CDN NEWS |

CDN NEWS |  US NEWS

US NEWS

External pressure and market circumstances have helped shape the new Russian gas export system so that it can’t really be used as a sinister tool of Putin’s rogue foreign policy. Meanwhile, it’s structured in a such a way that post-Putin Russia will still be able to maintain its energy market share and use it as a basis for useful trade partnerships. That makes it a positive part of Putin’s legacy, if not entirely thanks to Putin.

Problems Inherited and Self-Made

Russia inherited contracts from the Soviet Union to supply natural gas to Europe, one of the biggest sources of hard currency for Russia’s reeling post-Communist economy. But the Soviet pipelines were laid across Ukraine and Belarus, which were part of the empire. But they became independent nations that demanded transit fees and low-priced energy supplies in exchange for maintaining Russia’s energy supplies to Europe, or rather, to its ex-Communist part, where Russia and everything that came from it were newly unpopular.

At the same time, gas suppliers in Central Asia and Azerbaijan presented a competitive threat: It was relatively easy for them to pipe gas to Turkey, which could deliver it further to Europe.

In the 2000s, when Putin and his advisers nurtured the notion of Russia as an “energy superpower,” it became clear to Kremlin strategists that they needed more flexibility to increase supplies and get more economic leverage over neighbors in Europe and Asia. Blue Stream, laid across the bottom of the Black Sea to the Turkish port of Samsun and opened in 2003, was the opening move of the Putin gas game.

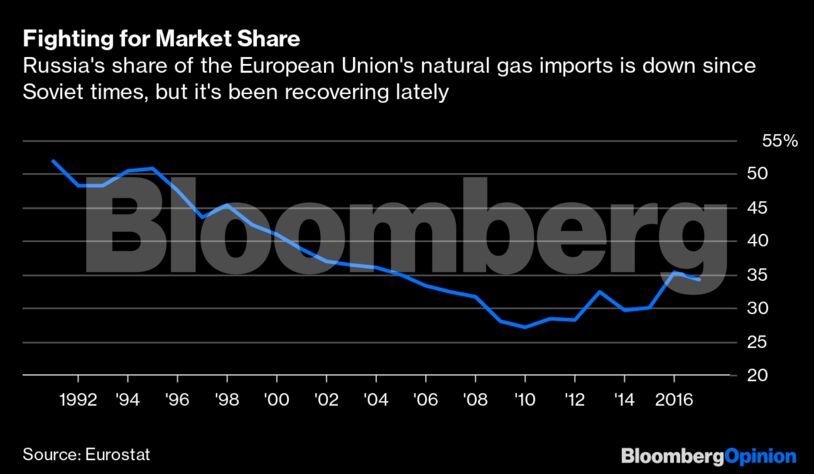

But Blue Stream’s capacity of 16 billion cubic meters of natural gas per year was dwarfed by the roughly 180 billion cubic meters the Soviet-built pipelines could export to Europe via Ukraine and Belarus. It helped Russia compete in Turkey, but didn’t solve the bigger problem of Russia’s dependence on Ukraine and Belarus. The share of European natural gas imports that came from Russia kept falling.

In 2011, Russia obtained full control over the Belarussian gas transit system in exchange for discounted gas supplies. But Ukraine remained firmly in control of its pipelines, which accounted for the lion’s share of Russia’s export capacity.

Putin wanted more direct access to southern and western Europe. He wanted to be able to bypass Ukraine, for both economic and political reasons. The Ukrainian pipeline system, run by National JSC Naftogaz Ukraine, was falling into disrepair, and Gazprom, the Russian export monopoly for pipeline gas, feared it might have to invest in fixing it without having much influence over its operation. At the same time, Putin wanted leverage over the Ukrainian government to keep it in Moscow’s orbit. Twice in the 2000s, Russia cut off gas supplies to Ukraine to try to bring it to heel, but without alternative export routes, such tactics were unsustainable.

In 2012, Russia made another major move with the opening of Nord Stream, stretching across the bottom of the Baltic Sea to northern Germany. With a capacity of 55 billion cubic meters a year, it boosted Russia’s share of European imports. At the same time, Russia was planning a major pipeline to southern Europe, South Stream, across the Black Sea to Bulgaria. From there it would branch out to carry gas to Greece, Italy, Serbia and on to central Europe.

The 2014 Crimea annexation made it imperative for Putin to redraw the gas export map. Now, Ukraine wasn’t just an inconvenient partner, it was an adversary, and bypassing it became a geopolitical necessity for Putin. Europe, too, was more worried than ever about increasing gas exports from Russia, which could use it to expand its political influence. The European Union scuppered South Stream in late 2014 by putting pressure on Bulgaria. Plans to expand Nord Stream by laying two parallel strings of pipe, known as Nord Stream 2, also became politically toxic, especially given U.S. resistance to that project: In Washington, fears of increased Russian leverage over Germany were compounded by the desire to supply more U.S. liquefied natural gas to Europe.

Art of the Possible

The way Russia altered its gas export plans in the last five years reflects a major shift in its geopolitical thinking. Putin’s anti-Western partnerships with key authoritarian regimes — those of Turkish President Recep Tayyip Erdogan and Chinese President Xi Jinping — had to be backed up with gas pipelines. At the same time, Putin wanted to maintain a lifeline to Germany, with its history of regime-agnostic Ostpolitik; Putin, a German speaker and a former Soviet intelligence agent in East Germany, sees Russia’s relationship with Europe as one with Germany first, even if Chancellor Angela Merkel is one of the continent’s least Putin-friendly leaders.

So South Stream mutated into TurkStream, a pipeline with a planned capacity of 31.5 billion cubic meters running to the western part of Turkey, from where gas will flow to the Balkans. It was first filled with gas in late November, and Putin and Erdogan plan to inaugurate it on Jan. 8.

The pipeline to China, Power of Siberia, which should be delivering 38 billion cubic meters of gas a year by 2024, opened early this month, with Putin and Xi watching via video link. It runs from Gazprom’s deposits in Eastern Siberia, too far from Europe for deliveries to make economic sense.

At the same time, Russia has made a point of competing with the U.S. and Middle Eastern suppliers on the new and fast-expanding European market for liquefied natural gas. Novatek PJSC, a private company in which state-owned Gazprom is a minority shareholder along with France’s Total SA, started exporting from its enormous LNG facility on the Yamal Peninsula in 2018, and this year it approved a $21 billion investment in a second LNG plant. (Gazprom and Rosneft, another state company, have their own LNG capacity, but mostly for export to Asian markets). In the third quarter of 2019, Russia was the EU’s second biggest LNG supplier after Qatar, with 15% of imports; the U.S. was fourth, with 12% — although data from the U.S. Energy Information Administration show that the U.S. has overtaken Russia more recently.

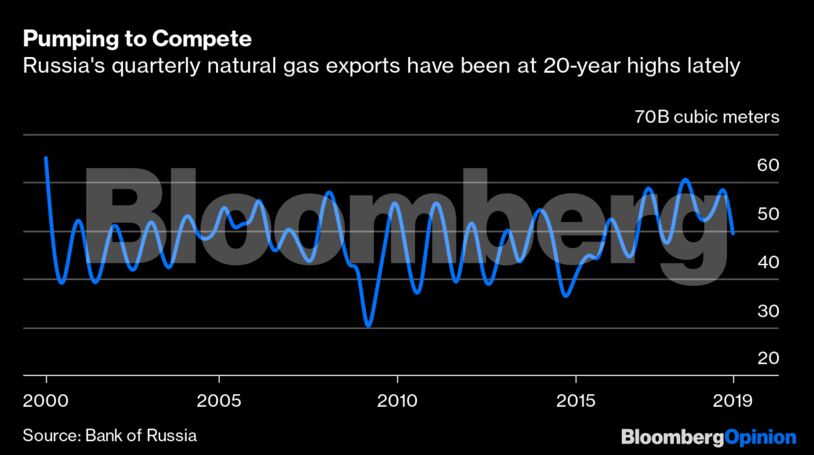

All these developments make it almost inevitable that Russian natural gas exports will keep increasing as spare production capacity keeps shrinking.

Though vessels laying pipe for Nord Stream 2 and their owners have been sanctioned by the U.S., and Swiss contractor Allseas has suspended work on the project to avoid falling afoul of the U.S. government, that pipeline will be completed, too. Gazprom and one of its Russian contractors have pipe-laying vessels of their own. Though they’ll move slower than the bigger one provided by Allseas, Peter Beyer, the German government’s coordinator for trans-Atlantic issues, said in a radio interview on Monday that the government expected Nord Stream 2 to be operational in the second half of 2020.

The delay has forced Russia to do a better deal with Ukraine than it would have been able to negotiate had there been no Nord Stream 2 sanctions. To replace the transit deal that runs out at the end of this year, Russia was trying to sign a mere one-year extension. Ukraine and the EU, which mediated the talks, were fighting for a 10-year contract that would spell out a minimum amount of gas for Gazprom to pump every year. Ukraine gets about $3 billion a year in transit fees from Gazprom, and it would develop a major hole in its budget without the funds.

Russia agreed to a five-year deal with a minimum of 65 billion cubic meters to be supplied in 2020 (slightly less than this year’s projected imports) and 40 billion cubic meters in the following years.

Both sides compromised on outstanding litigation that arose from the two countries’ previous tumultuous relationship as partners in the natural gas business. Gazprom agreed to pay Naftogaz the $3 billion it had won in an arbitration case, and Naftogaz agreed to drop lawsuits seek an additional $8 billion and to refrain from filing any others.

Other compromises may have been reached, too. It’s been reported in Ukraine that Russia might resume direct supplies of gas for Ukraine’s own needs — something unthinkable under former Ukrainian President Petro Poroshenko’s government, when Ukraine was buying Russian gas in the EU rather than deal with the invader of Crimea. Russia is denying that direct supplies are part of the deal, but current Ukiraine president, Volodymyr Zelenskiy, is more pragmatic than Poroshenko was and eager to end the armed conflict Russia has instigated in Ukraine’s eastern regions. The new gas deal, described by the EU official who brokered it as a win-win solution for both sides, shows that Putin, with his transactional approach to foreign policy, values Zelenskiy’s willingness to bargain and compromise.

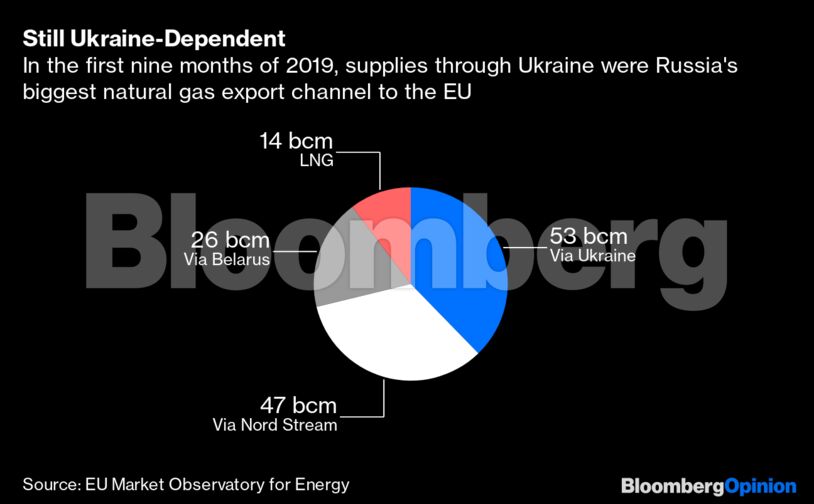

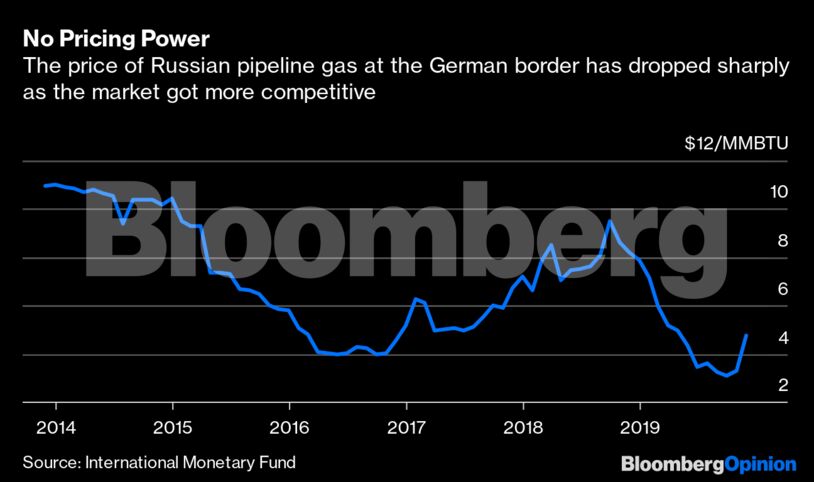

As a result, Ukraine will remain an important pillar of the new Russian gas export scheme at least for the next five years. Though Putin didn’t originally want that, making every effort to establish gas supply channels that go around it, Russia’s resulting export system is remarkably balanced. It links Russia to China, Turkey, southern, northern and eastern Europe. All these markets are competitive, especially in Europe, where the EU has cracked down on Gazprom’s earlier attempts at monopoly pricing.

Putin may have made and changed his plans for export channels in hopes of geopolitical leverage. This — and the big infrastructure contracts for Kremlin cronies that came with the pipeline buildout — helped justify the tens of billions of dollars invested in the pipeline and LNG projects. Gazprom’s capital expenditure has averaged $6.4 billion per quarter in the last five years, some 23% of the average quarterly revenue over the same period. The company has remained profitable throughout, but it has more than doubled its debt load since 2013, while revenue has increased by a projected 40% this year compared with 2014.

Now that the infrastructure mostly is in place and the deposits needed to feed it are either online or coming online in the near future, the marginal cost of exporting gas will be relatively low, and Russia is guaranteed a solid export revenue stream in a fast-changing global gas market. That’s important for a country that exported $49.1 billion worth of natural gas in 2018 and collected some 7% of its budget revenues from the gas industry.

Russia’s export partners, of course, eventually move to phase out fossil fuels. That, however, won’t be happening anytime soon, as both Europe and China will need more gas as they replace coal. Russia is projected to account for around a third of the EU’s gas supply at least until 2040.

Putin will be gone by then, but Russia’s energy trade will be more diversified than when he came to power. More benign Russian governments will be able to use it as a basis for good neighborly relations rather than as an instrument of pressure. The results of Putin’s grand project show how multiple players — Putin the ambitious authoritarian, his situational allies such as Erdogan and Xi, his adversaries such as the U.S., his reluctant partners such as the EU and his victims such as Ukraine — can combine efforts to build something worthwhile.

Share This: