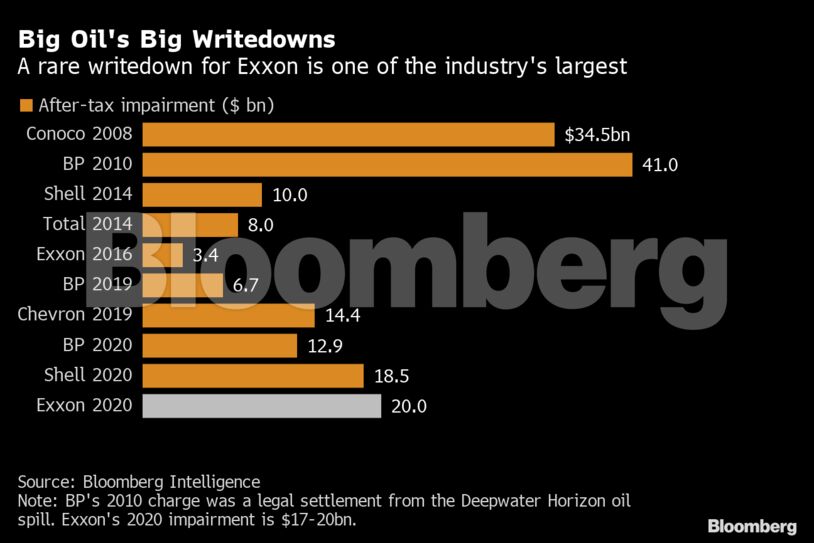

No Pivot

Unlike its European peers, Exxon has so far chosen to stick with its $15 billion-a-year dividend and has increased borrowing in recent months to fund it and its other capital priorities. On an annualized basis, the dividend has been increased each year for almost four decades.

Optimism that vaccines will soon restore global economic growth buoyed crude prices in recent weeks but the impact of the contagion on Big Oil is likely to be longlasting. With European giants Royal Dutch Shell Plc and BP accelerating the pivot to renewables and Exxon locking in drastic spending cuts, capital flows into big, traditional developments are expected to shrink in coming years.

Cowen & Co. analyst Jason Gabelman detected a subtle shift in Exxon’s word choices that may herald a dramatic change in financial priorities. Whereas company executives touted Exxon’s “reliable and growing dividend” during the third-quarter earnings conference call, Monday’s statement only mentioned reliability, the analyst said in a note to clients.

‘High-Grading’

“Continued emphasis on high-grading the asset base — through exploration, divestment and prioritization of advantaged development opportunities — will improve earnings power and cash generation, and rebuild balance sheet capacity,” Woods said in the statement.

Exxon has been warning shareholders since October that its gas assets were at risk of significant impairment. Previously, the energy titan’s largest writedown was for about $3.4 billion in 2016, according to Bloomberg Intelligence.

Assets removed from Exxon’s development plans include so-called dry gas resources in Appalachia and the Rocky Mountains, Oklahoma, Texas, Louisiana and Arkansas, as well as western Canada and Argentina, the company said. It will attempt to sell “less strategic” assets.

The writedown stems from former CEO Rex Tillerson’s decision a decade ago to buy XTO Energy for $35 billion rather than spend years building an in-house shale business. At the time, the outlook for North American gas prices was bright because demand was rising faster than supply.

Supply Glut

Instead, fracking was a victim of its own success, unleashing so much gas that it overwhelmed demand and the infrastructure needed to handle it, resulting in a prolonged stretch of depressed prices.

U.S. rival Chevron recorded an impairment of more than $5 billion on Appalachian gas a year ago, and recently agreed to sell those fields to EQT Corp. for about $735 million.

Share This:

COMMENTARY: 2025 Review of Global Energy Consumption – William Lacey