CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

By Liam Denning

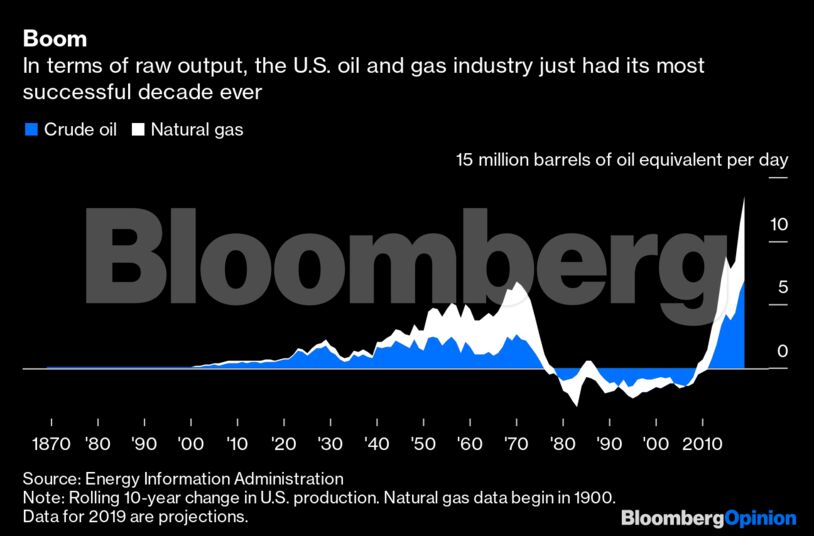

It isn’t an accident this happened in the same, zero-rate decade that gave us the likes of WeWork. Like many a unicorn, the frackers upended a mature industry using cheap capital in a brash grab for market share. Similarly, profits and payouts to shareholders ranked as distant runners-up to that dash for growth.

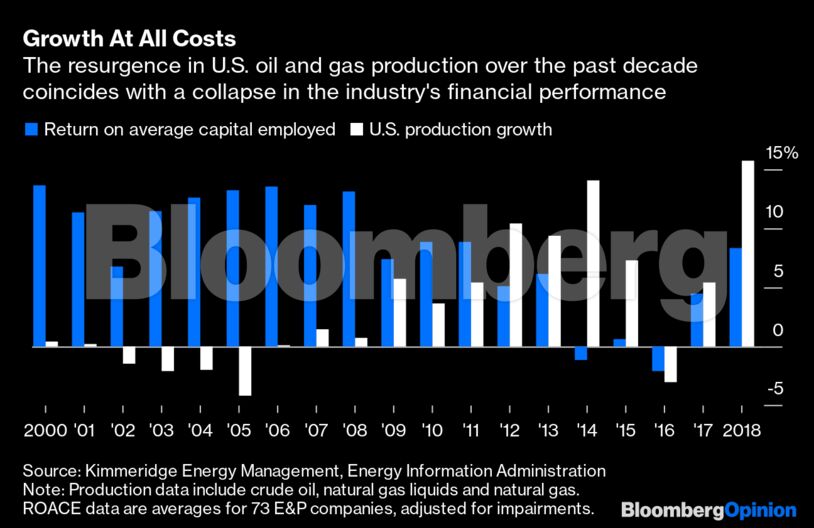

Chesapeake, for example, didn’t generate a single year of positive free cash flow out of the past 10. During that time, it generated $31 billion in cash from operations and topped that up with $44 billion of disposal proceeds. How much of that $75 billion went on capital expenditure? You guessed it: $75 billion.After a decade of no growth and decent returns on capital, the E&P sector took the opposite approach.

Early in the decade, triple-digit oil prices and wide-open equity and junk-bond markets provided a windfall. The E&P sector’s lax governance and perverse incentives ensured much of that ended up either in drilling budgets or sweet compensation packages for insiders. The resulting surplus of oil and gas teed up the crash in late 2014 that is now forcing a reckoning.

Ben Dell, the Bernstein analyst who wrote that report on Chesapeake, went on to found Kimmeridge Energy Management Co., a private equity firm that has engaged in shareholder activism with several E&P companies. These campaigns have echoed the central demands in that report from 2009: better governance and financial discipline.

In particular, Kimmeridge urges smaller E&P companies to merge in order to cut overheads, direct the savings into shareholder payouts and completely overhaul management compensation, with a heavy emphasis on stock awards linked to absolute total shareholder return.

Shifting the priority to returns could not only coax at least some investors back but also cool production growth, thereby taking some of the weight off oil and gas prices. Regarding the latter, Kimmeridge estimates that while the industry’s oil output grew at roughly 10% a year, compounded, in the decade through 2018, the vast majority of that was funded by third-party capital. Purely self-funded growth would have averaged less than 3% a year.

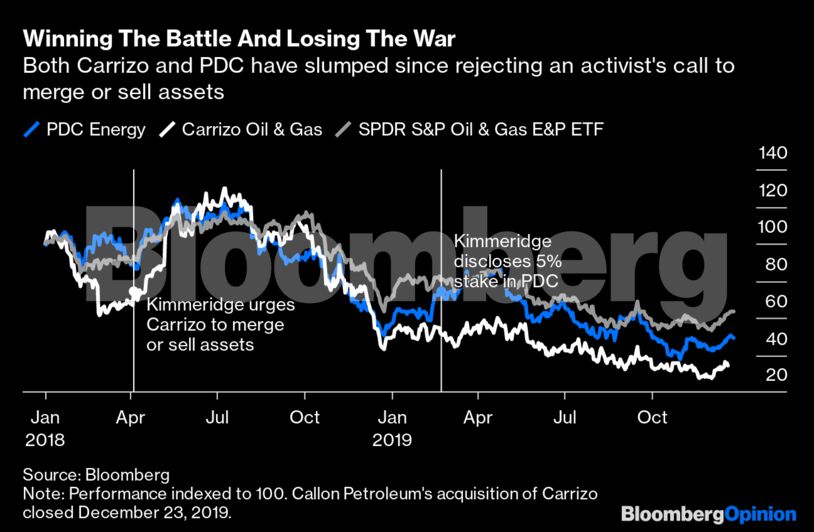

It’s an uphill battle, though. Recent campaigns at PDC Energy Inc. and Carrizo Oil & Gas Inc. were knocked back — although, given what’s happened since, investors may well regret that. Carrizo, especially, went from shrugging off calls to merge to agreeing to sell itself for a relative pittance within roughly 18 months.

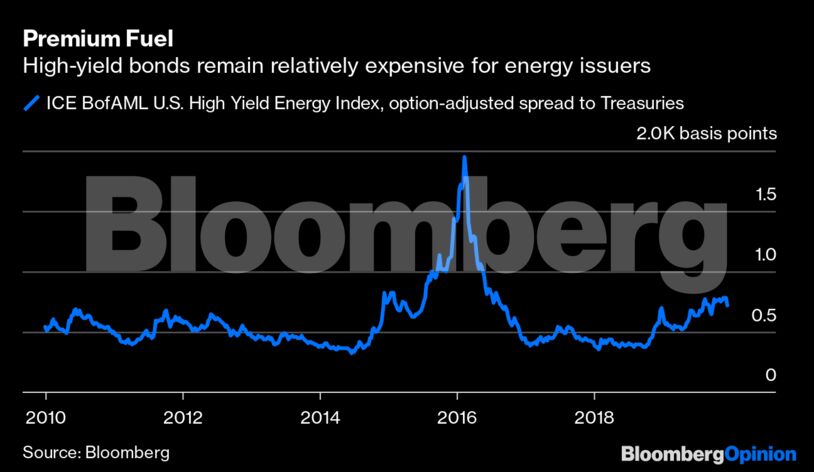

Such experiences may be sinking in, though. Generalist investors have largely deserted the sector, with valuation multiples notably unresponsive to oil prices for much of the past year. Equity and debt issuance has dropped off significantly, and stocks of more-indebted frackers have been hit hardest. While the recent rally in oil prices has eased conditions somewhat in the high-yield bond market, option-adjusted spreads for energy issuers remain elevated versus the more-forgiving levels that fueled the pre-2014 boom and offered relief in 2017-18.

It is fitting that, as the 2010s draw to a close, the biggest E&P company, ConocoPhillips, hosted a recent analyst day that summed up the fallout from the shale boom and what it will take to navigate from here. Growth must be an output, not an input to the model. Cut capital intensity, not just to fund big payouts but also to smooth volatility and resist the cost inflation that comes from following the herd. Above all, with investors AWOL and concerns about climate change sharpening rapidly, don’t assume energy exposure is a must-have. So benchmark against the market rather than just peers; no one gets rich owning the best performer in a bad sector.

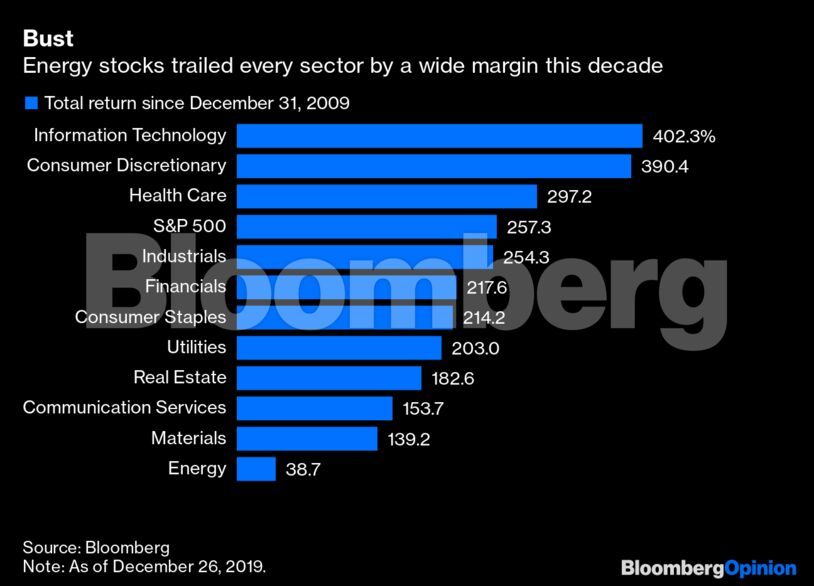

Cheap capital, technological breakthroughs and economic recovery should have added up to a vintage decade for frackers. That it didn’t for many is the result of bad decisions fostered by skewed incentives and enabled by weak oversight. In a business with few certainties, it’s a pretty sure thing this just won’t cut it in the 2020s.

Share This: