CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Julian Lee

Aramco, as the company is widely known, is creating a new corporate development organization that will focus on “portfolio optimization,” with a brief to “assess existing assets” and boost access to “growth markets and technologies.” It will be led by Senior Vice President Abdulaziz Al Gudaimi, who now heads up the company’s unprofitable downstream business.

The change, it said, “constitutes a refinement” of Aramco’s existing structure, not a fundamental organizational change. But it does suggest that the company is adapting itself to look more like its private sector rivals such as Exxon Mobil Corp. or Royal Dutch Shell Plc.

Aramco has never had to worry much about its portfolio of assets before. It developed oil fields at home in Saudi Arabia, building and operating the infrastructure to process, transport, export and refine its output. And, increasingly, it invested in joint ventures with overseas processors to refine its crude and lock in guaranteed markets. With huge profits to be made in the upstream sector of the business — finding, producing and selling crude oil — crude prices and production volumes have been the driver of corporate profit across the industry. But, as I wrote here, that’s a model that has been turned on its head this year.

Western oil companies have weathered the Covid-19 storm by slashing dividend payments, and in the case of the European majors, the successes of their trading departments — both things Aramco couldn’t tap.

Aramco has been hit twice by the pandemic and taken heavier blows than its competitors. First, the collapse in global demand triggered a rout in oil prices, taking Brent from almost $70 a barrel at the start of the year to below $20 in mid-April. Prices are now back around $45 a barrel, but have been stuck there, as the recovery in demand has faltered.

The second punch came from the Saudi-led OPEC+ response that saw the 23-nation group cut production by a record 9.7 million barrels a day in May. That slashed the volume of crude the company pumped by more than 4 million barrels a day, or 35%, between April and June. Under the current terms of the OPEC+ deal, output restraint is due to remain in place until April 2022.

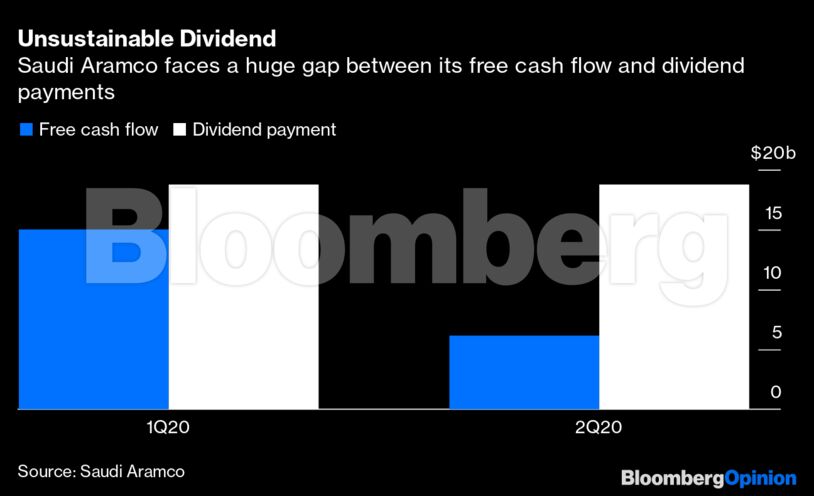

Aramco’s revenues have taken a battering. Free cash flow slumped to $6.1 billion in the second quarter, but the company maintained its $18.75 billion dividend payment. It had no real option. Before floating 1.5% of the company’s shares on the local stock market, its majority owner, the Saudi government, promised that dividend payments in 2020 wouldn’t fall below $75 billion.

Unless the company’s fortunes change dramatically, it will be impossible to maintain those payments without resorting to heavy borrowing. The company is unlikely to get much help from crude prices. Brent is forecast to average less than $42 a barrel this year, rising to $48 next year and $54 in 2022, according to the median of estimates in Bloomberg’s commodity price forecasts survey.

And it can’t just pump more oil. Aramco’s production should average 9 million barrels a day for the rest of 2020, rising to just under 9.5 million next year under the terms of the OPEC+ deal — that’s still about 250,000 barrels a day below what the company pumped before it embarked on its brief output surge in April.

Prior to Aramco’s IPO, JP Morgan Chase & Co. told prospective investors in a research report that under an “acid test” of crude at $40 a barrel and production of 9 million barrels a day — pretty close to the scenario facing the company this year — Aramco would only remain within its self-imposed borrowing target by cutting the dividend by 30% and slashing spending dramatically.

In this environment, it’s unlikely a simple strategy refinement will be enough. Aramco may have to rationalize what it already does. Earlier this year, it hired advisers for a potential multi-billion dollar sale of a stake in its pipeline business. It may be looking to shed other non-core assets. It says it’s still committed to a $10 billion refinery joint venture in China, denying it was suspending its involvement. However with dividend payments having to take priority, now may not be the moment to commit to a heavy investment that won’t deliver income for several years.

Perhaps because of its decision not to reduce payments to shareholders, Aramco’s stock has fared much better than those of its rivals. Its share price is down by less than 2% since the beginning of the year, compared with drops of 41% for Exxon and 48% for Shell.

The problem Aramco faces, though, is how to keep those dividend payments going until oil prices and production get back to comfortable levels. More actively managing its asset portfolio is one part of its response.

Share This: