CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Bloomberg News

Meanwhile, Donald Trump began the era as a reality TV star and will finish it as president and Tariff Man, with his America First agenda whipsawing billions of dollars in investment flows around the world. It all leaves investors dodging political bombs, recession fears and disappearing yields even as they close out the decade with some of best gains in a generation.

Seeking clues on what lies ahead, Bloomberg reporters chronicle here how the past 10 years has transformed the major asset classes.

Bonds: Return-Free Risk

From risk-free return to return-free risk: The world of fixed income got turned upside down as bears went into extinction and every sell-off proved little more than a head-fake.

At its peak a record $17 trillion stockpile of negative-yielding securities roiled global markets in 2019 — spurring capital gains for holders while saddling the likes of pension funds with loss-making investments down the road.

Benchmark 10-year Treasury yields are a shadow of their former selves, with those in Germany and Japan at epic lows. Thank demographics, growth angst, vanishing inflation, or monetary interventions. Whatever your worldview, the takeaway is the same: Interest rates failed to wake up from the crisis slumber.

“These yields echo that the ghost of the Great Recession is still continuing to circulate through global capital markets,” said Jack Malvey, a debt veteran and former chief global fixed-income strategist at Lehman Brothers Holdings Inc. “With little room left for return in bonds, the big question for the 2020s is when does the mean reversion come?”

The Bloomberg Barclays Global Aggregate Treasuries index has returned some 5% in 2019 alone through late December. It’s gained more than 19% since the start of 2010. Today coupons are paltry, if they exist at all. Further price gains look unlikely given the fierce starting point for valuations at the close of 2019.

Yet the risks couldn’t be greater. Duration, a gauge of how much prices decline as yields rise, is near record levels while outstanding stock has exploded by trillions of dollars.

| Key takeaways |

|---|

|

FX: King Dollar

The biggest danger in global finance this decade landed with the euro-area crisis, which threatened to wipe out the most ambitious currency project in history.

High levels of government debt, soaring bond yields and a collapse in confidence pushed nations in Europe’s periphery to the brink of bankruptcy. Greek yields soared past 40% at one point in 2012 while those on Italian, Portuguese and Spanish securities also surged.

It took a massive restructuring package and the famous “whatever it takes” declaration from then European Central Bank President Mario Draghi to stave off disaster. But big institutional frailties remain, like the conspicuous lack of a fiscal framework and full banking union. With high debt levels across much of the region and interest rates already at historic lows, the threat of another crisis remains very real.

By contrast the dollar’s status as the world’s premier reserve currency looks as strong as ever, defying post-crisis fears that the center of monetary gravity would shift from America to China. The greenback accounts for some 60% of global foreign exchange reserves, around the same as late 2009 though below 2015 levels.

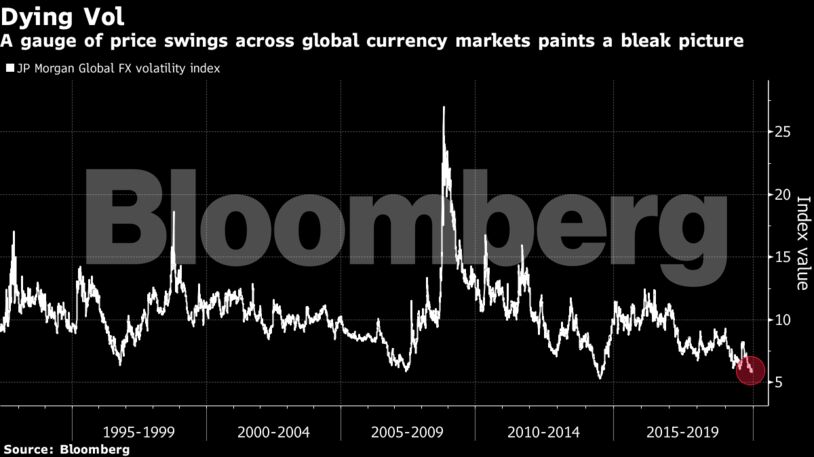

That’s little solace for traders who rely on price swings to make money. While the global currency market has grown by more than a third to $6.6 trillion since 2010, volatility has plummeted as central banks dance to a dovish beat in concert.

“It was pretty much a decade of fire and ice,” said Ned Rumpeltin, European head of foreign-exchange strategy at Toronto Dominion Bank. “We spent so much of the last 10 years lurching from crisis to crisis, but those episodes were interspersed with long periods of low vol.”

There were flare-ups: Flash crashes hit currencies including the British pound and the South African rand, prompting the Bank for International Settlements to warn of danger ahead when volatility roars back to life.

And that’s not the only hurdle the market will have to clear, as automation comes for Wall Street jobs and newfangled technologies like blockchain challenge the established order.

| Key takeaways |

|---|

|

Stocks: Unstoppable Bull

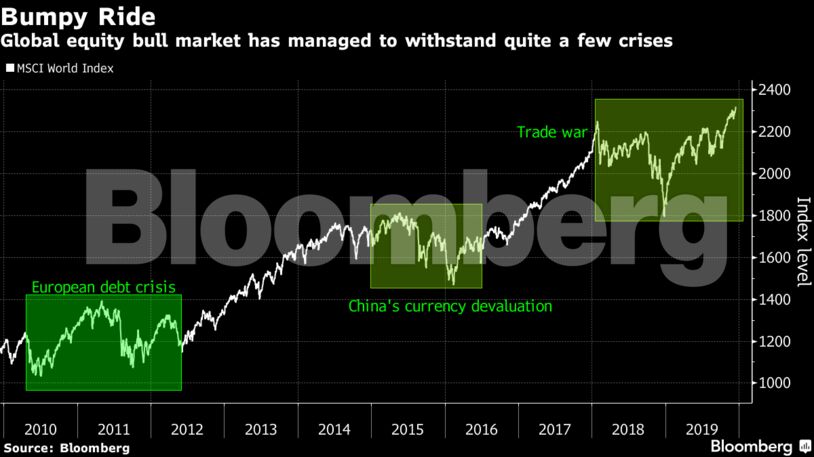

Events like the 2015 yuan devaluation and the 2018 risk rout gave stock bulls a scare, but in the first decade to dodge a U.S. recession since records began it wasn’t enough to break them.

“People can overreact to some of that news flow, which would undermine their ability to capture what’s been a clearly very strong 10-year growth cycle,” said Luke Barrs, EMEA head of fundamental equity client portfolio management at Goldman Sachs Asset Management.

American stocks were ground zero for animal spirits, trouncing developed-market competitors. Adjusted for volatility risk, gains in the S&P 500 index since Dec. 31, 2009 look poised to be the highest of any decade since at least the 1950s.

In dollar terms the Stoxx Europe 600 has posted only a third of the S&P 500’s total returns of more than 250% this decade. The region’s large exposure to beleaguered value shares, political risk from Brexit to Italian populism, and the absence of hot tech companies all played a role. Europe has suffered the biggest outflows among major markets, losing about $100 billion this year alone.

Famously, public equity markets have been shrinking this decade thanks to corporate buybacks, private equity funds taking companies off the market and initial public offerings dwindling. Volumes have also been falling as a result.

Meanwhile a number of leading Democratic candidates for the 2020 U.S. election are proposing higher corporate taxes, further threatening equity returns in the years ahead.

| Key takeaways |

|---|

|

Credit: Leverage Monster

Global corporate debt has nearly doubled this past decade, defying the oil-price crash and memories of the credit crisis. It became a seller’s market like never before: Negative-yielding corporate bonds surpassed $1 trillion in 2019, companies sold longer-duration debt and issuers dispensed with clauses to protect investors.

Corporate bond buyers today are getting vanishing premiums, close to record interest-rate risk and hefty leverage to boot. Anyone investing $100 in U.S. junk bonds on the last day of 2009, however, is sitting on more than double the amount. Europe has produced similar returns.

“It didn’t matter what you owned, everything went up because central banks were buying,” said Jonathan Gregory, a money manager at UBS Asset Management in London. “Who knows what the right price is when you have a buyer like that?”

At the same time the quality of the market has deteriorated. In the past decade, the stock of U.S. bonds rated BBB, the lowest rung of investment grade, has tripled to $3 trillion. If history repeats, a huge swath of credit could fall to junk in a recession.

| Key takeaways |

|---|

|

Crude: Awakening

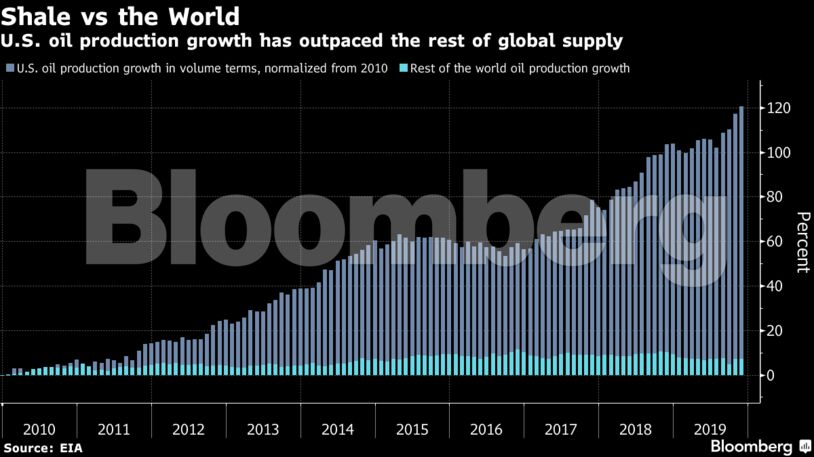

Oil may have spent the first half of the decade dancing around $100 a barrel, but the crash in 2014 told the story that would define global commodity markets for years to come: The shale revolution is here to stay.

“The U.S. has disrupted the industry in a way that was never expected,” said Abhishek Deshpande, head of oil market research at JPMorgan Chase & Co.

American supply has bestowed the market with a game-changing buffer in the face of civil wars, terrorist attacks and military conquests.

A drone strike in September shut down half of Saudi Arabia’s production in the single biggest disruption in the oil market’s history, yet investor reaction was largely sanguine after the initial shock. Lost barrels were offset by inventories.

Citigroup Inc. recently pegged geopolitical risk at its highest in 15 years while WTI prices for 2019 are set for their fourth-lowest average of the decade.

Looming over the market is China’s easing appetite for commodities to feed its export-led economic model. Double-digit oil demand growth has occurred almost half as many times this decade as in the previous one.

There are also bigger threats to the commodity complex as the green lobby and the Paris agreement shape market sentiment, from speculation in the futures market to capital expenditure by oil companies.

| Key takeaways |

|---|

|

Emerging Markets: Alpha Male

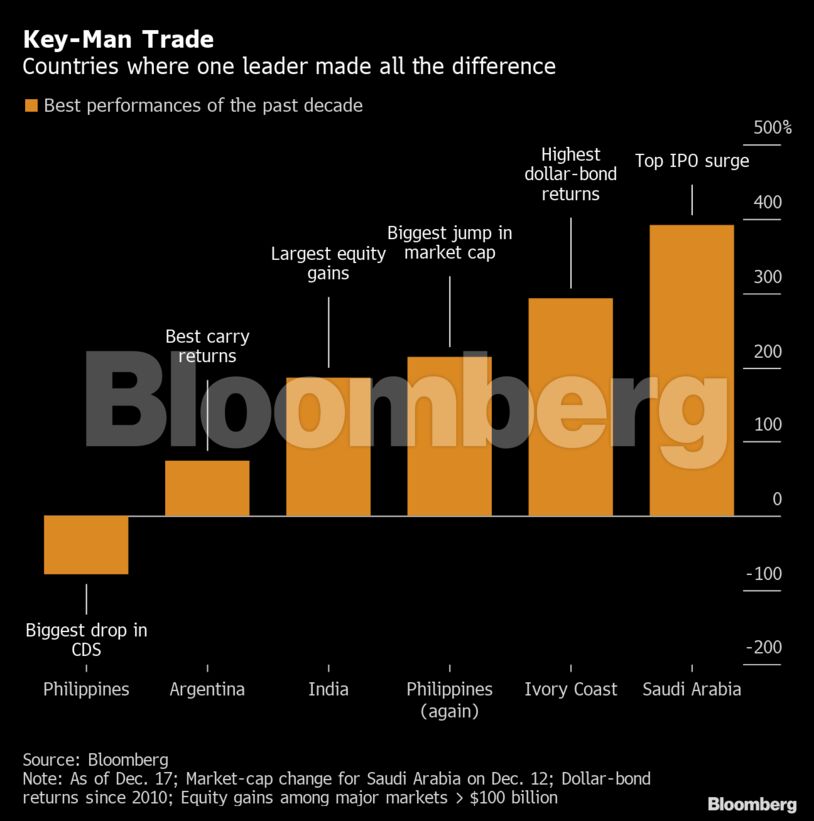

What unites Argentina, India, Ivory Coast, Pakistan, Philippines and Saudi Arabia? At first blush, very little. It takes India hardly any time to produce the full-year gross domestic product of Ivory Coast. The sky-high inflation rates of Argentina contrast with negative price-growth in Saudi Arabia. Pakistan has never enjoyed the leadership continuity common among peers.

Yet global investors have made billions over the past decade casting these markets in a similar vein in a key respect: They are in effect one-man shows.

Think Narendra Modi of India, Mohammed bin Salman of Saudi Arabia, Rodrigo Duterte of the Philippines, Recep Tayyip Erdogan of Turkey, Vladimir Putin of Russia. These men and others helped set the terms for the asset class in the 2010s.

Despite progress made this decade to beef up fiscal, trade and currency regimes, developing economies remain acutely prone to capital volatility, social unrest, and inflation flare-ups. A year’s gains can be wiped out in a week. A stable leader can make all the difference in pushing through reforms and maintaining order, rewarding investors with triple-digit returns along the way.

So-called key man dependence is not without huge risks given the endless political games — a threat looming over markets of all stripes in the 2020s.

| Key takeaways |

|---|

|

–With assistance from Cecile Gutscher, Julian Lee and Selcuk Gokoluk.

Share This: