CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

Talks between Russia and the Organization of Petroleum Exporting Countries have dragged on all week in Vienna as Moscow has resisted signing on to output reductions, delegates told Bloomberg News. With the market already looking well-supplied, OPEC’s technical experts are said to have recommended a cut of 600,000 barrels a day — considerably deeper than internal analysis that the virus will reduce demand by around 400,000 daily barrels for about six months.

Russia has its own immediate reasons for standing pat. The country’s oil output last year hit its highest level since the days of the Soviet Union, reaching around 11.25 million barrels a day. What’s more, it’s now in a situation that historically only Saudi Arabia and a few other Gulf countries have enjoyed, with spare capacity on hand — in the region of 500,000 barrels at day, enough to give it a role as a swing producer for the world.

There’s also deeper historical symmetry to what’s happening — one embedded in the five-decade struggle between Russia and Saudi Arabia for supremacy in the global oil market.

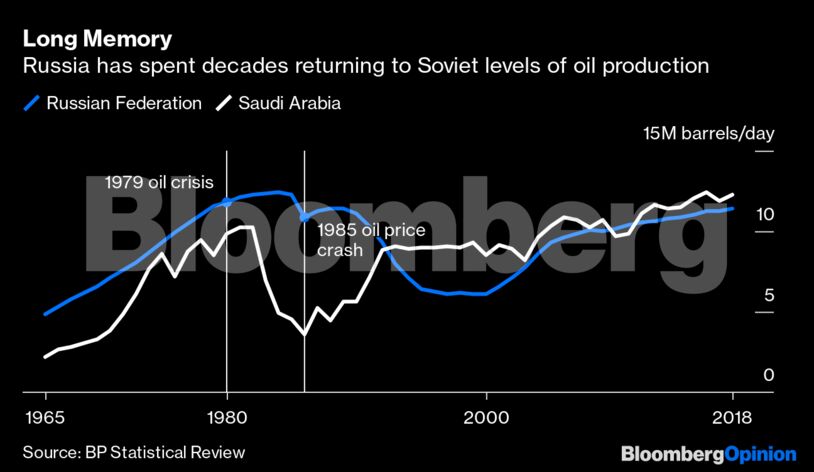

Oil played an under-appreciated role in the fall of the Soviet Union. As the USSR’s industrial and agricultural economies started to falter in the 1970s, it was an oil boom that kept the nation’s head above water. Buoyed by the sharp rise in prices as a result of the 1973 and 1979 oil crises, the country opened up vast petroleum reserves in Siberia. The hard currency earned paid for grain imports to feed a burgeoning urban population, as well as funding its ruinous war in Afghanistan.

That spending was largely financed by Saudi Arabian restraint. With demand from wealthy oil importers collapsing as a result of the new, higher prices and supply from non-Gulf producers surging, the kingdom cut output by nearly two-thirds through the early 1980s in an attempt to re-balance the market and lift prices. Something had to give — and the result was disastrous for Moscow.

“The timeline of the collapse of the Soviet Union can be traced to September 13, 1985,” according to Yegor Gaidar, the economist and politician who drove many of Russia’s wrenching reforms in the early 1990s. On that date, Riyadh’s oil minister, Sheikh Ahmad Zaki Yamani, abandoned the policy of supporting prices and elected to flood the market instead. Saudi Arabia, as the lowest-cost producer, was able to survive. As my colleague Clara Ferreira Marques wrote recently, the high-cost USSR was dealt one of many mortal blows.

“Oil production in Saudi Arabia increased fourfold, while oil prices collapsed by approximately the same amount in real terms” after the Saudi move, Gaidar later wrote. “As a result, the Soviet Union lost approximately $20 billion per year, money without which the country simply could not survive.”

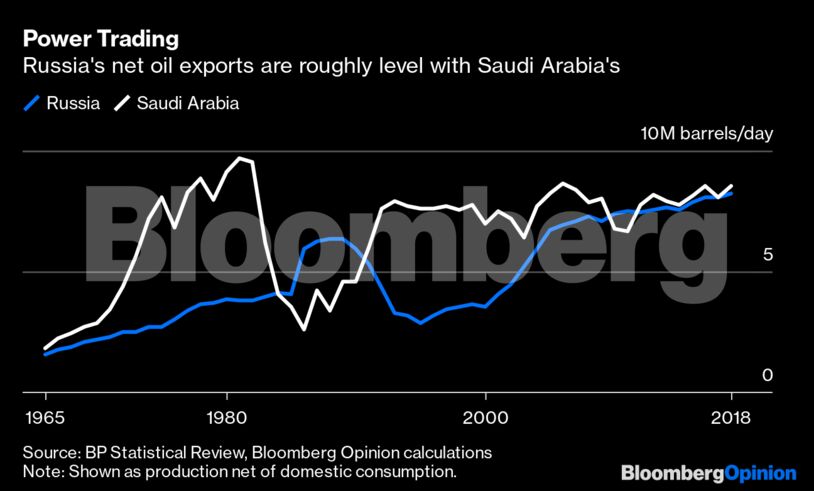

From one angle, the past 30 years of Russian energy policy has been a long, slow grind back to the position it enjoyed in 1985. Shorn of its oilfields in newly independent republics in the Caucasus and central Asia, it took until 2007 for output to move above 10 million barrels a day again. Nowadays, even exports are level-pegging with those from Saudi Arabia, despite Russia’s far bigger domestic economy. This time, though, the tables have turned.

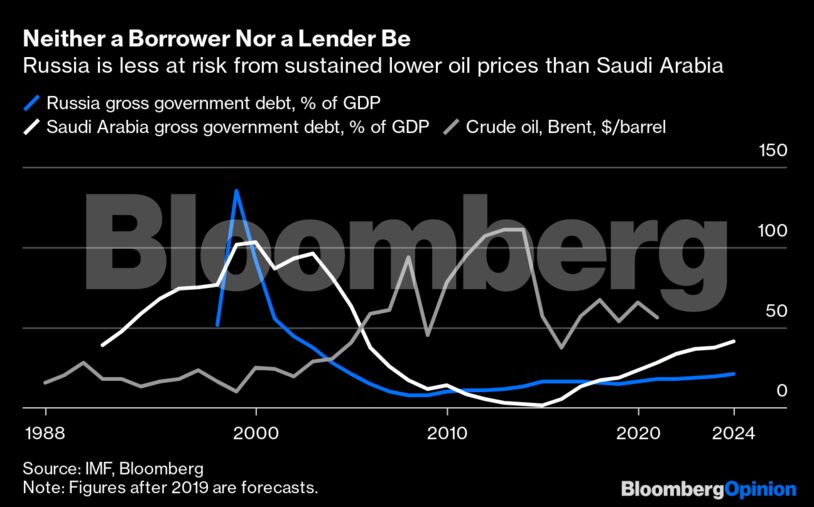

While Saudi Arabia can still boast some of the lowest production costs in the world, its bloated spending means that it needs a price of about $85 a barrel to balance its budget, compared with about $50 in Russia. Neither country is a major debtor, but Saudi Arabia’s borrowing, projected by the International Monetary Fund to hit 41% of output by 2024, is far more of a burden than Russia’s. Like Russia in the 1980s, Saudi Arabia can’t feed itself, depending on imports for 88% of its food supplies. Riyadh even has a military quagmire in Yemen to parallel the Soviet Union’s disastrous foray into Afghanistan.

There remains a good chance that Moscow will eventually bow to the wishes of OPEC members and cut production. As my colleague Liam Denning has written, Russia is famous for falling short on its promises of output restraint — indeed, it regularly makes noises about quitting the OPEC+ arrangement altogether. Still, at current prices of $53.76 a barrel for Urals crude, even Russia could do with more of a fiscal cushion.

Both nations will then face a deeper problem. While Moscow and Riyadh were focused on their unhealthy relationship, the U.S. has in recent years overtaken both countries to become the world’s leading producer. Worse still, oil demand itself is fast approaching a plateau.

The world’s energy markets will change drastically over the coming decade. This is no time for two of the biggest producers to be consumed by a decades-old rivalry.

Share This: