CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Elizabeth Low and Alex Longley

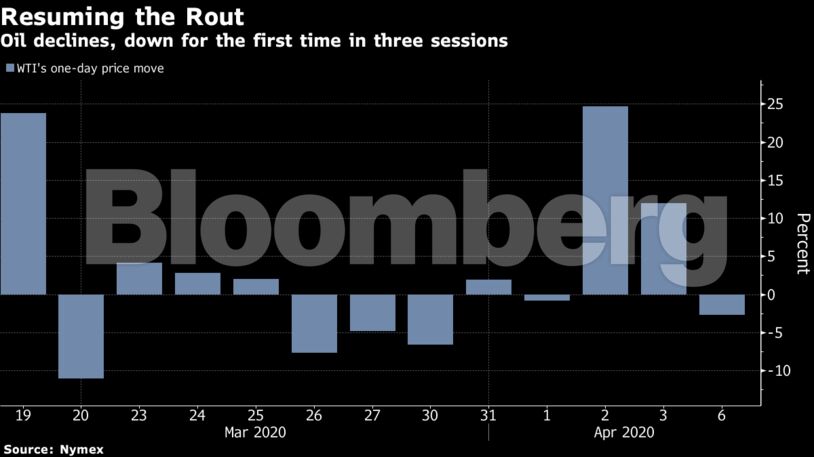

Futures fell 3.3% in New York, having earlier plunged 11%. Large oil-producing nations are racing to negotiate a deal to stem the price crash, but hurdles remain. A meeting of OPEC+ and others — already delayed once — is only tentatively scheduled for Thursday. Russia and Saudi Arabia want the U.S. to join in, but President Donald Trump has so far shown little willingness to do so.

“The fact that the OPEC+ alliance agreed to return to the negotiating table marks an important breakthrough,” said Stephen Brennock, an analyst at PVM Oil Associates. Nevertheless, the supply curbs being discussed “would fall short of the current loss in demand” and “would not prevent a further upswing in bloated global oil inventories.”

As crude futures fluctuate, the market for real barrels shows renewed weakness, trading several dollars below headline prices. Sellers from Russia to Congo are slashing prices in an effort to sell cargoes. At the same time, gasoline — a premium product in normal times — is currently unprofitable in Europe and barely profitable in America.

| Prices: |

|---|

|

Riyadh and Moscow are “very close” to an agreement on cuts, CNBC reported Monday, citing the head of Russia’s sovereign wealth fund. Still, a lack of participation from the U.S. — the world’s largest producer — could prove to be a stumbling block. Despite originally calling for a deal, Trump on Saturday described OPEC as a cartel and threatened tariffs on foreign oil.

Diplomats are now trying to stitch together a meeting of G-20 energy ministers for Friday, part of an effort to bring the U.S. on board, according to two people familiar with the situation.

Meanwhile, Saudi Aramco has delayed the release of its closely watched monthly oil-pricing list until Thursday to await the outcome of OPEC+ negotiations, according to people with knowledge of the situation. The U.A.E. signaled the same move on Monday, while also indicating that it had sharply increased production so far this month.

Share This: