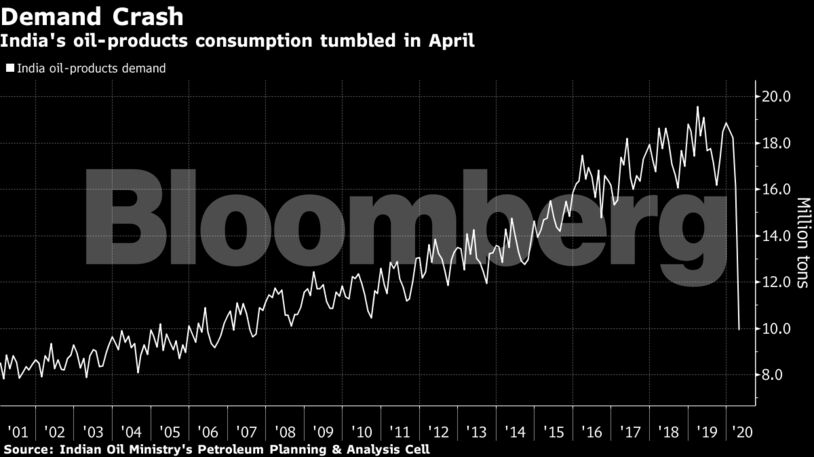

(Bloomberg) Oil pared last week’s gain as fears of a potential resurgence in global coronavirus cases countered tentative signs of a demand recovery.Futures fell 2.3% in New York to trade near $24 a barrel. China put Shulan, a city near the North Korean border, in lockdown over the weekend, while in the U.S., the White House was hit with a case of the virus even as President Donald Trump encouraged Americans to return to work. In India, data showed that consumption of oil products slumped 46% in April to a 12-year low.

“Weakness persists,” said SEB chief commodities analyst Bjarne Schieldrop. With a new virus lockdown in China, it is “not so strange that crude-oil prices are giving back some of their strong gains from last week.”

Prices

West Texas Intermediate for June delivery declined 58 cents to $24.16 a barrel on the New York Mercantile Exchange as of 10:58 a.m. London time

Brent for July settlement dropped 2.4% to $30.24 a barrel, after advancing 17% last week

There are signs that gasoline demand is picking up as parts of the world reopen for business. And in China, an economy emerging gradually from lockdown, oil stockpiles have shrunk in recent weeks after previously swelling to a record.

Investors have been returning to the crude market, with money managers last week holding the biggest net-long position in WTI in a little over a year, according to CFTC data released Friday.

But despite the optimism, there’s persistent concern that a relaxation of lockdown restrictions could bring a second wave of infections, pulling down oil demand once again.

The collapse in consumption caused by the pandemic has forced countries around the world to cut crude output. In the U.S., producers reduced the number of active drilling rigs by 33 to 292 last week, the lowest level since September 2009, according to Baker Hughes data.

Other oil-market news

Saudi Aramco is in early talks about further staggering payments for a controlling stake in petrochemical giant Saudi Basic Industries Corp. as the collapse in oil prices puts pressure on its finances.

Petroleos Mexicanos’s trading arm, PMI, has declared force majeure on some fuel cargoes, deferring others until later in the year, after measures to contain the coronavirus outbreak wiped out demand.

CDN NEWS |

CDN NEWS |  US NEWS

US NEWS