CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Saket Sundria and Alex Longley

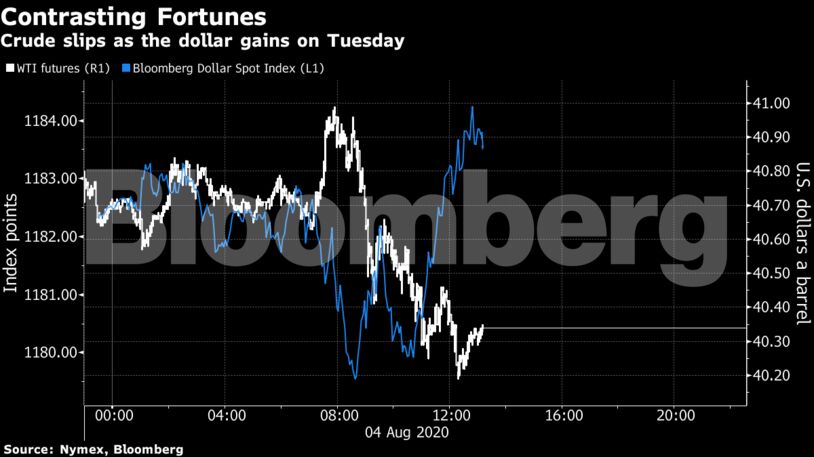

OPEC’s crude output rose last month, led by Saudi Arabia, ahead of the group and its allies relaxing their historic cuts this month, according to a Bloomberg survey. Weaker equity markets and a stronger dollar also weighed on oil prices on Tuesday.

There’s been a slew of mixed demand news this week. In Europe, airline EasyJet Plc said it would add additional flights after better-than-expected demand for travel over the summer. China’s vehicle sales jumped in July compared with the previous year, but state-owned refiner Sinopec has been processing less oil because of flooding. India’s diesel sales dropped sharply last month.

Oil has been stuck near $40 since early June as rising coronavirus cases in many parts of the world raise doubts about a sustained recovery in demand. The futures price curve is showing some weakness, with the three-month timespread for U.S. crude near the widest contango since May, indicating concerns about oversupply. That could potentially be made worse by returning output from OPEC+.

Also see: London Traders Hit $500 Million Jackpot When Oil Went Negative

“August will be a month of some price volatility,” said Paola Rodriguez Masiu, senior oil markets analyst at Rystad Energy AS. “With demand recovery stalling for a while amid Covid-19’s resurgence, supply indications will swing oil trading from gains to losses.”

| Prices |

|---|

|

The Organization of Petroleum Exporting Countries increased output by 900,000 barrels a day last month as Saudi Arabia, the United Arab Emirates and Kuwait restored additional production that was curbed in June when they amplified efforts to trim a glut. The market will also be watching this week to see if Saudi Aramco cuts the official selling price for its main crude grade for the first time since May.

| Other oil-market news |

|---|

|

Share This: