CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Nathaniel Bullard

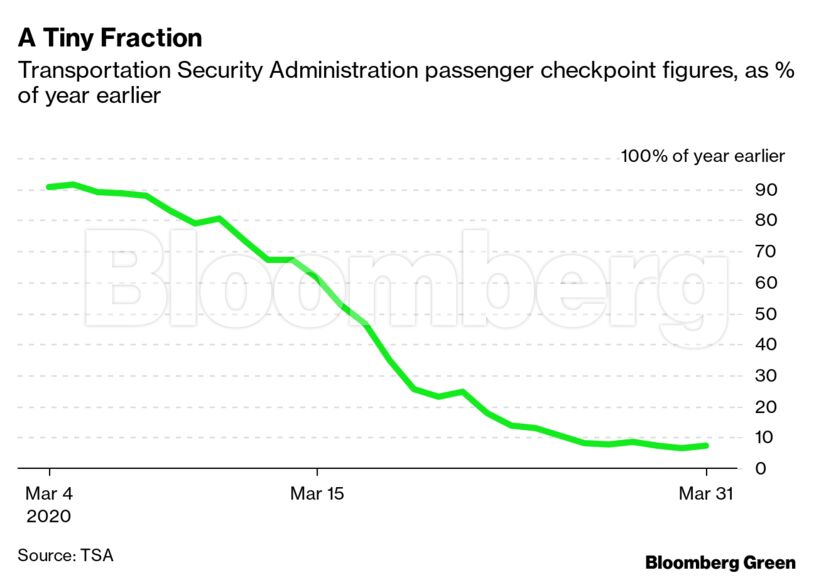

Here’s a bending market: U.S. aviation. On March 6, checkpoints run by the Transportation Security Administration processed nearly 2.2 million passengers. On March 31, the TSA processed all of 146,000—a nearly 93% decline.

Here’s another bending market, one bent so far it’s gone negative: On March 18, and again on March 30 and 31, producers of one grade of U.S. crude oil paid buyers to take it away. Wyoming Asphalt Sour, a very dense oil that’s mostly used to make road surfacing material, went for $-0.47 a barrel on Monday. That’s an extreme bend in the market, but it’s not quite broken (and it’s not strictly pandemic-related); it’s a function of supply and demand in an over-supplied market. It’s still a transaction, and if supply and demand generate a negative price, well then so be it.

Then there are the broken markets, where nothing is transacting at all. That happened elsewhere in the oil market, as Ecuador’s state oil company voided its spot price auction “as bids failed to meet minimum expectations.”

There’s another broken market in aviation. Last week, an auction for European Union aviation carbon allowances failed, with just four airlines bidding. Demand for air travel is so low, and therefore airlines’ energy consumption and emissions as well, that their need for permits has fallen to the point where there’s no market to be made.

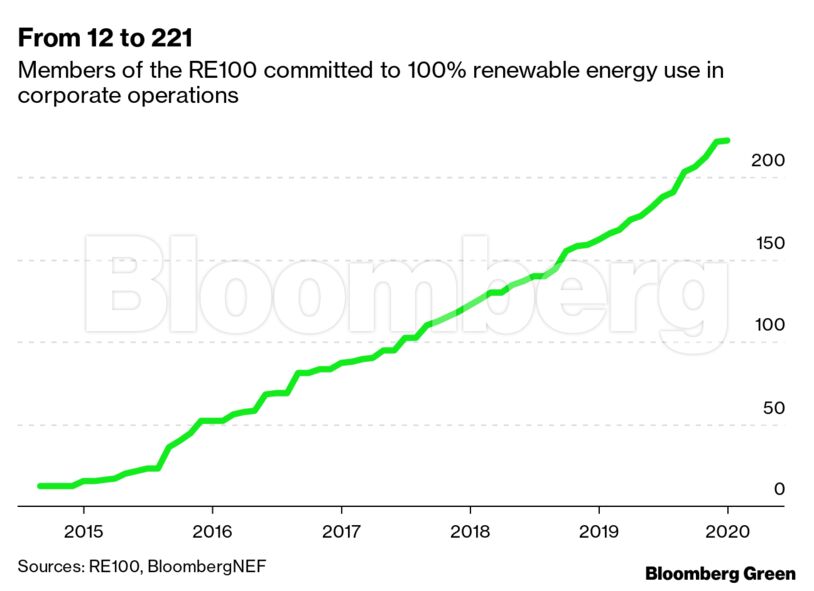

Looking ahead, it’s worth watching a few corporate sustainability markets to see how much they bend (or if they break) in our current economic climate. The first is the RE100, a group of corporations that have committed to meet 100% of energy demand with clean sources. There were 12 members when it was founded in 2014; now there are 221. How many more companies will make such a commitment given everything else corporate executives now have to focus on? Companies might not renege on commitments, and if they do, they probably won’t make much noise about it. But it’s quite possible that the rate of growth in RE100 members slows considerably.

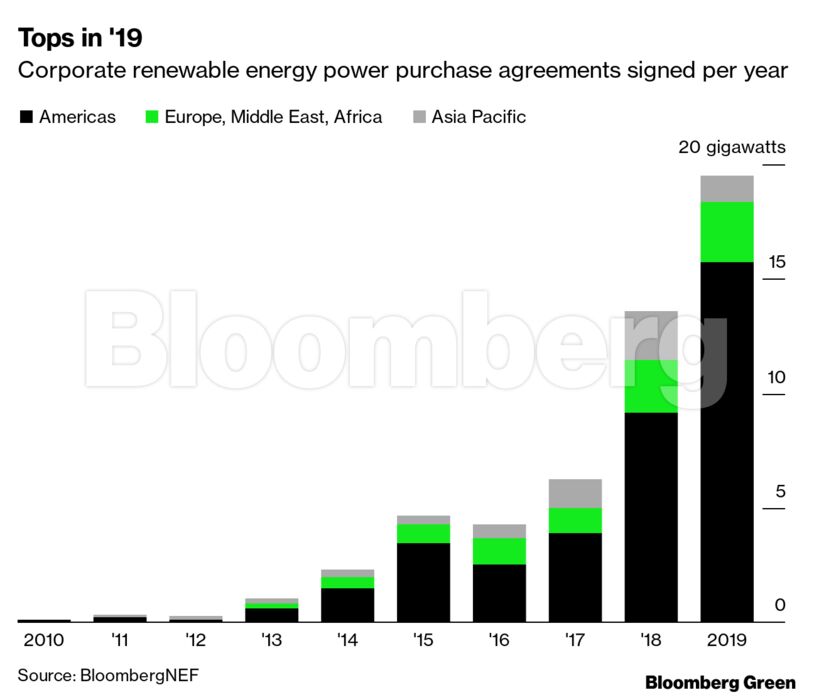

But there’s a more immediate—and more market-sensitive—place to watch this dynamic play out: corporate renewable energy power purchase agreements. Analysis by BloombergNEF shows that companies signed a record volume of such agreements for zero-carbon power last year, most of them in the Americas.

The appetite to sign more of these agreements will certainly be curbed. Falling power demand should depress power prices in most markets, making grid power more attractive. (Although in many places, renewables will still at least be competitive, if not the lowest-cost option.) From a CFO’s perspective right now, “sustainability” is probably more about keeping a business going than examining its electricity mix.

Keeping the lights on matters most right now. We’ll see if that imperative bends the corporate renewable power purchase market, and how far and how fast it does so.

Share This: